-

Trailing stop is a popular stop-loss trading strategy by which the investor

will sell the asset once its price experiences a pre-specified percentage

drawdown. In this paper, we study the problem of timing buy and then sell an

asset subject to a trailing stop. Under a general linear diffusion framework,

we study an optimal double stopping problem with a random path-dependent

maturity. Specifically, we first derive the optimal liquidation strategy prior

to a given trailing stop, and prove the optimality of using a sell limit order

in conjunction with the trailing stop. Our analytic results for the liquidation

problem is then used to solve for the optimal strategy to acquire the asset and

simultaneously initiate the trailing stop. The method of solution also lends

itself to an efficient numerical method for computing the the optimal

acquisition and liquidation regions. For illustration, we implement an example

and conduct a sensitivity analysis under the exponential Ornstein-Uhlenbeck

model.

-

In this paper, we present a family of a control-stopping games which arise

naturally in equilibrium-based models of market microstructure, as well as in

other models with strategic buyers and sellers. A distinctive feature of this

family of games is the fact that the agents do not have any exogenously given

fundamental value for the asset, and they deduce the value of their position

from the bid and ask prices posted by other agents (i.e. they are pure

speculators). As a result, in such a game, the reward function of each agent,

at the time of stopping, depends directly on the controls of other players. The

equilibrium problem leads naturally to a system of coupled control-stopping

problems (or, equivalently, Reflected Backward Stochastic Differential

Equations (RBSDEs)), in which the individual reward functions (or, reflecting

barriers) depend on the value functions (or, solution components) of other

agents. The resulting system, in general, presents multiple mathematical

challenges due to the non-standard form of coupling (or, reflection). In the

present case, this system is also complicated by the fact that the continuous

controls of the agents, describing their posted bid and ask prices, are

constrained to take values in a discrete grid. The latter feature reflects the

presence of a positive tick size in the market, and it creates additional

discontinuities in the agents reward functions (or, reflecting barriers).

Herein, we prove the existence of a solution to the associated system in a

special Markovian framework, provide numerical examples, and discuss the

potential applications.

-

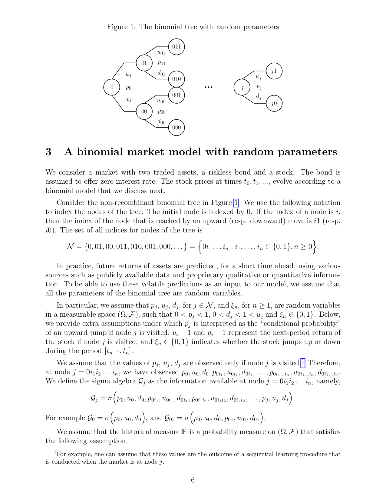

We introduce a new class of forward performance processes that are endogenous

and predictable with regards to an underlying market information set and,

furthermore, are updated at discrete times. We analyze in detail a binomial

model whose parameters are random and updated dynamically as the market

evolves. We show that the key step in the construction of the associated

predictable forward performance process is to solve a single-period inverse

investment problem, namely, to determine, period-by-period and conditionally on

the current market information, the end-time utility function from a given

initial-time value function. We reduce this inverse problem to solving a

functional equation and establish conditions for the existence and uniqueness

of its solutions in the class of inverse marginal functions.

-

We consider the problem of stopping a diffusion process with a payoff

functional that renders the problem time-inconsistent. We study stopping

decisions of naive agents who reoptimize continuously in time, as well as

equilibrium strategies of sophisticated agents who anticipate but lack control

over their future selves' behaviors. When the state process is one dimensional

and the payoff functional satisfies some regularity conditions, we prove that

any equilibrium can be obtained as a fixed point of an operator. This operator

represents strategic reasoning that takes the future selves' behaviors into

account. We then apply the general results to the case when the agents distort

probability and the diffusion process is a geometric Brownian motion. The

problem is inherently time-inconsistent as the level of distortion of a same

event changes over time. We show how the strategic reasoning may turn a naive

agent into a sophisticated one. Moreover, we derive stopping strategies of the

two types of agent for various parameter specifications of the problem,

illustrating rich behaviors beyond the extreme ones such as "never-stopping" or

"never-starting".

-

We investigate the supports of extremal martingale measures with

pre-specified marginals in a two-period setting. First, we establish in full

generality the equivalence between the extremality of a given measure $Q$ and

the denseness in $L^1(Q)$ of a suitable linear subspace, which can be seen in a

financial context as the set of all semi-static trading strategies. Moreover,

when the supports of both marginals are countable, we focus on the slightly

stronger notion of weak exact predictable representation property (henceforth,

WEP) and provide two combinatorial sufficient conditions, called "2-link

property" and "full erasability", on how the points in the supports are linked

to each other for granting extremality. When the support of the first marginal

is a finite set, we give a necessary and sufficient condition for the WEP to

hold in terms of the new concepts of $2$-net and deadlock. Finally, we study

the relation between cycles and extremality.

