-

Let $\Omega$ be a Polish space with Borel $\sigma$-field $\mathcal{F}$ and

countably generated sub $\sigma$-field $\mathcal{G}\subset\mathcal{F}$. Denote

by $\mathcal{L}(\mathcal{F})$ the set of all bounded $\mathcal{F}$-upper

semianalytic functions from $\Omega$ to the reals and by

$\mathcal{L}(\mathcal{G})$ the subset of $\mathcal{G}$-upper semianalytic

functions. Let

$\mathcal{E}(\cdot|\mathcal{G})\colon\mathcal{L}(\mathcal{F})\to\mathcal{L}(\mathcal{G})$

be a sublinear increasing functional which leaves $\mathcal{L}(\mathcal{G})$

invariant. It is shown that there exists a $\mathcal{G}$-analytic set-valued

mapping $\mathcal{P}_{\mathcal{G}}$ from $\Omega$ to the set of probabilities

which are concentrated on atoms of $\mathcal{G}$ with compact convex values

such that $\mathcal{E}(X|\mathcal{G})(\omega)=$

$\sup_{P\in\mathcal{P}_{\mathcal{G}}(\omega)} E_P[X]$ if and only if

$\mathcal{E}(\cdot |\mathcal{G})$ is pointwise continuous from below and

continuous from above on the continuous functions. Further, given another

sublinear increasing functional

$\mathcal{E}(\cdot)\colon\mathcal{L}(\mathcal{F})\to\mathbb{R}$ which leaves

the constants invariant, the tower property

$\mathcal{E}(\cdot)=\mathcal{E}(\mathcal{E}(\cdot|\mathcal{G}))$ is

characterized via a pasting property of the representing sets of probabilities,

and the importance of analytic functions is explained. Finally, it is

characterized when a nonlinear version of Fubini's theorem holds true and when

the product of a set of probabilities and a set of kernels is compact.

-

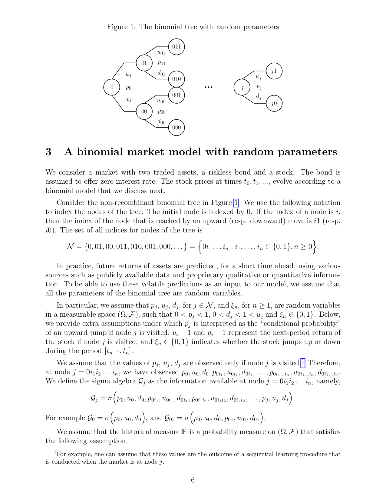

We introduce a new class of forward performance processes that are endogenous

and predictable with regards to an underlying market information set and,

furthermore, are updated at discrete times. We analyze in detail a binomial

model whose parameters are random and updated dynamically as the market

evolves. We show that the key step in the construction of the associated

predictable forward performance process is to solve a single-period inverse

investment problem, namely, to determine, period-by-period and conditionally on

the current market information, the end-time utility function from a given

initial-time value function. We reduce this inverse problem to solving a

functional equation and establish conditions for the existence and uniqueness

of its solutions in the class of inverse marginal functions.

-

Accounting for model uncertainty in risk management and option pricing leads

to infinite dimensional optimization problems which are both analytically and

numerically intractable. In this article we study when this hurdle can be

overcome for the so-called optimized certainty equivalent risk measure (OCE) --

including the average value-at-risk as a special case. First we focus on the

case where the uncertainty is modeled by a nonlinear expectation penalizing

distributions that are "far" in terms of optimal-transport distance

(Wasserstein distance for instance) from a given baseline distribution. It

turns out that the computation of the robust OCE reduces to a finite

dimensional problem, which in some cases can even be solved explicitly. This

principle also applies to the shortfall risk measure as well as for the pricing

of European options. Further, we derive convex dual representations of the

robust OCE for measurable claims without any assumptions on the set of

distributions. Finally, we give conditions on the latter set under which the

robust average value-at-risk is a tail risk measure.

-

We introduce a novel class of credit risk models in which the drift of the

survival process of a firm is a linear function of the factors. The prices of

defaultable bonds and credit default swaps (CDS) are linear-rational in the

factors. The price of a CDS option can be uniformly approximated by polynomials

in the factors. Multi-name models can produce simultaneous defaults, generate

positively as well as negatively correlated default intensities, and

accommodate stochastic interest rates. A calibration study illustrates the

versatility of these models by fitting CDS spread time series. A numerical

analysis validates the efficiency of the option price approximation method.

-

The financial crisis showed the importance of measuring, allocating and

regulating systemic risk. Recently, the systemic risk measures that can be

decomposed into an aggregation function and a scalar measure of risk, received

a lot of attention. In this framework, capital allocations are added after

aggregation and can represent bailout costs. More recently, a framework has

been introduced, where institutions are supplied with capital allocations

before aggregation. This yields an interpretation that is particularly useful

for regulatory purposes. In each framework, the set of all feasible capital

allocations leads to a multivariate risk measure. In this paper, we present

dual representations for scalar systemic risk measures as well as for the

corresponding multivariate risk measures concerning capital allocations. Our

results cover both frameworks: aggregating after allocating and allocating

after aggregation. As examples, we consider the aggregation mechanisms of the

Eisenberg-Noe model as well as those of the resource allocation and network

flow models.

-

We present a constructive and self-contained approach to data driven infinite

partition-of-unity copulas that were recently introduced in the literature. In

particular, we consider negative binomial and Poisson copulas and present a

solution to the problem of fitting such copulas to highly asymmetric data in

arbitrary dimensions.

-

We construct new multivariate copulas on the basis of a generalized infinite

partition-of-unity approach. This approach allows - in contrast to finite

partition-of-unity copulas - for tail-dependence as well as for asymmetry. A

possibility of fitting such copulas to real data from quantitative risk

management is also pointed out.

