-

Semidefinite programs (SDPs) -- some of the most useful and versatile

optimization problems of the last few decades -- are often pathological: the

optimal values of the primal and dual problems may differ and may not be

attained. Such SDPs are both theoretically interesting and often impossible to

solve; yet, the pathological SDPs in the literature look strikingly similar.

Based on our recent work \cite{Pataki:17} we characterize pathological

semidefinite systems by certain {\em excluded matrices}, which are easy to spot

in all published examples. Our main tool is a normal (canonical) form of

semidefinite systems, which makes their pathological behavior easy to verify.

The normal form is constructed in a surprisingly simple fashion, using mostly

elementary row operations inherited from Gaussian elimination. The proofs are

elementary and can be followed by a reader at the advanced undergraduate level.

As a byproduct, we show how to transform any linear map acting on symmetric

matrices into a normal form, which allows us to quickly check whether the image

of the semidefinite cone under the map is closed. We can thus introduce readers

to a fundamental issue in convex analysis: the linear image of a closed convex

set may not be closed, and often simple conditions are available to verify the

closedness, or lack of it.

-

LaSalle invariance principle was originally proposed in the 1950's and has

become a fundamental mathematical tool in the area of dynamical systems and

control. In both theoretical research and engineering practice, discrete-time

dynamical systems have been at least as extensively studied as continuous-time

systems. For example, model predictive control is typically studied in

discrete-time via Lyapunov methods. However, there is a peculiar absence in the

standard literature of standard treatments of Lyapunov functions and LaSalle

invariance principle for discrete-time nonlinear systems. Most of the textbooks

on nonlinear dynamical systems focus only on continuous-time systems. In

Chapter 1 of the book by LaSalle [11], the author establishes the LaSalle

invariance principle for difference equation systems. However, all the useful

lemmas in [11] are given in the form of exercises with no proof provided. In

this document, we provide the proofs of all the lemmas proposed in [11] that

are needed to derive the main theorem on the LaSalle invariance principle for

discrete-time dynamical systems. We organize all the materials in a

self-contained manner. We first introduce some basic concepts and definitions

in Section 1, such as dynamical systems, invariant sets, and limit sets. In

Section 2 we present and prove some useful lemmas on the properties of

invariant sets and limit sets. Finally, we establish the original LaSalle

invariance principle for discrete-time dynamical systems and a simple extension

in Section~3. In Section 4, we provide some references on extensions of LaSalle

invariance principles for further reading. This document is intended for

educational and tutorial purposes and contains lemmas that might be useful as a

reference for researchers.

-

We study some optimal control problems on networks with junctions,

approximate the junctions by a switching rule of delay-relay type and study the

passage to the limit when $\varepsilon$, the parameter of the approximation,

goes to zero. First, for a twofold junction problem we characterize the limit

value function as viscosity solution and maximal subsolution of a suitable

Hamilton-Jacobi problem. Then, for a threefold junction problem we consider two

different approximations, recovering in both cases some uniqueness results in

the sense of maximal subsolution.