-

We demonstrate that the use of asymptotic expansion as prior knowledge in the

"deep BSDE solver", which is a deep learning method for high dimensional BSDEs

proposed by Weinan E, Han & Jentzen (2017), drastically reduces the loss

function and accelerates the speed of convergence. We illustrate the technique

and its implications by using Bergman's model with different lending and

borrowing rates as a typical model for FVA as well as a class of solvable BSDEs

with quadratic growth drivers. We also present an extension of the deep BSDE

solver for reflected BSDEs representing American option prices.

-

We study time reversal, last passage time, and $h$-transform of linear

diffusions. For general diffusions with killing, we obtain the probability

density of the last passage time to an arbitrary level and analyze the

distribution of the time left until killing after the last passage time. With

these tools, we develop a new risk management framework for companies based on

the leverage process (the ratio of a company asset process over its debt) and

its corresponding alarming level. We also suggest how a company can determine

the alarming level for the leverage process by constructing a relevant

optimization problem.

-

We introduce a novel class of credit risk models in which the drift of the

survival process of a firm is a linear function of the factors. The prices of

defaultable bonds and credit default swaps (CDS) are linear-rational in the

factors. The price of a CDS option can be uniformly approximated by polynomials

in the factors. Multi-name models can produce simultaneous defaults, generate

positively as well as negatively correlated default intensities, and

accommodate stochastic interest rates. A calibration study illustrates the

versatility of these models by fitting CDS spread time series. A numerical

analysis validates the efficiency of the option price approximation method.

-

We introduce the entropic measure transform (EMT) problem for a general

process and prove the existence of a unique optimal measure characterizing the

solution. The density process of the optimal measure is characterized using a

semimartingale BSDE under general conditions. The EMT is used to reinterpret

the conditional entropic risk-measure and to obtain a convenient formula for

the conditional expectation of a process which admits an affine representation

under a related measure. The entropic measure transform is then used provide a

new characterization of defaultable bond prices, forward prices, and futures

prices when the asset is driven by a jump diffusion. The characterization of

these pricing problems in terms of the EMT provides economic interpretations as

a maximization of returns subject to a penalty for removing financial risk as

expressed through the aggregate relative entropy. The EMT is shown to extend

the optimal stochastic control characterization of default-free bond prices of

Gombani and Runggaldier (Math. Financ. 23(4):659-686, 2013). These methods are

illustrated numerically with an example in the defaultable bond setting.

-

We consider an optimal consumption/investment problem to maximize expected

utility from consumption. In this market model, the investor is allowed to

choose a portfolio which consists of one bond, one liquid risky asset (no

transaction costs) and one illiquid risky asset (proportional transaction

costs). We fully characterize the optimal consumption and trading strategies in

terms of the solution of the free boundary ODE with an integral constraint. We

find an explicit characterization of model parameters for the well-posedness of

the problem, and show that the problem is well-posed if and only if there

exists a shadow price process. Finally, we describe how the investor's optimal

strategy is affected by the additional opportunity of trading the liquid risky

asset, compared to the simpler model with one bond and one illiquid risky

asset.

-

We study discretizations of polynomial processes using finite state Markov

processes satisfying suitable moment matching conditions. The states of these

Markov processes together with their transition probabilities can be

interpreted as Markov cubature rules. The polynomial property allows us to

study such rules using algebraic techniques. Markov cubature rules aid the

tractability of path-dependent tasks such as American option pricing in models

where the underlying factors are polynomial processes.

-

Optimal liquidation of an asset with unknown constant drift and stochastic

regime-switching volatility is studied. The uncertainty about the drift is

represented by an arbitrary probability distribution; the stochastic volatility

is modelled by $m$-state Markov chain. Using filtering theory, an equivalent

reformulation of the original problem as a four-dimensional optimal stopping

problem is found and then analysed by constructing approximating sequences of

three-dimensional optimal stopping problems. An optimal liquidation strategy

and various structural properties of the problem are determined. Analysis of

the two-point prior case is presented in detail, building on which, an outline

of the extension to the general prior case is given.

-

In classical optimal transport, the contributions of Benamou-Brenier and

McCann regarding the time-dependent version of the problem are cornerstones of

the field and form the basis for a variety of applications in other

mathematical areas.

We suggest a Benamou-Brenier type formulation of the martingale transport

problem for given $d$-dimensional distributions $\mu, \nu $ in convex order.

The unique solution $M^*=(M_t^*)_{t\in [0,1]}$ of this problem turns out to be

a Markov-martingale which has several notable properties: In a specific sense

it mimics the movement of a Brownian particle as closely as possible subject to

the conditions $M^*_0\sim\mu, M^*_1\sim \nu$. Similar to McCann's

displacement-interpolation, $M^*$ provides a time-consistent interpolation

between $\mu$ and $\nu$. For particular choices of the initial and terminal

law, $M^*$ recovers archetypical martingales such as Brownian motion, geometric

Brownian motion, and the Bass martingale. Furthermore, it yields a natural

approximation to the local vol model and a new approach to Kellerer's theorem.