-

Determining risk contributions of unit exposures to portfolio-wide economic

capital is an important task in financial risk management. Computing risk

contributions involves difficulties caused by rare-event simulations. In this

study, we address the problem of estimating risk contributions when the total

risk is measured by value-at-risk (VaR). Our proposed estimator of VaR

contributions is based on the Metropolis-Hasting (MH) algorithm, which is one

of the most prevalent Markov chain Monte Carlo (MCMC) methods. Unlike existing

estimators, our MH-based estimator consists of samples from conditional loss

distribution given a rare event of interest. This feature enhances sample

efficiency compared with the crude Monte Carlo method. Moreover, our method has

the consistency and asymptotic normality, and is widely applicable to various

risk models having joint loss density. Our numerical experiments based on

simulation and real-world data demonstrate that in various risk models, even

those having high-dimensional (approximately 500) inhomogeneous margins, our MH

estimator has smaller bias and mean squared error compared with existing

estimators.

-

It has been understood that the "local" existence of the Markowitz' optimal

portfolio or the solution to the local-risk minimization problem is guaranteed

by some specific mathematical structures on the underlying assets price

processes known in the literature as "{\it Structure Conditions}". In this

paper, we consider a semi-martingale market model, and an arbitrary random time

that is not adapted to the information flow of the market model. This random

time may model the default time of a firm, the death time of an insured, or any

the occurrence time of an event that might impact the market model somehow. By

adding additional uncertainty to the market model, via this random time, the

{\it structures conditions} may fail and hence the Markowitz's optimal

portfolio and other quadratic-optimal portfolios might fail to exist. Our aim

is to investigate the impact of this random time on the structures conditions

from different perspectives. Our analysis allows us to conclude that under some

mild assumptions on the market model and the random time, these structures

conditions will remain valid on the one hand. Furthermore, we provide two

examples illustrating the importance of these assumptions. On the other hand,

we describe the random time models for which these structure conditions are

preserved for any market model. These results are elaborated separately for the

two contexts of stopping with the random time and incorporating totally a

specific class of random times respectively.

-

The aim of this paper is to quantify and manage systemic risk caused by

default contagion in the interbank market. We model the market as a random

directed network, where the vertices represent financial institutions and the

weighted edges monetary exposures between them. Our model captures the strong

degree of heterogeneity observed in empirical data and the parameters can

easily be fitted to real data sets. One of our main results allows us to

determine the impact of local shocks, where initially some banks default, to

the entire system and the wider economy. Here the impact is measured by some

index of total systemic importance of all eventually defaulted institutions. As

a central application, we characterize resilient and non-resilient cases. In

particular, for the prominent case where the network has a degree sequence

without second moment, we show that a small number of initially defaulted banks

can trigger a substantial default cascade. Our results complement and extend

significantly earlier findings derived in the configuration model where the

existence of a second moment of the degree distribution is assumed. As a second

main contribution, paralleling regulatory discussions, we determine minimal

capital requirements for financial institutions sufficient to make the network

resilient to small shocks. An appealing feature of these capital requirements

is that they can be determined locally by each institution without knowing the

complete network structure as they basically only depend on the institution's

exposures to its counterparties.

-

In a very high-dimensional vector space, two randomly-chosen vectors are

almost orthogonal with high probability. Starting from this observation, we

develop a statistical factor model, the random factor model, in which factors

are chosen at random based on the random projection method. Randomness of

factors has the consequence that covariance matrix is well preserved in a

linear factor representation. It also enables derivation of probabilistic

bounds for the accuracy of the random factor representation of time-series,

their cross-correlations and covariances. As an application, we analyze

reproduction of time-series and their cross-correlation coefficients in the

well-diversified Russell 3,000 equity index.

-

The utility of Potential Future Exposure (PFE) for counterparty trading

limits is being challenged by new market developments, notably widespread

regulatory Initial Margin (using 99% 10-day exposure), and netting of trade and

collateral flows. However PFE has pre-existing challenges w.r.t.

portfolios/distributions, collateralization, netting set seniority, and

overlaps with CVA. We introduce Potential Future Loss (PFL) which combines

expected shortfall (ES) and loss given default (LGD) as a replacement for PFE.

With two additional variants Adjusted PFL (aPFL) and Protected Adjusted PFL

(paPFL) these deal with both new and pre-existing challenges. We provide a

theoretical background and numerical examples.

-

We derive bounds on the distribution function, therefore also on the

Value-at-Risk, of $\varphi(\mathbf X)$ where $\varphi$ is an aggregation

function and $\mathbf X = (X_1,\dots,X_d)$ is a random vector with known

marginal distributions and partially known dependence structure. More

specifically, we analyze three types of available information on the dependence

structure: First, we consider the case where extreme value information, such as

the distributions of partial minima and maxima of $\mathbf X$, is available. In

order to include this information in the computation of Value-at-Risk bounds,

we utilize a reduction principle that relates this problem to an optimization

problem over a standard Fr\'echet class, which can then be solved by means of

the rearrangement algorithm or using analytical results. Second, we assume that

the copula of $\mathbf X$ is known on a subset of its domain, and finally we

consider the case where the copula of $\mathbf X$ lies in the vicinity of a

reference copula as measured by a statistical distance. In order to derive

Value-at-Risk bounds in the latter situations, we first improve the

Fr\'echet--Hoeffding bounds on copulas so as to include this additional

information on the dependence structure. Then, we translate the improved

Fr\'echet--Hoeffding bounds to bounds on the Value-at-Risk using the so-called

improved standard bounds. In numerical examples we illustrate that the

additional information typically leads to a significant improvement of the

bounds compared to the marginals-only case.