-

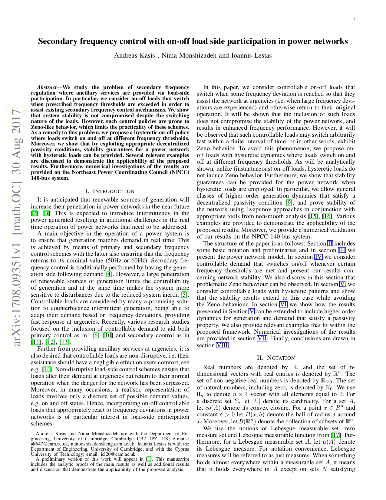

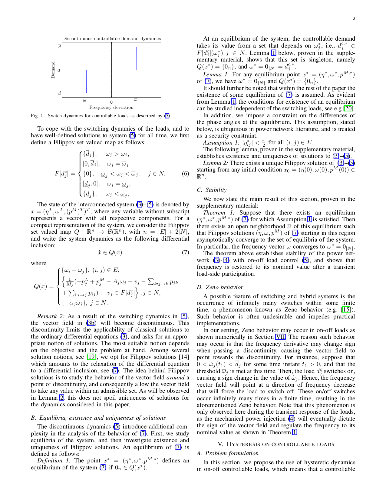

We study the problem of decentralized secondary frequency regulation in power

networks where ancillary services are provided via on-off load-side

participation. We initially consider on-off loads that switch when prescribed

frequency thresholds are exceeded, together with a large class of passive

continuous dynamics for generation and demand. The considered on-off loads are

able to assist existing secondary frequency control mechanisms and return to

their nominal operation when the power system is restored to its normal

operation, a highly desirable feature which minimizes users disruption. We show

that system stability is not compromised despite the switching nature of the

loads. However, such control policies are prone to chattering, which limits the

practicality of these schemes. As a remedy to this problem, we propose a

hysteretic on-off policy where loads switch on and off at different frequency

thresholds and show that stability guarantees are retained when the same

decentralized passivity conditions for continuous generation and demand hold.

Several relevant examples are discussed to demonstrate the applicability of the

proposed results. Furthermore, we verify our analytic results with numerical

investigations on the Northeast Power Coordinating Council (NPCC) 140-bus

system.

-

In this article, inspired by Shi, et al. we investigate the optimal portfolio

selection with one risk-free asset and one risky asset in a multiple period

setting under cumulative prospect theory (CPT). Compared with their study, our

novelty is that we consider a stochastic benchmark, and portfolio constraints.

We test the sensitivity of the optimal CPT-investment strategies to different

model parameters by performing a numerical analysis.

-

Distributed machine learning algorithms enable learning of models from

datasets that are distributed over a network without gathering the data at a

centralized location. While efficient distributed algorithms have been

developed under the assumption of faultless networks, failures that can render

these algorithms nonfunctional occur frequently in the real world. This paper

focuses on the problem of Byzantine failures, which are the hardest to

safeguard against in distributed algorithms. While Byzantine fault tolerance

has a rich history, existing work does not translate into efficient and

practical algorithms for high-dimensional learning in fully distributed (also

known as decentralized) settings. In this paper, an algorithm termed

Byzantine-resilient distributed coordinate descent (ByRDiE) is developed and

analyzed that enables distributed learning in the presence of Byzantine

failures. Theoretical analysis (convex settings) and numerical experiments

(convex and nonconvex settings) highlight its usefulness for high-dimensional

distributed learning in the presence of Byzantine failures.

-

This paper introduces a theoretical framework for the analysis and control of

the stochastic susceptible-infected-removed (SIR) spreading process over a

network of heterogeneous agents. In our analysis, we analyze the exact

networked Markov process describing the SIR model, without resorting to

mean-field approximations, and introduce a convex optimization framework to

find an efficient allocation of resources to contain the expected number of

accumulated infections over time. Numerical simulations are presented to

illustrate the effectiveness of the obtained results.

-

Information communicated within cyber-physical systems (CPSs) is often used

in determining the physical states of such systems, and malicious adversaries

may intercept these communications in order to infer future states of a CPS or

its components. Accordingly, there arises a need to protect the state values of

a system. Recently, the notion of differential privacy has been used to protect

state trajectories in dynamical systems, and it is this notion of privacy that

we use here to protect the state trajectories of CPSs. We incorporate a cloud

computer to coordinate the agents comprising the CPSs of interest, and the

cloud offers the ability to remotely coordinate many agents, rapidly perform

computations, and broadcast the results, making it a natural fit for systems

with many interacting agents or components. Striving for broad applicability,

we solve infinite-horizon linear-quadratic-regulator (LQR) problems, and each

agent protects its own state trajectory by adding noise to its states before

they are sent to the cloud. The cloud then uses these state values to generate

optimal inputs for the agents. As a result, private data is fed into feedback

loops at each iteration, and each noisy term affects every future state of

every agent. In this paper, we show that the differentially private LQR problem

can be related to the well-studied linear-quadratic-Gaussian (LQG) problem, and

we provide bounds on how agents' privacy requirements affect the cloud's

ability to generate optimal feedback control values for the agents. These

results are illustrated in numerical simulations.