This article is parallel to the work of Huesmann-Trevisan, who consider a

related class of problems from a PDE-oriented perspective.

-

We study the optimal liquidation problem in a market model where the bid

price follows a geometric pure jump process whose local characteristics are

driven by an unobservable finite-state Markov chain and by the liquidation

rate. This model is consistent with stylized facts of high frequency data such

as the discrete nature of tick data and the clustering in the order flow. We

include both temporary and permanent effects into our analysis. We use

stochastic filtering to reduce the optimal liquidation problem to an equivalent

optimization problem under complete information. This leads to a stochastic

control problem for piecewise deterministic Markov processes (PDMPs). We carry

out a detailed mathematical analysis of this problem. In particular, we derive

the optimality equation for the value function, we characterize the value

function as continuous viscosity solution of the associated dynamic programming

equation, and we prove a novel comparison result. The paper concludes with

numerical results illustrating the impact of partial information and price

impact on the value function and on the optimal liquidation rate.

-

These are course notes on the application of SDEs to options pricing. The

author was partially supported by NSF grant DMS-0739195.

-

We model continuous-time information flows generated by a number of

information sources that switch on and off at random times. By modulating a

multi-dimensional L\'evy random bridge over a random point field, our framework

relates the discovery of relevant new information sources to jumps in

conditional expectation martingales. In the canonical Brownian random bridge

case, we show that the underlying measure-valued process follows jump-diffusion

dynamics, where the jumps are governed by information switches. The dynamic

representation gives rise to a set of stochastically-linked Brownian motions on

random time intervals that capture evolving information states, as well as to a

state-dependent stochastic volatility evolution with jumps. The nature of

information flows usually exhibits complex behaviour, however, we maintain

analytic tractability by introducing what we term the effective and

complementary information processes, which dynamically incorporate active and

inactive information, respectively. As an application, we price a financial

vanilla option, which we prove is expressed by a weighted sum of option values

based on the possible state configurations at expiry. This result may be viewed

as an information-based analogue of Merton's option price, but where

jump-diffusion arises endogenously. The proposed information flows also lend

themselves to the quantification of asymmetric informational advantage among

competitive agents, a feature we analyse by notions of information geometry.

-

We study super-replication of contingent claims in markets with delayed

filtration. The first result in this paper reveals that in the Black--Scholes

model with constant delay the super-replication price is prohibitively costly

and leads to trivial buy-and-hold strategies. Our second result says that the

scaling limit of super--replication prices for binomial models with a fixed

number of times of delay $H$ is equal to the $G$--expectation with volatility

uncertainty interval $[0,\sigma\sqrt{H+1}]$.

-

We study an infinite-horizon discrete-time optimal stopping problem under

non-exponential discounting. A new method, which we call the iterative

approach, is developed to find subgame perfect Nash equilibria. When the

discount function induces decreasing impatience, we establish the existence of

an equilibrium through fixed-point iterations. Moreover, we show that there

exists a unique optimal equilibrium, which generates larger value than any

other equilibrium does at all times. To the best of our knowledge, this is the

first time a dominating subgame perfect Nash equilibrium is shown to exist in

the literature of time-inconsistency.

-

This paper is devoted to obtaining a wellposedness result for

multidimensional BSDEs with possibly unbounded random time horizon and driven

by a general martingale in a filtration only assumed to satisfy the usual

hypotheses, i.e. the filtration may be stochastically discontinuous. We show

that for stochastic Lipschitz generators and unbounded, possibly infinite, time

horizon, these equations admit a unique solution in appropriately weighted

spaces. Our result allows in particular to obtain a wellposedness result for

BSDEs driven by discrete--time approximations of general martingales.

-

We discuss the binary nature of funding impact in derivative valuation. Under

some conditions, funding is either a cost or a benefit, i.e., one of the

lending/borrowing rates does not play a role in pricing derivatives. When

derivatives are priced, considering different lending/borrowing rates leads to

semi-linear BSDEs and PDEs, and thus it is necessary to solve the equations

numerically. However, once it can be guaranteed that only one of the rates

affects pricing, linear equations can be recovered and analytical formulae can

be derived. Moreover, as a byproduct, our results explain how debt value

adjustment (DVA) and funding benefits are dissimilar. It is often believed that

considering both DVA and funding benefits results in a double-counting issue

but it will be shown that the two components are affected by different

mathematical structures of derivative transactions. We find that funding

benefit is related to the decreasing property of the payoff function, but this

relationship decreases as the funding choices of underlying assets are

transferred to repo markets.

-

The paper studies the First Order BSPDEs (Backward Stochastic Partial

Differential Equations) suggested earlier for a case of multidimensional state

domain with a boundary. These equations represent analogs of

Hamilton-Jacobi-Bellman equations and allow to construct the value function for

stochastic optimal control problems with unspecified dynamics where the

underlying processes do not necessarily satisfy stochastic differential

equations of a known kind with a given structure. The problems considered arise

in financial modelling.