-

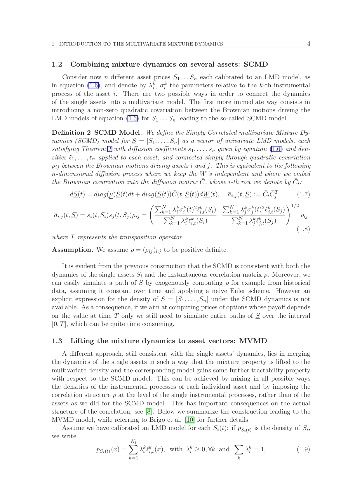

The Multi Variate Mixture Dynamics model is a tractable, dynamical,

arbitrage-free multivariate model characterized by transparency on the

dependence structure, since closed form formulae for terminal correlations,

average correlations and copula function are available. It also allows for

complete decorrelation between assets and instantaneous variances. Each single

asset is modelled according to a lognormal mixture dynamics model, and this

univariate version is widely used in the industry due to its flexibility and

accuracy. The same property holds for the multivariate process of all assets,

whose density is a mixture of multivariate basic densities. This allows for

consistency of single asset and index/portfolio smile. In this paper, we

generalize the MVMD model by introducing shifted dynamics and we propose a

definition of implied correlation under this model. We investigate whether the

model is able to consistently reproduce the implied volatility of FX cross

rates once the single components are calibrated to univariate shifted lognormal

mixture dynamics models. We consider in particular the case of the Chinese

renminbi FX rate, showing that the shifted MVMD model correctly recovers the

CNY/EUR smile given the EUR/USD smile and the USD/CNY smile, thus highlighting

that the model can also work as an arbitrage free volatility smile

extrapolation tool for cross currencies that may not be liquid or fully

observable. We compare the performance of the shifted MVMD model in terms of

implied correlation with those of the shifted Simply Correlated Mixture

Dynamics model where the dynamics of the single assets are connected naively by

introducing correlation among their Brownian motions. Finally, we introduce a

model with uncertain volatilities and correlation. The Markovian projection of

this model is a generalization of the shifted MVMD model.

-

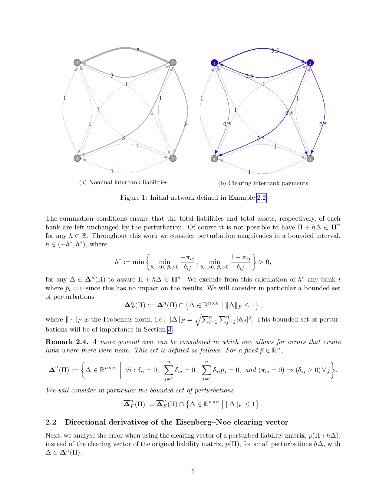

We quantify the sensitivity of the Eisenberg-Noe clearing vector to

estimation errors in the bilateral liabilities of a financial system in a

stylized setting. The interbank liabilities matrix is a crucial input to the

computation of the clearing vector. However, in practice central bankers and

regulators must often estimate this matrix because complete information on

bilateral liabilities is rarely available. As a result, the clearing vector may

suffer from estimation errors in the liabilities matrix. We quantify the

clearing vector's sensitivity to such estimation errors and show that its

directional derivatives are, like the clearing vector itself, solutions of

fixed point equations. We describe estimation errors utilizing a basis for the

space of matrices representing permissible perturbations and derive analytical

solutions to the maximal deviations of the Eisenberg-Noe clearing vector. This

allows us to compute upper bounds for the worst case perturbations of the

clearing vector in our simple setting. Moreover, we quantify the probability of

observing clearing vector deviations of a certain magnitude, for uniformly or

normally distributed errors in the relative liability matrix.

Applying our methodology to a dataset of European banks, we find that

perturbations to the relative liabilities can result in economically sizeable

differences that could lead to an underestimation of the risk of contagion. Our

results are a first step towards allowing regulators to quantify errors in

their simulations.

-

In our model, private actors with interbank cash flows similar to, but nore

general than (Carmona, Fouque, Sun, 2013) borrow from the outside economy at a

certain interest rate, controlled by the central bank, and invest in risky

assets. Each private actor aims to maximize its expected terminal logarithmic

utility. The central bank, in turn, aims to control the overall economy by

means of an exponential utility function. We solve all stochastic optimal

control problems explicitly. We are able to recreate occasions such as

liquidity trap. We study distribution of the number of defaults (net worth of a

private actor going below a certain threshold).

-

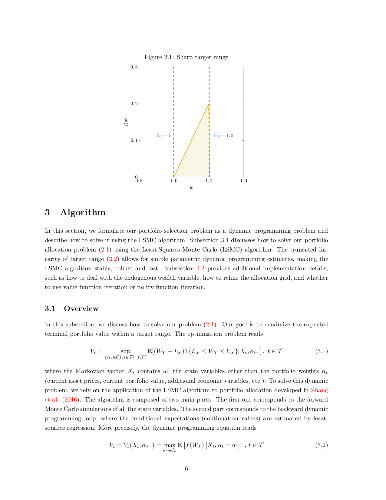

In this paper, we propose a novel investment strategy for portfolio

optimization problems. The proposed strategy maximizes the expected portfolio

value bounded within a targeted range, composed of a conservative lower target

representing a need for capital protection and a desired upper target

representing an investment goal. This strategy favorably shapes the entire

probability distribution of returns, as it simultaneously seeks a desired

expected return, cuts off downside risk and implicitly caps volatility and

higher moments. To illustrate the effectiveness of this investment strategy, we

study a multiperiod portfolio optimization problem with transaction costs and

develop a two-stage regression approach that improves the classical least

squares Monte Carlo (LSMC) algorithm when dealing with difficult payoffs, such

as highly concave, abruptly changing or discontinuous functions. Our numerical

results show substantial improvements over the classical LSMC algorithm for

both the constant relative risk-aversion (CRRA) utility approach and the

proposed skewed target range strategy (STRS). Our numerical results illustrate

the ability of the STRS to contain the portfolio value within the targeted

range. When compared with the CRRA utility approach, the STRS achieves a

similar mean-variance efficient frontier while delivering a better downside

risk-return trade-off.

-

We propose a novel credit default model that takes into account the impact of

macroeconomic information and contagion effect on the defaults of obligors. We

use a set-valued Markov chain to model the default process, which is the set of

all defaulted obligors in the group. We obtain analytic characterizations for

the default process, and use them to derive pricing formulas in explicit forms

for synthetic collateralized debt obligations (CDOs). Furthermore, we use

market data to calibrate the model and conduct numerical studies on the tranche

spreads of CDOs. We find evidence to support that systematic default risk

coupled with default contagion could have the leading component of the total

default risk.