-

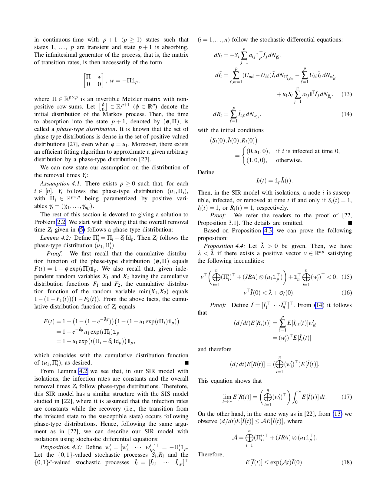

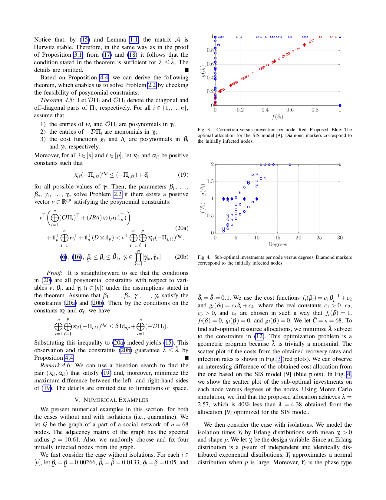

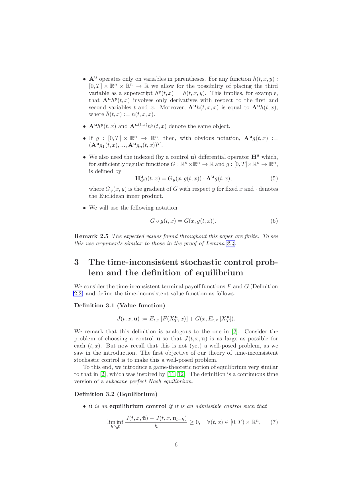

Control problems not admitting the dynamic programming principle are known as

time-inconsistent. The game-theoretic approach is to interpret such problems as

intrapersonal dynamic games and look for subgame perfect Nash equilibria. A

fundamental result of time-inconsistent stochastic control is a verification

theorem saying that solving the extended HJB system is a sufficient condition

for equilibrium. We show that solving the extended HJB system is a necessary

condition for equilibrium, under regularity assumptions. The controlled process

is a general It\^o diffusion.

-

We analyze the learning properties of the stochastic gradient method when

multiple passes over the data and mini-batches are allowed. We study how

regularization properties are controlled by the step-size, the number of passes

and the mini-batch size. In particular, we consider the square loss and show

that for a universal step-size choice, the number of passes acts as a

regularization parameter, and optimal finite sample bounds can be achieved by

early-stopping. Moreover, we show that larger step-sizes are allowed when

considering mini-batches. Our analysis is based on a unifying approach,

encompassing both batch and stochastic gradient methods as special cases. As a

byproduct, we derive optimal convergence results for batch gradient methods

(even in the non-attainable cases).

-

We study fundamental performance limitations of distributed feedback control

in large-scale networked dynamical systems. Specifically, we address the

question of whether dynamic feedback controllers perform better than static

(memoryless) ones when subject to locality constraints. We consider distributed

linear consensus and vehicular formation control problems modeled over toric

lattice networks. For the resulting spatially invariant systems we study the

large-scale asymptotics (in network size) of global performance metrics that

quantify the level of network coherence. With static feedback from relative

state measurements, such metrics are known to scale unfavorably in lattices of

low spatial dimensions, preventing, for example, a 1-dimensional string of

vehicles to move like a rigid object. We show that the same limitations in

general apply also to dynamic feedback control that is locally of first order.