-

We analyse the optimal exercise of an executive stock option (ESO) written on

a stock whose drift parameter falls to a lower value at a change point, an

exponentially distributed random time independent of the Brownian motion

driving the stock. Two agents, who do not trade the stock, have differing

information on the change point, and seek to optimally exercise the option by

maximising its discounted payoff under the physical measure. The first agent

has full information, and observes the change point. The second agent has

partial information and filters the change point from price observations. This

scenario is designed to mimic the positions of two employees of varying

seniority, a fully informed executive and a partially informed less senior

employee, each of whom receives an ESO. The partial information scenario yields

a model under the observation filtration $\widehat{\mathbb{F}}$ in which the

stock drift becomes a diffusion driven by the innovations process, an

$\widehat{\mathbb{F}}$-Brownian motion also driving the stock under

$\widehat{\mathbb{F}}$, and the partial information optimal stopping value

function has two spatial dimensions. We rigorously characterise the free

boundary PDEs for both agents, establish shape and regularity properties of the

associated optimal exercise boundaries, and prove the smooth pasting property

in both information scenarios, exploiting some stochastic flow ideas to do so

in the partial information case. We develop finite difference algorithms to

numerically solve both agents' exercise and valuation problems and illustrate

that the additional information of the fully informed agent can result in

exercise patterns which exploit the information on the change point, lending

credence to empirical studies which suggest that privileged information of bad

news is a factor leading to early exercise of ESOs prior to poor stock price

performance.

-

We present a solution to an optimal stopping problem for a process with a

wide-class of novel dynamics. The dynamics model the support/resistance line

concept from financial technical analysis.

-

We show that when the price process $S$ represents a fully incomplete market,

the optimal super-replication of any Markovian claim $g(S_T)$ with $g(\cdot)$

being nonnegative and lower semicontinuous is of buy-and-hold type. Since both

(unbounded) stochastic volatility models and rough volatility models are

examples of fully incomplete markets, one can interpret the buy-and-hold

property when super-replicating Markovian claims as a natural phenomenon in

incomplete markets.

-

We study super--replication of contingent claims in markets with fixed

transaction costs. This can be viewed as a stochastic impulse control problem

with a terminal state constraint. The first result in this paper reveals that

in reasonable continuous time financial market models the super--replication

price is prohibitively costly and leads to trivial buy--and--hold strategies.

Our second result derives nontrivial scaling limits of super--replication

prices for binomial models with small fixed costs.

Trailing stop is a popular stop-loss trading strategy by which the investor will sell the asset once its price experiences a pre-specified percentage drawdown. In this paper, we study the problem of timing buy and then sell an asset subject to a trailing stop. Under a general linear diffusion framework, we study an optimal double stopping problem with a random path-dependent maturity. Specifically, we first derive the optimal liquidation strategy prior to a given trailing stop, and prove the optimality of using a sell limit order in conjunction with the trailing stop. Our analytic results for the liquidation problem is then used to solve for the optimal strategy to acquire the asset and simultaneously initiate the trailing stop. The method of solution also lends itself to an efficient numerical method for computing the the optimal acquisition and liquidation regions. For illustration, we implement an example and conduct a sensitivity analysis under the exponential Ornstein-Uhlenbeck model.

Trailing stop is a popular stop-loss trading strategy by which the investor will sell the asset once its price experiences a pre-specified percentage drawdown. In this paper, we study the problem of timing buy and then sell an asset subject to a trailing stop. Under a general linear diffusion framework, we study an optimal double stopping problem with a random path-dependent maturity. Specifically, we first derive the optimal liquidation strategy prior to a given trailing stop, and prove the optimality of using a sell limit order in conjunction with the trailing stop. Our analytic results for the liquidation problem is then used to solve for the optimal strategy to acquire the asset and simultaneously initiate the trailing stop. The method of solution also lends itself to an efficient numerical method for computing the the optimal acquisition and liquidation regions. For illustration, we implement an example and conduct a sensitivity analysis under the exponential Ornstein-Uhlenbeck model.

In this paper, we present a family of a control-stopping games which arise naturally in equilibrium-based models of market microstructure, as well as in other models with strategic buyers and sellers. A distinctive feature of this family of games is the fact that the agents do not have any exogenously given fundamental value for the asset, and they deduce the value of their position from the bid and ask prices posted by other agents (i.e. they are pure speculators). As a result, in such a game, the reward function of each agent, at the time of stopping, depends directly on the controls of other players. The equilibrium problem leads naturally to a system of coupled control-stopping problems (or, equivalently, Reflected Backward Stochastic Differential Equations (RBSDEs)), in which the individual reward functions (or, reflecting barriers) depend on the value functions (or, solution components) of other agents. The resulting system, in general, presents multiple mathematical challenges due to the non-standard form of coupling (or, reflection). In the present case, this system is also complicated by the fact that the continuous controls of the agents, describing their posted bid and ask prices, are constrained to take values in a discrete grid. The latter feature reflects the presence of a positive tick size in the market, and it creates additional discontinuities in the agents reward functions (or, reflecting barriers). Herein, we prove the existence of a solution to the associated system in a special Markovian framework, provide numerical examples, and discuss the potential applications.