-

We propose a robust risk measurement approach that minimizes the expectation

of overestimation plus underestimation costs. We consider uncertainty by taking

the supremum over a collection of probability measures, relating our approach

to dual sets in the representation of coherent risk measures. We provide

results that guarantee the existence of a solution and explore the properties

of minimizer and minimum as risk and deviation measures, respectively. An

empirical illustration is carried out to demonstrate the use of our approach in

capital determination.

-

We propose a new backtesting framework for Expected Shortfall that could be

used by the regulator. Instead of looking at the estimated capital reserve and

the realised cash-flow separately, one could bind them into the secured

position, for which risk measurement is much easier. Using this simple concept

combined with monotonicity of Expected Shortfall with respect to its target

confidence level we introduce a natural and efficient backtesting framework.

Our test statistics is given by the biggest number of worst realisations for

the secured position that add up to a negative total. Surprisingly, this simple

quantity could be used to construct an efficient backtesting framework for

unconditional coverage of Expected Shortfall in a natural extension of the

regulatory traffic-light approach for Value-at-Risk. While being easy to

calculate, the test statistic is based on the underlying duality between

coherent risk measures and scale-invariant performance measures.

-

We study a class of backtests for forecast distributions in which the test

statistic depends on a spectral transformation that weights exceedance events

by a function of the modeled probability level. The weighting scheme is

specified by a kernel measure which makes explicit the user's priorities for

model performance. The class of spectral backtests includes tests of

unconditional coverage and tests of conditional coverage. We show how the class

embeds a wide variety of backtests in the existing literature, and further

propose novel variants which are easily implemented, well-sized and have good

power. In an empirical application, we backtest forecast distributions for the

overnight P&L of ten bank trading portfolios. For some portfolios, test results

depend materially on the choice of kernel.

-

Assessing systemic risk in financial markets is of great importance but it

often requires data that are unavailable or available at a very low frequency.

For this reason, systemic risk assessment with partial information is

potentially very useful for regulators and other stakeholders. In this paper we

consider systemic risk due to fire sales spillover and portfolio rebalancing by

using the risk metrics defined by Greenwood et al. (2015). By using the Maximum

Entropy principle we propose a method to assess aggregated and single bank's

systemicness and vulnerability and to statistically test for a change in these

variables when only the information on the size of each bank and the

capitalization of the investment assets are available. We prove the

effectiveness of our method on 2001-2013 quarterly data of US banks for which

portfolio composition is available.

-

Accounting for the non-normality of asset returns remains challenging in

robust portfolio optimization. In this article, we tackle this problem by

assessing the risk of the portfolio through the "amount of randomness" conveyed

by its returns. We achieve this by using an objective function that relies on

the exponential of R\'enyi entropy, an information-theoretic criterion that

precisely quantifies the uncertainty embedded in a distribution, accounting for

higher-order moments. Compared to Shannon entropy, R\'enyi entropy features a

parameter that can be tuned to play around the notion of uncertainty. A

Gram-Charlier expansion shows that it controls the relative contributions of

the central (variance) and tail (kurtosis) parts of the distribution in the

measure. We further rely on a non-parametric estimator of the exponential

R\'enyi entropy that extends a robust sample-spacings estimator initially

designed for Shannon entropy. A portfolio selection application illustrates

that minimizing R\'enyi entropy yields portfolios that outperform

state-of-the-art minimum variance portfolios in terms of risk-return-turnover

trade-off.

-

This paper provides a general framework for modeling financial contagion in a

system with obligations in multiple illiquid assets (e.g., currencies). In so

doing, we develop a multi-layered financial network that extends the single

network of Eisenberg and Noe (2001). In particular, we develop a financial

contagion model with fire sales that allows institutions to both buy and sell

assets to cover their liabilities in the different assets and act as utility

maximizers.

We prove that, under standard assumptions and without market impacts,

equilibrium portfolio holdings exist and are unique. However, with market

impacts, we prove that equilibrium portfolio holdings and market prices exist

which clear the multi-layered financial system. In general, though, these

clearing solutions are not unique. We extend this result by considering the

t\^atonnement process to find the unique attained equilibrium. The attained

equilibrium need not be continuous with respect to the initial shock; these

points of discontinuity match those stresses in which a financial crisis

becomes a systemic crisis. We further provide mathematical formulations for

payment rules and utility functions satisfying the necessary conditions for

these existence and uniqueness results.

We demonstrate the value of our model through illustrative numerical case

studies. In particular, we study a counterfactual scenario on the event that

Greece re-instituted the drachma on a dataset from the European Banking

Authority.

-

This paper studies the optimal dividend problem with capital injection under

the constraint that the cumulative dividend strategy is absolutely continuous.

We consider an open problem of the general spectrally negative case and derive

the optimal solution explicitly using the fluctuation identities of the

refracted-reflected L\'evy process. The optimal strategy as well as the value

function are concisely written in terms of the scale function. Numerical

results are also provided to confirm the analytical conclusions.

Let $\Omega$ be a Polish space with Borel $\sigma$-field $\mathcal{F}$ and countably generated sub $\sigma$-field $\mathcal{G}\subset\mathcal{F}$. Denote by $\mathcal{L}(\mathcal{F})$ the set of all bounded $\mathcal{F}$-upper semianalytic functions from $\Omega$ to the reals and by $\mathcal{L}(\mathcal{G})$ the subset of $\mathcal{G}$-upper semianalytic functions. Let $\mathcal{E}(\cdot|\mathcal{G})\colon\mathcal{L}(\mathcal{F})\to\mathcal{L}(\mathcal{G})$ be a sublinear increasing functional which leaves $\mathcal{L}(\mathcal{G})$ invariant. It is shown that there exists a $\mathcal{G}$-analytic set-valued mapping $\mathcal{P}_{\mathcal{G}}$ from $\Omega$ to the set of probabilities which are concentrated on atoms of $\mathcal{G}$ with compact convex values such that $\mathcal{E}(X|\mathcal{G})(\omega)=$ $\sup_{P\in\mathcal{P}_{\mathcal{G}}(\omega)} E_P[X]$ if and only if $\mathcal{E}(\cdot |\mathcal{G})$ is pointwise continuous from below and continuous from above on the continuous functions. Further, given another sublinear increasing functional $\mathcal{E}(\cdot)\colon\mathcal{L}(\mathcal{F})\to\mathbb{R}$ which leaves the constants invariant, the tower property $\mathcal{E}(\cdot)=\mathcal{E}(\mathcal{E}(\cdot|\mathcal{G}))$ is characterized via a pasting property of the representing sets of probabilities, and the importance of analytic functions is explained. Finally, it is characterized when a nonlinear version of Fubini's theorem holds true and when the product of a set of probabilities and a set of kernels is compact.