This means that the addition of one local state to the controller gives a

similar asymptotic performance to the memoryless case. This holds unless the

controller can access noiseless measurements of its local state with respect to

an absolute reference frame, in which case the addition of controller memory

may fundamentally improve performance. In simulations of platoons with 20-200

vehicles we show that the performance limitations we derive manifest as

unwanted accordion-like motions. Similar behaviors are to be expected in any

network that is embeddable in a low-dimensional toric lattice, and the same

fundamental limitations would apply. To derive our results, we present a

general technical framework for the analysis of stability and performance of

spatially invariant systems in the limit of large networks.

-

We explore the lifting question in the context of cut-generating functions.

Most of the prior literature on this question focuses on cut-generating

functions that have the unique lifting property. We develop a general theory

for understanding the lifting question for cut-generating functions that do not

necessarily have the unique lifting property.

-

This document presents a (mostly) chronologically ordered bibliography of

scientific publications on the superiorization methodology and perturbation

resilience of algorithms which is compiled and continuously updated by us at:

http://math.haifa.ac.il/yair/bib-superiorization-censor.html. Since the

beginnings of this topic we try to trace the work that has been published about

it since its inception. To the best of our knowledge this bibliography

represents all available publications on this topic to date, and while the URL

is continuously updated we will revise this document and bring it up to date on

arXiv approximately once a year. Abstracts of the cited works, and some links

and downloadable files of preprints or reprints are available on the above

mentioned Internet page. If you know of a related scientific work in any form

that should be included here kindly write to me on: yair@math.haifa.ac.il with

full bibliographic details, a DOI if available, and a PDF copy of the work if

possible. The Internet page was initiated on March 7, 2015, and has been last

updated on March 2, 2021.

Comment: Some of the items have on the above mentioned Internet page more

information and links than in this report.

Acknowledgment: This work was supported by the ISF-NSFC joint research

program grant No. 2874/19.

-

Let $A$ be an $(m \times n)$ integral matrix, and let $P=\{ x : A x \leq b\}$

be an $n$-dimensional polytope. The width of $P$ is defined as $ w(P)=min\{

x\in \mathbb{Z}^n\setminus\{0\} :\: max_{x \in P} x^\top u - min_{x \in P}

x^\top v \}$. Let $\Delta(A)$ and $\delta(A)$ denote the greatest and the

smallest absolute values of a determinant among all $r(A) \times r(A)$

sub-matrices of $A$, where $r(A)$ is the rank of a matrix $A$. We prove that if

every $r(A) \times r(A)$ sub-matrix of $A$ has a determinant equal to $\pm

\Delta(A)$ or $0$ and $w(P)\ge (\Delta(A)-1)(n+1)$, then $P$ contains $n$

affine independent integer points. Also we have similar results for the case of

\emph{$k$-modular} matrices. The matrix $A$ is called \emph{totally

$k$-modular} if every square sub-matrix of $A$ has a determinant in the set

$\{0,\, \pm k^r :\: r \in \mathbb{N} \}$. When $P$ is a simplex and $w(P)\ge

\delta(A)-1$, we describe a polynomial time algorithm for finding an integer

point in $P$. Finally we show that if $A$ is \emph{almost unimodular}, then

integer program $\max \{c^\top x :\: x \in P \cap \mathbb{Z}^n \}$ can be

solved in polynomial time. The matrix $A$ is called \emph{almost unimodular} if

$\Delta(A) \leq 2$ and any $(r(A)-1)\times(r(A)-1)$ sub-matrix has a

determinant from the set $\{0,\pm 1\}$.