In this paper, we present a family of a control-stopping games which arise naturally in equilibrium-based models of market microstructure, as well as in other models with strategic buyers and sellers. A distinctive feature of this family of games is the fact that the agents do not have any exogenously given fundamental value for the asset, and they deduce the value of their position from the bid and ask prices posted by other agents (i.e. they are pure speculators). As a result, in such a game, the reward function of each agent, at the time of stopping, depends directly on the controls of other players. The equilibrium problem leads naturally to a system of coupled control-stopping problems (or, equivalently, Reflected Backward Stochastic Differential Equations (RBSDEs)), in which the individual reward functions (or, reflecting barriers) depend on the value functions (or, solution components) of other agents. The resulting system, in general, presents multiple mathematical challenges due to the non-standard form of coupling (or, reflection). In the present case, this system is also complicated by the fact that the continuous controls of the agents, describing their posted bid and ask prices, are constrained to take values in a discrete grid. The latter feature reflects the presence of a positive tick size in the market, and it creates additional discontinuities in the agents reward functions (or, reflecting barriers). Herein, we prove the existence of a solution to the associated system in a special Markovian framework, provide numerical examples, and discuss the potential applications.

We introduce a new class of forward performance processes that are endogenous and predictable with regards to an underlying market information set and, furthermore, are updated at discrete times. We analyze in detail a binomial model whose parameters are random and updated dynamically as the market evolves. We show that the key step in the construction of the associated predictable forward performance process is to solve a single-period inverse investment problem, namely, to determine, period-by-period and conditionally on the current market information, the end-time utility function from a given initial-time value function. We reduce this inverse problem to solving a functional equation and establish conditions for the existence and uniqueness of its solutions in the class of inverse marginal functions.

We introduce a new class of forward performance processes that are endogenous and predictable with regards to an underlying market information set and, furthermore, are updated at discrete times. We analyze in detail a binomial model whose parameters are random and updated dynamically as the market evolves. We show that the key step in the construction of the associated predictable forward performance process is to solve a single-period inverse investment problem, namely, to determine, period-by-period and conditionally on the current market information, the end-time utility function from a given initial-time value function. We reduce this inverse problem to solving a functional equation and establish conditions for the existence and uniqueness of its solutions in the class of inverse marginal functions.

We investigate the supports of extremal martingale measures with pre-specified marginals in a two-period setting. First, we establish in full generality the equivalence between the extremality of a given measure $Q$ and the denseness in $L^1(Q)$ of a suitable linear subspace, which can be seen in a financial context as the set of all semi-static trading strategies. Moreover, when the supports of both marginals are countable, we focus on the slightly stronger notion of weak exact predictable representation property (henceforth, WEP) and provide two combinatorial sufficient conditions, called "2-link property" and "full erasability", on how the points in the supports are linked to each other for granting extremality. When the support of the first marginal is a finite set, we give a necessary and sufficient condition for the WEP to hold in terms of the new concepts of $2$-net and deadlock. Finally, we study the relation between cycles and extremality.

We investigate the supports of extremal martingale measures with pre-specified marginals in a two-period setting. First, we establish in full generality the equivalence between the extremality of a given measure $Q$ and the denseness in $L^1(Q)$ of a suitable linear subspace, which can be seen in a financial context as the set of all semi-static trading strategies. Moreover, when the supports of both marginals are countable, we focus on the slightly stronger notion of weak exact predictable representation property (henceforth, WEP) and provide two combinatorial sufficient conditions, called "2-link property" and "full erasability", on how the points in the supports are linked to each other for granting extremality. When the support of the first marginal is a finite set, we give a necessary and sufficient condition for the WEP to hold in terms of the new concepts of $2$-net and deadlock. Finally, we study the relation between cycles and extremality.

We study time reversal, last passage time, and $h$-transform of linear diffusions. For general diffusions with killing, we obtain the probability density of the last passage time to an arbitrary level and analyze the distribution of the time left until killing after the last passage time. With these tools, we develop a new risk management framework for companies based on the leverage process (the ratio of a company asset process over its debt) and its corresponding alarming level. We also suggest how a company can determine the alarming level for the leverage process by constructing a relevant optimization problem.

We study time reversal, last passage time, and $h$-transform of linear diffusions. For general diffusions with killing, we obtain the probability density of the last passage time to an arbitrary level and analyze the distribution of the time left until killing after the last passage time. With these tools, we develop a new risk management framework for companies based on the leverage process (the ratio of a company asset process over its debt) and its corresponding alarming level. We also suggest how a company can determine the alarming level for the leverage process by constructing a relevant optimization problem.