Let $\Omega$ be a Polish space with Borel $\sigma$-field $\mathcal{F}$ and countably generated sub $\sigma$-field $\mathcal{G}\subset\mathcal{F}$. Denote by $\mathcal{L}(\mathcal{F})$ the set of all bounded $\mathcal{F}$-upper semianalytic functions from $\Omega$ to the reals and by $\mathcal{L}(\mathcal{G})$ the subset of $\mathcal{G}$-upper semianalytic functions. Let $\mathcal{E}(\cdot|\mathcal{G})\colon\mathcal{L}(\mathcal{F})\to\mathcal{L}(\mathcal{G})$ be a sublinear increasing functional which leaves $\mathcal{L}(\mathcal{G})$ invariant. It is shown that there exists a $\mathcal{G}$-analytic set-valued mapping $\mathcal{P}_{\mathcal{G}}$ from $\Omega$ to the set of probabilities which are concentrated on atoms of $\mathcal{G}$ with compact convex values such that $\mathcal{E}(X|\mathcal{G})(\omega)=$ $\sup_{P\in\mathcal{P}_{\mathcal{G}}(\omega)} E_P[X]$ if and only if $\mathcal{E}(\cdot |\mathcal{G})$ is pointwise continuous from below and continuous from above on the continuous functions. Further, given another sublinear increasing functional $\mathcal{E}(\cdot)\colon\mathcal{L}(\mathcal{F})\to\mathbb{R}$ which leaves the constants invariant, the tower property $\mathcal{E}(\cdot)=\mathcal{E}(\mathcal{E}(\cdot|\mathcal{G}))$ is characterized via a pasting property of the representing sets of probabilities, and the importance of analytic functions is explained. Finally, it is characterized when a nonlinear version of Fubini's theorem holds true and when the product of a set of probabilities and a set of kernels is compact.

We introduce a new class of forward performance processes that are endogenous and predictable with regards to an underlying market information set and, furthermore, are updated at discrete times. We analyze in detail a binomial model whose parameters are random and updated dynamically as the market evolves. We show that the key step in the construction of the associated predictable forward performance process is to solve a single-period inverse investment problem, namely, to determine, period-by-period and conditionally on the current market information, the end-time utility function from a given initial-time value function. We reduce this inverse problem to solving a functional equation and establish conditions for the existence and uniqueness of its solutions in the class of inverse marginal functions.

We introduce a new class of forward performance processes that are endogenous and predictable with regards to an underlying market information set and, furthermore, are updated at discrete times. We analyze in detail a binomial model whose parameters are random and updated dynamically as the market evolves. We show that the key step in the construction of the associated predictable forward performance process is to solve a single-period inverse investment problem, namely, to determine, period-by-period and conditionally on the current market information, the end-time utility function from a given initial-time value function. We reduce this inverse problem to solving a functional equation and establish conditions for the existence and uniqueness of its solutions in the class of inverse marginal functions.

Accounting for model uncertainty in risk management and option pricing leads to infinite dimensional optimization problems which are both analytically and numerically intractable. In this article we study when this hurdle can be overcome for the so-called optimized certainty equivalent risk measure (OCE) -- including the average value-at-risk as a special case. First we focus on the case where the uncertainty is modeled by a nonlinear expectation penalizing distributions that are "far" in terms of optimal-transport distance (Wasserstein distance for instance) from a given baseline distribution. It turns out that the computation of the robust OCE reduces to a finite dimensional problem, which in some cases can even be solved explicitly. This principle also applies to the shortfall risk measure as well as for the pricing of European options. Further, we derive convex dual representations of the robust OCE for measurable claims without any assumptions on the set of distributions. Finally, we give conditions on the latter set under which the robust average value-at-risk is a tail risk measure.

Accounting for model uncertainty in risk management and option pricing leads to infinite dimensional optimization problems which are both analytically and numerically intractable. In this article we study when this hurdle can be overcome for the so-called optimized certainty equivalent risk measure (OCE) -- including the average value-at-risk as a special case. First we focus on the case where the uncertainty is modeled by a nonlinear expectation penalizing distributions that are "far" in terms of optimal-transport distance (Wasserstein distance for instance) from a given baseline distribution. It turns out that the computation of the robust OCE reduces to a finite dimensional problem, which in some cases can even be solved explicitly. This principle also applies to the shortfall risk measure as well as for the pricing of European options. Further, we derive convex dual representations of the robust OCE for measurable claims without any assumptions on the set of distributions. Finally, we give conditions on the latter set under which the robust average value-at-risk is a tail risk measure.

We introduce a novel class of credit risk models in which the drift of the survival process of a firm is a linear function of the factors. The prices of defaultable bonds and credit default swaps (CDS) are linear-rational in the factors. The price of a CDS option can be uniformly approximated by polynomials in the factors. Multi-name models can produce simultaneous defaults, generate positively as well as negatively correlated default intensities, and accommodate stochastic interest rates. A calibration study illustrates the versatility of these models by fitting CDS spread time series. A numerical analysis validates the efficiency of the option price approximation method.

We introduce a novel class of credit risk models in which the drift of the survival process of a firm is a linear function of the factors. The prices of defaultable bonds and credit default swaps (CDS) are linear-rational in the factors. The price of a CDS option can be uniformly approximated by polynomials in the factors. Multi-name models can produce simultaneous defaults, generate positively as well as negatively correlated default intensities, and accommodate stochastic interest rates. A calibration study illustrates the versatility of these models by fitting CDS spread time series. A numerical analysis validates the efficiency of the option price approximation method.