-

This paper investigates the behavior of the Min-Sum message passing scheme to

solve systems of linear equations in the Laplacian matrices of graphs and to

compute electric flows. Voltage and flow problems involve the minimization of

quadratic functions and are fundamental primitives that arise in several

domains. Algorithms that have been proposed are typically centralized and

involve multiple graph-theoretic constructions or sampling mechanisms that make

them difficult to implement and analyze. On the other hand, message passing

routines are distributed, simple, and easy to implement. In this paper we

establish a framework to analyze Min-Sum to solve voltage and flow problems. We

characterize the error committed by the algorithm on general weighted graphs in

terms of hitting times of random walks defined on the computation trees that

support the operations of the algorithms with time. For $d$-regular graphs with

equal weights, we show that the convergence of the algorithms is controlled by

the total variation distance between the distributions of non-backtracking

random walks defined on the original graph that start from neighboring nodes.

The framework that we introduce extends the analysis of Min-Sum to settings

where the contraction arguments previously considered in the literature (based

on the assumption of walk summability or scaled diagonal dominance) can not be

used, possibly in the presence of constraints.

-

Accounting for model uncertainty in risk management and option pricing leads

to infinite dimensional optimization problems which are both analytically and

numerically intractable. In this article we study when this hurdle can be

overcome for the so-called optimized certainty equivalent risk measure (OCE) --

including the average value-at-risk as a special case. First we focus on the

case where the uncertainty is modeled by a nonlinear expectation penalizing

distributions that are "far" in terms of optimal-transport distance

(Wasserstein distance for instance) from a given baseline distribution. It

turns out that the computation of the robust OCE reduces to a finite

dimensional problem, which in some cases can even be solved explicitly. This

principle also applies to the shortfall risk measure as well as for the pricing

of European options. Further, we derive convex dual representations of the

robust OCE for measurable claims without any assumptions on the set of

distributions. Finally, we give conditions on the latter set under which the

robust average value-at-risk is a tail risk measure.

-

Large networks of queueing systems model important real-world systems such as

MapReduce clusters, web-servers, hospitals, call centers and airport passenger

terminals. To model such systems accurately, we must infer queueing parameters

from data. Unfortunately, for many queueing networks there is no clear way to

proceed with parameter inference from data. Approximate Bayesian computation

could offer a straightforward way to infer parameters for such networks if we

could simulate data quickly enough.

We present a computationally efficient method for simulating from a very

general set of queueing networks with the R package queuecomputer. Remarkable

speedups of more than 2 orders of magnitude are observed relative to the

popular DES packages simmer and simpy. We replicate output from these packages

to validate the package.

The package is modular and integrates well with the popular R package dplyr.

Complex queueing networks with tandem, parallel and fork/join topologies can

easily be built with these two packages together. We show how to use this

package with two examples: a call center and an airport terminal.

-

This paper investigates the synthesis of distributed economic control

algorithms under which dynamically coupled physical systems are regulated to a

variational equilibrium of a constrained convex game. We study two

complementary cases: (i) each subsystem is linear and controllable; and (ii)

each subsystem is nonlinear and in the strict-feedback form. The convergence of

the proposed algorithms is guaranteed using Lyapunov analysis. Their

performance is verified by two case studies on a multi-zone building

temperature regulation problem and an optimal power flow problem, respectively.

-

This paper develops an analytic framework to design both stress-controlled

and displacement-controlled T-periodic loadings which make the quasistatic

evolution of a one-dimensional network of elastoplastic springs converging to a

unique periodic regime. The solution of such an evolution problem is a function

t-> (e(t),p(t)), where e_i(t) and p_i(t) are the elastic and plastic

deformations of spring i, defined on [t0,\infty) by the initial condition

(e(t0),p(t0)).