We introduce a novel class of credit risk models in which the drift of the survival process of a firm is a linear function of the factors. The prices of defaultable bonds and credit default swaps (CDS) are linear-rational in the factors. The price of a CDS option can be uniformly approximated by polynomials in the factors. Multi-name models can produce simultaneous defaults, generate positively as well as negatively correlated default intensities, and accommodate stochastic interest rates. A calibration study illustrates the versatility of these models by fitting CDS spread time series. A numerical analysis validates the efficiency of the option price approximation method.

We introduce a novel class of credit risk models in which the drift of the survival process of a firm is a linear function of the factors. The prices of defaultable bonds and credit default swaps (CDS) are linear-rational in the factors. The price of a CDS option can be uniformly approximated by polynomials in the factors. Multi-name models can produce simultaneous defaults, generate positively as well as negatively correlated default intensities, and accommodate stochastic interest rates. A calibration study illustrates the versatility of these models by fitting CDS spread time series. A numerical analysis validates the efficiency of the option price approximation method.

We consider an optimal consumption/investment problem to maximize expected utility from consumption. In this market model, the investor is allowed to choose a portfolio which consists of one bond, one liquid risky asset (no transaction costs) and one illiquid risky asset (proportional transaction costs). We fully characterize the optimal consumption and trading strategies in terms of the solution of the free boundary ODE with an integral constraint. We find an explicit characterization of model parameters for the well-posedness of the problem, and show that the problem is well-posed if and only if there exists a shadow price process. Finally, we describe how the investor's optimal strategy is affected by the additional opportunity of trading the liquid risky asset, compared to the simpler model with one bond and one illiquid risky asset.

We consider an optimal consumption/investment problem to maximize expected utility from consumption. In this market model, the investor is allowed to choose a portfolio which consists of one bond, one liquid risky asset (no transaction costs) and one illiquid risky asset (proportional transaction costs). We fully characterize the optimal consumption and trading strategies in terms of the solution of the free boundary ODE with an integral constraint. We find an explicit characterization of model parameters for the well-posedness of the problem, and show that the problem is well-posed if and only if there exists a shadow price process. Finally, we describe how the investor's optimal strategy is affected by the additional opportunity of trading the liquid risky asset, compared to the simpler model with one bond and one illiquid risky asset.

We study discretizations of polynomial processes using finite state Markov processes satisfying suitable moment matching conditions. The states of these Markov processes together with their transition probabilities can be interpreted as Markov cubature rules. The polynomial property allows us to study such rules using algebraic techniques. Markov cubature rules aid the tractability of path-dependent tasks such as American option pricing in models where the underlying factors are polynomial processes.

We study discretizations of polynomial processes using finite state Markov processes satisfying suitable moment matching conditions. The states of these Markov processes together with their transition probabilities can be interpreted as Markov cubature rules. The polynomial property allows us to study such rules using algebraic techniques. Markov cubature rules aid the tractability of path-dependent tasks such as American option pricing in models where the underlying factors are polynomial processes.

Optimal liquidation of an asset with unknown constant drift and stochastic regime-switching volatility is studied. The uncertainty about the drift is represented by an arbitrary probability distribution; the stochastic volatility is modelled by $m$-state Markov chain. Using filtering theory, an equivalent reformulation of the original problem as a four-dimensional optimal stopping problem is found and then analysed by constructing approximating sequences of three-dimensional optimal stopping problems. An optimal liquidation strategy and various structural properties of the problem are determined. Analysis of the two-point prior case is presented in detail, building on which, an outline of the extension to the general prior case is given.

Optimal liquidation of an asset with unknown constant drift and stochastic regime-switching volatility is studied. The uncertainty about the drift is represented by an arbitrary probability distribution; the stochastic volatility is modelled by $m$-state Markov chain. Using filtering theory, an equivalent reformulation of the original problem as a four-dimensional optimal stopping problem is found and then analysed by constructing approximating sequences of three-dimensional optimal stopping problems. An optimal liquidation strategy and various structural properties of the problem are determined. Analysis of the two-point prior case is presented in detail, building on which, an outline of the extension to the general prior case is given.

In classical optimal transport, the contributions of Benamou-Brenier and McCann regarding the time-dependent version of the problem are cornerstones of the field and form the basis for a variety of applications in other mathematical areas. We suggest a Benamou-Brenier type formulation of the martingale transport problem for given $d$-dimensional distributions $\mu, \nu $ in convex order. The unique solution $M^*=(M_t^*)_{t\in [0,1]}$ of this problem turns out to be a Markov-martingale which has several notable properties: In a specific sense it mimics the movement of a Brownian particle as closely as possible subject to the conditions $M^*_0\sim\mu, M^*_1\sim \nu$. Similar to McCann's displacement-interpolation, $M^*$ provides a time-consistent interpolation between $\mu$ and $\nu$. For particular choices of the initial and terminal law, $M^*$ recovers archetypical martingales such as Brownian motion, geometric Brownian motion, and the Bass martingale. Furthermore, it yields a natural approximation to the local vol model and a new approach to Kellerer's theorem. This article is parallel to the work of Huesmann-Trevisan, who consider a related class of problems from a PDE-oriented perspective.