Determining risk contributions of unit exposures to portfolio-wide economic capital is an important task in financial risk management. Computing risk contributions involves difficulties caused by rare-event simulations. In this study, we address the problem of estimating risk contributions when the total risk is measured by value-at-risk (VaR). Our proposed estimator of VaR contributions is based on the Metropolis-Hasting (MH) algorithm, which is one of the most prevalent Markov chain Monte Carlo (MCMC) methods. Unlike existing estimators, our MH-based estimator consists of samples from conditional loss distribution given a rare event of interest. This feature enhances sample efficiency compared with the crude Monte Carlo method. Moreover, our method has the consistency and asymptotic normality, and is widely applicable to various risk models having joint loss density. Our numerical experiments based on simulation and real-world data demonstrate that in various risk models, even those having high-dimensional (approximately 500) inhomogeneous margins, our MH estimator has smaller bias and mean squared error compared with existing estimators.

Determining risk contributions of unit exposures to portfolio-wide economic capital is an important task in financial risk management. Computing risk contributions involves difficulties caused by rare-event simulations. In this study, we address the problem of estimating risk contributions when the total risk is measured by value-at-risk (VaR). Our proposed estimator of VaR contributions is based on the Metropolis-Hasting (MH) algorithm, which is one of the most prevalent Markov chain Monte Carlo (MCMC) methods. Unlike existing estimators, our MH-based estimator consists of samples from conditional loss distribution given a rare event of interest. This feature enhances sample efficiency compared with the crude Monte Carlo method. Moreover, our method has the consistency and asymptotic normality, and is widely applicable to various risk models having joint loss density. Our numerical experiments based on simulation and real-world data demonstrate that in various risk models, even those having high-dimensional (approximately 500) inhomogeneous margins, our MH estimator has smaller bias and mean squared error compared with existing estimators.

In a very high-dimensional vector space, two randomly-chosen vectors are almost orthogonal with high probability. Starting from this observation, we develop a statistical factor model, the random factor model, in which factors are chosen at random based on the random projection method. Randomness of factors has the consequence that covariance matrix is well preserved in a linear factor representation. It also enables derivation of probabilistic bounds for the accuracy of the random factor representation of time-series, their cross-correlations and covariances. As an application, we analyze reproduction of time-series and their cross-correlation coefficients in the well-diversified Russell 3,000 equity index.

In a very high-dimensional vector space, two randomly-chosen vectors are almost orthogonal with high probability. Starting from this observation, we develop a statistical factor model, the random factor model, in which factors are chosen at random based on the random projection method. Randomness of factors has the consequence that covariance matrix is well preserved in a linear factor representation. It also enables derivation of probabilistic bounds for the accuracy of the random factor representation of time-series, their cross-correlations and covariances. As an application, we analyze reproduction of time-series and their cross-correlation coefficients in the well-diversified Russell 3,000 equity index.

The Multi Variate Mixture Dynamics model is a tractable, dynamical, arbitrage-free multivariate model characterized by transparency on the dependence structure, since closed form formulae for terminal correlations, average correlations and copula function are available. It also allows for complete decorrelation between assets and instantaneous variances. Each single asset is modelled according to a lognormal mixture dynamics model, and this univariate version is widely used in the industry due to its flexibility and accuracy. The same property holds for the multivariate process of all assets, whose density is a mixture of multivariate basic densities. This allows for consistency of single asset and index/portfolio smile. In this paper, we generalize the MVMD model by introducing shifted dynamics and we propose a definition of implied correlation under this model. We investigate whether the model is able to consistently reproduce the implied volatility of FX cross rates once the single components are calibrated to univariate shifted lognormal mixture dynamics models. We consider in particular the case of the Chinese renminbi FX rate, showing that the shifted MVMD model correctly recovers the CNY/EUR smile given the EUR/USD smile and the USD/CNY smile, thus highlighting that the model can also work as an arbitrage free volatility smile extrapolation tool for cross currencies that may not be liquid or fully observable. We compare the performance of the shifted MVMD model in terms of implied correlation with those of the shifted Simply Correlated Mixture Dynamics model where the dynamics of the single assets are connected naively by introducing correlation among their Brownian motions. Finally, we introduce a model with uncertain volatilities and correlation. The Markovian projection of this model is a generalization of the shifted MVMD model.

The Multi Variate Mixture Dynamics model is a tractable, dynamical, arbitrage-free multivariate model characterized by transparency on the dependence structure, since closed form formulae for terminal correlations, average correlations and copula function are available. It also allows for complete decorrelation between assets and instantaneous variances. Each single asset is modelled according to a lognormal mixture dynamics model, and this univariate version is widely used in the industry due to its flexibility and accuracy. The same property holds for the multivariate process of all assets, whose density is a mixture of multivariate basic densities. This allows for consistency of single asset and index/portfolio smile. In this paper, we generalize the MVMD model by introducing shifted dynamics and we propose a definition of implied correlation under this model. We investigate whether the model is able to consistently reproduce the implied volatility of FX cross rates once the single components are calibrated to univariate shifted lognormal mixture dynamics models. We consider in particular the case of the Chinese renminbi FX rate, showing that the shifted MVMD model correctly recovers the CNY/EUR smile given the EUR/USD smile and the USD/CNY smile, thus highlighting that the model can also work as an arbitrage free volatility smile extrapolation tool for cross currencies that may not be liquid or fully observable. We compare the performance of the shifted MVMD model in terms of implied correlation with those of the shifted Simply Correlated Mixture Dynamics model where the dynamics of the single assets are connected naively by introducing correlation among their Brownian motions. Finally, we introduce a model with uncertain volatilities and correlation. The Markovian projection of this model is a generalization of the shifted MVMD model.