After we rigorously convert the problem into a Moreau sweeping process with a

moving polyhedron C(t) in a vector space E of dimension d, it becomes natural

to expect (based on a result by Krejci) that the solution t->(e(t),p(t)) always

converges to a T-periodic function. The achievement of this paper is in

spotting a class of loadings where the Krejci's limit doesn't depend on the

initial condition (e(t0),p(t0)) and so all the trajectories approach the same

T-periodic regime. The proposed class of sweeping processes is the one for

which the normal vectors of any d different facets of the moving polyhedron

C(t) are linearly independent. We further link this geometric condition to

mechanical properties of the given network of springs. We discover that the

normal vectors of any d different facets of the moving polyhedron C(t) are

linearly independent, if the number of displacement-controlled loadings is two

less the number of nodes of the given network of springs and when the magnitude

of the stress-controlled loading is sufficiently large (but admissible). The

result can be viewed as an analogue of the high-gain control method for

elastoplastic systems. In continuum theory of plasticity, the respective result

is known as Frederick-Armstrong theorem.

-

The classic Alternating Direction Method of Multipliers (ADMM) is a popular

framework to solve linear-equality constrained problems. In this paper, we

extend the ADMM naturally to nonlinear equality-constrained problems, called

neADMM. The difficulty of neADMM is to solve nonconvex subproblems. We provide

globally optimal solutions to them in two important applications. Experiments

on synthetic and real-world datasets demonstrate excellent performance and

scalability of our proposed neADMM over existing state-of-the-start methods.

-

In stochastic simulation, input uncertainty (IU) is caused by the error in

estimating the input distributions using finite real-world data. When it comes

to simulation-based Ranking and Selection (R&S), ignoring IU could lead to the

failure of many existing selection procedures. In this paper, we study R&S

under IU by allowing the possibility of acquiring additional data. Two

classical R&S formulations are extended to account for IU: (i) for fixed

confidence, we consider when data arrive sequentially so that IU can be reduced

over time; (ii) for fixed budget, a joint budget is assumed to be available for

both collecting input data and running simulations. New procedures are proposed

for each formulation using the frameworks of Sequential Elimination and Optimal

Computing Budget Allocation, with theoretical guarantees provided accordingly

(e.g., upper bound on the expected running time and finite-sample bound on the

probability of false selection). Numerical results demonstrate the

effectiveness of our procedures through a multi-stage production-inventory

problem.

-

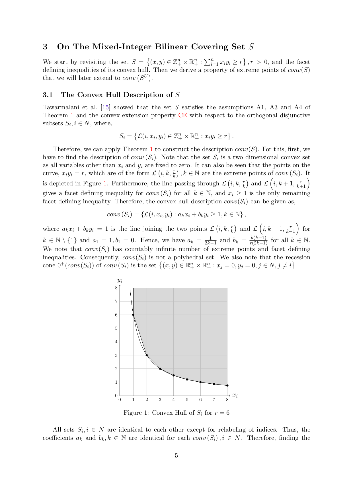

We derive a closed form description of the convex hull of mixed-integer

bilinear covering set with bounds on the integer variables. This convex hull

description is determined by considering some orthogonal disjunctive sets

defined in a certain way. This description does not introduce any new

variables, but consists of exponentially many inequalities. An extended

formulation with a few extra variables and much smaller number of constraints

is presented. We also derive a linear time separation algorithm for finding the

facet defining inequalities of this convex hull. We study the effectiveness of

the new inequalities and the extended formulation using some examples.

-

Motivated by applications arising from large scale optimization and machine

learning, we consider stochastic quasi-Newton (SQN) methods for solving

unconstrained convex optimization problems. The convergence analysis of the SQN

methods, both full and limited-memory variants, require the objective function

to be strongly convex. However, this assumption is fairly restrictive and does

not hold for applications such as minimizing the logistic regression loss

function. To the best of our knowledge, no rate statements currently exist for

SQN methods in the absence of such an assumption. Also, among the existing

first-order methods for addressing stochastic optimization problems with merely

convex objectives, those equipped with provable convergence rates employ

averaging. However, this averaging technique has a detrimental impact on

inducing sparsity. Motivated by these gaps, the main contributions of the paper

are as follows: (i) Addressing large scale stochastic optimization problems, we

develop an iteratively regularized stochastic limited-memory BFGS (IRS-LBFGS)