In classical optimal transport, the contributions of Benamou-Brenier and McCann regarding the time-dependent version of the problem are cornerstones of the field and form the basis for a variety of applications in other mathematical areas. We suggest a Benamou-Brenier type formulation of the martingale transport problem for given $d$-dimensional distributions $\mu, \nu $ in convex order. The unique solution $M^*=(M_t^*)_{t\in [0,1]}$ of this problem turns out to be a Markov-martingale which has several notable properties: In a specific sense it mimics the movement of a Brownian particle as closely as possible subject to the conditions $M^*_0\sim\mu, M^*_1\sim \nu$. Similar to McCann's displacement-interpolation, $M^*$ provides a time-consistent interpolation between $\mu$ and $\nu$. For particular choices of the initial and terminal law, $M^*$ recovers archetypical martingales such as Brownian motion, geometric Brownian motion, and the Bass martingale. Furthermore, it yields a natural approximation to the local vol model and a new approach to Kellerer's theorem. This article is parallel to the work of Huesmann-Trevisan, who consider a related class of problems from a PDE-oriented perspective.

We study the optimal liquidation problem in a market model where the bid price follows a geometric pure jump process whose local characteristics are driven by an unobservable finite-state Markov chain and by the liquidation rate. This model is consistent with stylized facts of high frequency data such as the discrete nature of tick data and the clustering in the order flow. We include both temporary and permanent effects into our analysis. We use stochastic filtering to reduce the optimal liquidation problem to an equivalent optimization problem under complete information. This leads to a stochastic control problem for piecewise deterministic Markov processes (PDMPs). We carry out a detailed mathematical analysis of this problem. In particular, we derive the optimality equation for the value function, we characterize the value function as continuous viscosity solution of the associated dynamic programming equation, and we prove a novel comparison result. The paper concludes with numerical results illustrating the impact of partial information and price impact on the value function and on the optimal liquidation rate.

We study the optimal liquidation problem in a market model where the bid price follows a geometric pure jump process whose local characteristics are driven by an unobservable finite-state Markov chain and by the liquidation rate. This model is consistent with stylized facts of high frequency data such as the discrete nature of tick data and the clustering in the order flow. We include both temporary and permanent effects into our analysis. We use stochastic filtering to reduce the optimal liquidation problem to an equivalent optimization problem under complete information. This leads to a stochastic control problem for piecewise deterministic Markov processes (PDMPs). We carry out a detailed mathematical analysis of this problem. In particular, we derive the optimality equation for the value function, we characterize the value function as continuous viscosity solution of the associated dynamic programming equation, and we prove a novel comparison result. The paper concludes with numerical results illustrating the impact of partial information and price impact on the value function and on the optimal liquidation rate.

These are course notes on the application of SDEs to options pricing. The author was partially supported by NSF grant DMS-0739195.

These are course notes on the application of SDEs to options pricing. The author was partially supported by NSF grant DMS-0739195.

We model continuous-time information flows generated by a number of information sources that switch on and off at random times. By modulating a multi-dimensional L\'evy random bridge over a random point field, our framework relates the discovery of relevant new information sources to jumps in conditional expectation martingales. In the canonical Brownian random bridge case, we show that the underlying measure-valued process follows jump-diffusion dynamics, where the jumps are governed by information switches. The dynamic representation gives rise to a set of stochastically-linked Brownian motions on random time intervals that capture evolving information states, as well as to a state-dependent stochastic volatility evolution with jumps. The nature of information flows usually exhibits complex behaviour, however, we maintain analytic tractability by introducing what we term the effective and complementary information processes, which dynamically incorporate active and inactive information, respectively. As an application, we price a financial vanilla option, which we prove is expressed by a weighted sum of option values based on the possible state configurations at expiry. This result may be viewed as an information-based analogue of Merton's option price, but where jump-diffusion arises endogenously. The proposed information flows also lend themselves to the quantification of asymmetric informational advantage among competitive agents, a feature we analyse by notions of information geometry.

We model continuous-time information flows generated by a number of information sources that switch on and off at random times. By modulating a multi-dimensional L\'evy random bridge over a random point field, our framework relates the discovery of relevant new information sources to jumps in conditional expectation martingales. In the canonical Brownian random bridge case, we show that the underlying measure-valued process follows jump-diffusion dynamics, where the jumps are governed by information switches. The dynamic representation gives rise to a set of stochastically-linked Brownian motions on random time intervals that capture evolving information states, as well as to a state-dependent stochastic volatility evolution with jumps. The nature of information flows usually exhibits complex behaviour, however, we maintain analytic tractability by introducing what we term the effective and complementary information processes, which dynamically incorporate active and inactive information, respectively. As an application, we price a financial vanilla option, which we prove is expressed by a weighted sum of option values based on the possible state configurations at expiry. This result may be viewed as an information-based analogue of Merton's option price, but where jump-diffusion arises endogenously. The proposed information flows also lend themselves to the quantification of asymmetric informational advantage among competitive agents, a feature we analyse by notions of information geometry.