We quantify the sensitivity of the Eisenberg-Noe clearing vector to estimation errors in the bilateral liabilities of a financial system in a stylized setting. The interbank liabilities matrix is a crucial input to the computation of the clearing vector. However, in practice central bankers and regulators must often estimate this matrix because complete information on bilateral liabilities is rarely available. As a result, the clearing vector may suffer from estimation errors in the liabilities matrix. We quantify the clearing vector's sensitivity to such estimation errors and show that its directional derivatives are, like the clearing vector itself, solutions of fixed point equations. We describe estimation errors utilizing a basis for the space of matrices representing permissible perturbations and derive analytical solutions to the maximal deviations of the Eisenberg-Noe clearing vector. This allows us to compute upper bounds for the worst case perturbations of the clearing vector in our simple setting. Moreover, we quantify the probability of observing clearing vector deviations of a certain magnitude, for uniformly or normally distributed errors in the relative liability matrix. Applying our methodology to a dataset of European banks, we find that perturbations to the relative liabilities can result in economically sizeable differences that could lead to an underestimation of the risk of contagion. Our results are a first step towards allowing regulators to quantify errors in their simulations.

We quantify the sensitivity of the Eisenberg-Noe clearing vector to estimation errors in the bilateral liabilities of a financial system in a stylized setting. The interbank liabilities matrix is a crucial input to the computation of the clearing vector. However, in practice central bankers and regulators must often estimate this matrix because complete information on bilateral liabilities is rarely available. As a result, the clearing vector may suffer from estimation errors in the liabilities matrix. We quantify the clearing vector's sensitivity to such estimation errors and show that its directional derivatives are, like the clearing vector itself, solutions of fixed point equations. We describe estimation errors utilizing a basis for the space of matrices representing permissible perturbations and derive analytical solutions to the maximal deviations of the Eisenberg-Noe clearing vector. This allows us to compute upper bounds for the worst case perturbations of the clearing vector in our simple setting. Moreover, we quantify the probability of observing clearing vector deviations of a certain magnitude, for uniformly or normally distributed errors in the relative liability matrix. Applying our methodology to a dataset of European banks, we find that perturbations to the relative liabilities can result in economically sizeable differences that could lead to an underestimation of the risk of contagion. Our results are a first step towards allowing regulators to quantify errors in their simulations.

In our model, private actors with interbank cash flows similar to, but nore general than (Carmona, Fouque, Sun, 2013) borrow from the outside economy at a certain interest rate, controlled by the central bank, and invest in risky assets. Each private actor aims to maximize its expected terminal logarithmic utility. The central bank, in turn, aims to control the overall economy by means of an exponential utility function. We solve all stochastic optimal control problems explicitly. We are able to recreate occasions such as liquidity trap. We study distribution of the number of defaults (net worth of a private actor going below a certain threshold).

In our model, private actors with interbank cash flows similar to, but nore general than (Carmona, Fouque, Sun, 2013) borrow from the outside economy at a certain interest rate, controlled by the central bank, and invest in risky assets. Each private actor aims to maximize its expected terminal logarithmic utility. The central bank, in turn, aims to control the overall economy by means of an exponential utility function. We solve all stochastic optimal control problems explicitly. We are able to recreate occasions such as liquidity trap. We study distribution of the number of defaults (net worth of a private actor going below a certain threshold).

In this paper, we propose a novel investment strategy for portfolio optimization problems. The proposed strategy maximizes the expected portfolio value bounded within a targeted range, composed of a conservative lower target representing a need for capital protection and a desired upper target representing an investment goal. This strategy favorably shapes the entire probability distribution of returns, as it simultaneously seeks a desired expected return, cuts off downside risk and implicitly caps volatility and higher moments. To illustrate the effectiveness of this investment strategy, we study a multiperiod portfolio optimization problem with transaction costs and develop a two-stage regression approach that improves the classical least squares Monte Carlo (LSMC) algorithm when dealing with difficult payoffs, such as highly concave, abruptly changing or discontinuous functions. Our numerical results show substantial improvements over the classical LSMC algorithm for both the constant relative risk-aversion (CRRA) utility approach and the proposed skewed target range strategy (STRS). Our numerical results illustrate the ability of the STRS to contain the portfolio value within the targeted range. When compared with the CRRA utility approach, the STRS achieves a similar mean-variance efficient frontier while delivering a better downside risk-return trade-off.

In this paper, we propose a novel investment strategy for portfolio optimization problems. The proposed strategy maximizes the expected portfolio value bounded within a targeted range, composed of a conservative lower target representing a need for capital protection and a desired upper target representing an investment goal. This strategy favorably shapes the entire probability distribution of returns, as it simultaneously seeks a desired expected return, cuts off downside risk and implicitly caps volatility and higher moments. To illustrate the effectiveness of this investment strategy, we study a multiperiod portfolio optimization problem with transaction costs and develop a two-stage regression approach that improves the classical least squares Monte Carlo (LSMC) algorithm when dealing with difficult payoffs, such as highly concave, abruptly changing or discontinuous functions. Our numerical results show substantial improvements over the classical LSMC algorithm for both the constant relative risk-aversion (CRRA) utility approach and the proposed skewed target range strategy (STRS). Our numerical results illustrate the ability of the STRS to contain the portfolio value within the targeted range. When compared with the CRRA utility approach, the STRS achieves a similar mean-variance efficient frontier while delivering a better downside risk-return trade-off.

We propose a robust risk measurement approach that minimizes the expectation of overestimation plus underestimation costs. We consider uncertainty by taking the supremum over a collection of probability measures, relating our approach to dual sets in the representation of coherent risk measures. We provide results that guarantee the existence of a solution and explore the properties of minimizer and minimum as risk and deviation measures, respectively. An empirical illustration is carried out to demonstrate the use of our approach in capital determination.

We propose a robust risk measurement approach that minimizes the expectation of overestimation plus underestimation costs. We consider uncertainty by taking the supremum over a collection of probability measures, relating our approach to dual sets in the representation of coherent risk measures. We provide results that guarantee the existence of a solution and explore the properties of minimizer and minimum as risk and deviation measures, respectively. An empirical illustration is carried out to demonstrate the use of our approach in capital determination.

We study a class of backtests for forecast distributions in which the test statistic depends on a spectral transformation that weights exceedance events by a function of the modeled probability level. The weighting scheme is specified by a kernel measure which makes explicit the user's priorities for model performance. The class of spectral backtests includes tests of unconditional coverage and tests of conditional coverage. We show how the class embeds a wide variety of backtests in the existing literature, and further propose novel variants which are easily implemented, well-sized and have good power. In an empirical application, we backtest forecast distributions for the overnight P&L of ten bank trading portfolios. For some portfolios, test results depend materially on the choice of kernel.