algorithm, where the stepsize, regularization parameter, and the Hessian

inverse approximation matrix are updated iteratively. We establish the

convergence to an optimal solution of the original problem both in an

almost-sure and mean senses. We derive the convergence rate in terms of the

objective function's values and show that it is of the order

$\mathcal{O}\left(k^{-\left(\frac{1}{3}-\epsilon\right)}\right)$, where

$\epsilon$ is an arbitrary small positive scalar; (ii) In deterministic regime,

we show that the regularized limited-memory BFGS algorithm displays a rate of

the order $\mathcal{O}\left(\frac{1}{k^{1 -\epsilon'}}\right)$, where

$\epsilon'$ is an arbitrary small positive scalar. We present our numerical

experiments performed on a large scale text classification problem.

-

We propose a new method for simplifying semidefinite programs (SDP) inspired

by symmetry reduction. Specifically, we show if an orthogonal projection map

satisfies certain invariance conditions, restricting to its range yields an

equivalent primal-dual pair over a lower-dimensional symmetric cone---namely,

the cone-of-squares of a Jordan subalgebra of symmetric matrices. We present a

simple algorithm for minimizing the rank of this projection and hence the

dimension of this subalgebra. We also show that minimizing rank optimizes the

direct-sum decomposition of the algebra into simple ideals, yielding an optimal

"block-diagonalization" of the SDP. Finally, we give combinatorial versions of

our algorithm that execute at reduced computational cost and illustrate

effectiveness of an implementation on examples. Through the theory of Jordan

algebras, the proposed method easily extends to linear and second-order-cone

programming and, more generally, symmetric cone optimization.

-

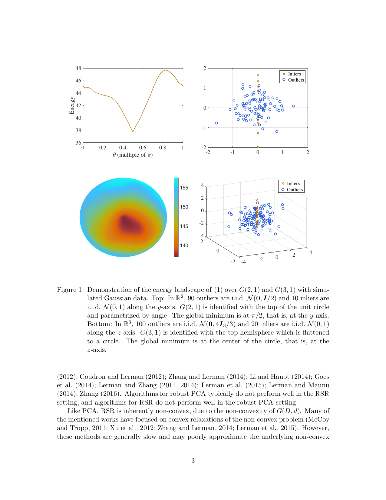

We present a mathematical analysis of a non-convex energy landscape for

robust subspace recovery. We prove that an underlying subspace is the only

stationary point and local minimizer in a specified neighborhood under a

deterministic condition on a dataset. If the deterministic condition is

satisfied, we further show that a geodesic gradient descent method over the

Grassmannian manifold can exactly recover the underlying subspace when the

method is properly initialized. Proper initialization by principal component

analysis is guaranteed with a simple deterministic condition. Under slightly

stronger assumptions, the gradient descent method with a piecewise constant

step-size scheme achieves linear convergence. The practicality of the

deterministic condition is demonstrated on some statistical models of data, and

the method achieves almost state-of-the-art recovery guarantees on the Haystack

Model for different regimes of sample size and ambient dimension. In

particular, when the ambient dimension is fixed and the sample size is large

enough, we show that our gradient method can exactly recover the underlying

subspace for any fixed fraction of outliers (less than 1).

We study the problem of decentralized secondary frequency regulation in power networks where ancillary services are provided via on-off load-side participation. We initially consider on-off loads that switch when prescribed frequency thresholds are exceeded, together with a large class of passive continuous dynamics for generation and demand. The considered on-off loads are able to assist existing secondary frequency control mechanisms and return to their nominal operation when the power system is restored to its normal operation, a highly desirable feature which minimizes users disruption. We show that system stability is not compromised despite the switching nature of the loads. However, such control policies are prone to chattering, which limits the practicality of these schemes. As a remedy to this problem, we propose a hysteretic on-off policy where loads switch on and off at different frequency thresholds and show that stability guarantees are retained when the same decentralized passivity conditions for continuous generation and demand hold. Several relevant examples are discussed to demonstrate the applicability of the proposed results. Furthermore, we verify our analytic results with numerical investigations on the Northeast Power Coordinating Council (NPCC) 140-bus system.