We study an infinite-horizon discrete-time optimal stopping problem under non-exponential discounting. A new method, which we call the iterative approach, is developed to find subgame perfect Nash equilibria. When the discount function induces decreasing impatience, we establish the existence of an equilibrium through fixed-point iterations. Moreover, we show that there exists a unique optimal equilibrium, which generates larger value than any other equilibrium does at all times. To the best of our knowledge, this is the first time a dominating subgame perfect Nash equilibrium is shown to exist in the literature of time-inconsistency.

We study an infinite-horizon discrete-time optimal stopping problem under non-exponential discounting. A new method, which we call the iterative approach, is developed to find subgame perfect Nash equilibria. When the discount function induces decreasing impatience, we establish the existence of an equilibrium through fixed-point iterations. Moreover, we show that there exists a unique optimal equilibrium, which generates larger value than any other equilibrium does at all times. To the best of our knowledge, this is the first time a dominating subgame perfect Nash equilibrium is shown to exist in the literature of time-inconsistency.

This paper is devoted to obtaining a wellposedness result for multidimensional BSDEs with possibly unbounded random time horizon and driven by a general martingale in a filtration only assumed to satisfy the usual hypotheses, i.e. the filtration may be stochastically discontinuous. We show that for stochastic Lipschitz generators and unbounded, possibly infinite, time horizon, these equations admit a unique solution in appropriately weighted spaces. Our result allows in particular to obtain a wellposedness result for BSDEs driven by discrete--time approximations of general martingales.

This paper is devoted to obtaining a wellposedness result for multidimensional BSDEs with possibly unbounded random time horizon and driven by a general martingale in a filtration only assumed to satisfy the usual hypotheses, i.e. the filtration may be stochastically discontinuous. We show that for stochastic Lipschitz generators and unbounded, possibly infinite, time horizon, these equations admit a unique solution in appropriately weighted spaces. Our result allows in particular to obtain a wellposedness result for BSDEs driven by discrete--time approximations of general martingales.

We discuss the binary nature of funding impact in derivative valuation. Under some conditions, funding is either a cost or a benefit, i.e., one of the lending/borrowing rates does not play a role in pricing derivatives. When derivatives are priced, considering different lending/borrowing rates leads to semi-linear BSDEs and PDEs, and thus it is necessary to solve the equations numerically. However, once it can be guaranteed that only one of the rates affects pricing, linear equations can be recovered and analytical formulae can be derived. Moreover, as a byproduct, our results explain how debt value adjustment (DVA) and funding benefits are dissimilar. It is often believed that considering both DVA and funding benefits results in a double-counting issue but it will be shown that the two components are affected by different mathematical structures of derivative transactions. We find that funding benefit is related to the decreasing property of the payoff function, but this relationship decreases as the funding choices of underlying assets are transferred to repo markets.

We discuss the binary nature of funding impact in derivative valuation. Under some conditions, funding is either a cost or a benefit, i.e., one of the lending/borrowing rates does not play a role in pricing derivatives. When derivatives are priced, considering different lending/borrowing rates leads to semi-linear BSDEs and PDEs, and thus it is necessary to solve the equations numerically. However, once it can be guaranteed that only one of the rates affects pricing, linear equations can be recovered and analytical formulae can be derived. Moreover, as a byproduct, our results explain how debt value adjustment (DVA) and funding benefits are dissimilar. It is often believed that considering both DVA and funding benefits results in a double-counting issue but it will be shown that the two components are affected by different mathematical structures of derivative transactions. We find that funding benefit is related to the decreasing property of the payoff function, but this relationship decreases as the funding choices of underlying assets are transferred to repo markets.

We present a solution to an optimal stopping problem for a process with a wide-class of novel dynamics. The dynamics model the support/resistance line concept from financial technical analysis.

We present a solution to an optimal stopping problem for a process with a wide-class of novel dynamics. The dynamics model the support/resistance line concept from financial technical analysis.

We show that when the price process $S$ represents a fully incomplete market, the optimal super-replication of any Markovian claim $g(S_T)$ with $g(\cdot)$ being nonnegative and lower semicontinuous is of buy-and-hold type. Since both (unbounded) stochastic volatility models and rough volatility models are examples of fully incomplete markets, one can interpret the buy-and-hold property when super-replicating Markovian claims as a natural phenomenon in incomplete markets.

We show that when the price process $S$ represents a fully incomplete market, the optimal super-replication of any Markovian claim $g(S_T)$ with $g(\cdot)$ being nonnegative and lower semicontinuous is of buy-and-hold type. Since both (unbounded) stochastic volatility models and rough volatility models are examples of fully incomplete markets, one can interpret the buy-and-hold property when super-replicating Markovian claims as a natural phenomenon in incomplete markets.