We study a class of backtests for forecast distributions in which the test statistic depends on a spectral transformation that weights exceedance events by a function of the modeled probability level. The weighting scheme is specified by a kernel measure which makes explicit the user's priorities for model performance. The class of spectral backtests includes tests of unconditional coverage and tests of conditional coverage. We show how the class embeds a wide variety of backtests in the existing literature, and further propose novel variants which are easily implemented, well-sized and have good power. In an empirical application, we backtest forecast distributions for the overnight P&L of ten bank trading portfolios. For some portfolios, test results depend materially on the choice of kernel.

Assessing systemic risk in financial markets is of great importance but it often requires data that are unavailable or available at a very low frequency. For this reason, systemic risk assessment with partial information is potentially very useful for regulators and other stakeholders. In this paper we consider systemic risk due to fire sales spillover and portfolio rebalancing by using the risk metrics defined by Greenwood et al. (2015). By using the Maximum Entropy principle we propose a method to assess aggregated and single bank's systemicness and vulnerability and to statistically test for a change in these variables when only the information on the size of each bank and the capitalization of the investment assets are available. We prove the effectiveness of our method on 2001-2013 quarterly data of US banks for which portfolio composition is available.

Assessing systemic risk in financial markets is of great importance but it often requires data that are unavailable or available at a very low frequency. For this reason, systemic risk assessment with partial information is potentially very useful for regulators and other stakeholders. In this paper we consider systemic risk due to fire sales spillover and portfolio rebalancing by using the risk metrics defined by Greenwood et al. (2015). By using the Maximum Entropy principle we propose a method to assess aggregated and single bank's systemicness and vulnerability and to statistically test for a change in these variables when only the information on the size of each bank and the capitalization of the investment assets are available. We prove the effectiveness of our method on 2001-2013 quarterly data of US banks for which portfolio composition is available.

Accounting for the non-normality of asset returns remains challenging in robust portfolio optimization. In this article, we tackle this problem by assessing the risk of the portfolio through the "amount of randomness" conveyed by its returns. We achieve this by using an objective function that relies on the exponential of R\'enyi entropy, an information-theoretic criterion that precisely quantifies the uncertainty embedded in a distribution, accounting for higher-order moments. Compared to Shannon entropy, R\'enyi entropy features a parameter that can be tuned to play around the notion of uncertainty. A Gram-Charlier expansion shows that it controls the relative contributions of the central (variance) and tail (kurtosis) parts of the distribution in the measure. We further rely on a non-parametric estimator of the exponential R\'enyi entropy that extends a robust sample-spacings estimator initially designed for Shannon entropy. A portfolio selection application illustrates that minimizing R\'enyi entropy yields portfolios that outperform state-of-the-art minimum variance portfolios in terms of risk-return-turnover trade-off.

Accounting for the non-normality of asset returns remains challenging in robust portfolio optimization. In this article, we tackle this problem by assessing the risk of the portfolio through the "amount of randomness" conveyed by its returns. We achieve this by using an objective function that relies on the exponential of R\'enyi entropy, an information-theoretic criterion that precisely quantifies the uncertainty embedded in a distribution, accounting for higher-order moments. Compared to Shannon entropy, R\'enyi entropy features a parameter that can be tuned to play around the notion of uncertainty. A Gram-Charlier expansion shows that it controls the relative contributions of the central (variance) and tail (kurtosis) parts of the distribution in the measure. We further rely on a non-parametric estimator of the exponential R\'enyi entropy that extends a robust sample-spacings estimator initially designed for Shannon entropy. A portfolio selection application illustrates that minimizing R\'enyi entropy yields portfolios that outperform state-of-the-art minimum variance portfolios in terms of risk-return-turnover trade-off.

This paper provides a general framework for modeling financial contagion in a system with obligations in multiple illiquid assets (e.g., currencies). In so doing, we develop a multi-layered financial network that extends the single network of Eisenberg and Noe (2001). In particular, we develop a financial contagion model with fire sales that allows institutions to both buy and sell assets to cover their liabilities in the different assets and act as utility maximizers. We prove that, under standard assumptions and without market impacts, equilibrium portfolio holdings exist and are unique. However, with market impacts, we prove that equilibrium portfolio holdings and market prices exist which clear the multi-layered financial system. In general, though, these clearing solutions are not unique. We extend this result by considering the t\^atonnement process to find the unique attained equilibrium. The attained equilibrium need not be continuous with respect to the initial shock; these points of discontinuity match those stresses in which a financial crisis becomes a systemic crisis. We further provide mathematical formulations for payment rules and utility functions satisfying the necessary conditions for these existence and uniqueness results. We demonstrate the value of our model through illustrative numerical case studies. In particular, we study a counterfactual scenario on the event that Greece re-instituted the drachma on a dataset from the European Banking Authority.

This paper provides a general framework for modeling financial contagion in a system with obligations in multiple illiquid assets (e.g., currencies). In so doing, we develop a multi-layered financial network that extends the single network of Eisenberg and Noe (2001). In particular, we develop a financial contagion model with fire sales that allows institutions to both buy and sell assets to cover their liabilities in the different assets and act as utility maximizers. We prove that, under standard assumptions and without market impacts, equilibrium portfolio holdings exist and are unique. However, with market impacts, we prove that equilibrium portfolio holdings and market prices exist which clear the multi-layered financial system. In general, though, these clearing solutions are not unique. We extend this result by considering the t\^atonnement process to find the unique attained equilibrium. The attained equilibrium need not be continuous with respect to the initial shock; these points of discontinuity match those stresses in which a financial crisis becomes a systemic crisis. We further provide mathematical formulations for payment rules and utility functions satisfying the necessary conditions for these existence and uniqueness results. We demonstrate the value of our model through illustrative numerical case studies. In particular, we study a counterfactual scenario on the event that Greece re-instituted the drachma on a dataset from the European Banking Authority.