We study the problem of decentralized secondary frequency regulation in power networks where ancillary services are provided via on-off load-side participation. We initially consider on-off loads that switch when prescribed frequency thresholds are exceeded, together with a large class of passive continuous dynamics for generation and demand. The considered on-off loads are able to assist existing secondary frequency control mechanisms and return to their nominal operation when the power system is restored to its normal operation, a highly desirable feature which minimizes users disruption. We show that system stability is not compromised despite the switching nature of the loads. However, such control policies are prone to chattering, which limits the practicality of these schemes. As a remedy to this problem, we propose a hysteretic on-off policy where loads switch on and off at different frequency thresholds and show that stability guarantees are retained when the same decentralized passivity conditions for continuous generation and demand hold. Several relevant examples are discussed to demonstrate the applicability of the proposed results. Furthermore, we verify our analytic results with numerical investigations on the Northeast Power Coordinating Council (NPCC) 140-bus system.

In this article, inspired by Shi, et al. we investigate the optimal portfolio selection with one risk-free asset and one risky asset in a multiple period setting under cumulative prospect theory (CPT). Compared with their study, our novelty is that we consider a stochastic benchmark, and portfolio constraints. We test the sensitivity of the optimal CPT-investment strategies to different model parameters by performing a numerical analysis.

In this article, inspired by Shi, et al. we investigate the optimal portfolio selection with one risk-free asset and one risky asset in a multiple period setting under cumulative prospect theory (CPT). Compared with their study, our novelty is that we consider a stochastic benchmark, and portfolio constraints. We test the sensitivity of the optimal CPT-investment strategies to different model parameters by performing a numerical analysis.

Distributed machine learning algorithms enable learning of models from datasets that are distributed over a network without gathering the data at a centralized location. While efficient distributed algorithms have been developed under the assumption of faultless networks, failures that can render these algorithms nonfunctional occur frequently in the real world. This paper focuses on the problem of Byzantine failures, which are the hardest to safeguard against in distributed algorithms. While Byzantine fault tolerance has a rich history, existing work does not translate into efficient and practical algorithms for high-dimensional learning in fully distributed (also known as decentralized) settings. In this paper, an algorithm termed Byzantine-resilient distributed coordinate descent (ByRDiE) is developed and analyzed that enables distributed learning in the presence of Byzantine failures. Theoretical analysis (convex settings) and numerical experiments (convex and nonconvex settings) highlight its usefulness for high-dimensional distributed learning in the presence of Byzantine failures.

Distributed machine learning algorithms enable learning of models from datasets that are distributed over a network without gathering the data at a centralized location. While efficient distributed algorithms have been developed under the assumption of faultless networks, failures that can render these algorithms nonfunctional occur frequently in the real world. This paper focuses on the problem of Byzantine failures, which are the hardest to safeguard against in distributed algorithms. While Byzantine fault tolerance has a rich history, existing work does not translate into efficient and practical algorithms for high-dimensional learning in fully distributed (also known as decentralized) settings. In this paper, an algorithm termed Byzantine-resilient distributed coordinate descent (ByRDiE) is developed and analyzed that enables distributed learning in the presence of Byzantine failures. Theoretical analysis (convex settings) and numerical experiments (convex and nonconvex settings) highlight its usefulness for high-dimensional distributed learning in the presence of Byzantine failures.

This paper introduces a theoretical framework for the analysis and control of the stochastic susceptible-infected-removed (SIR) spreading process over a network of heterogeneous agents. In our analysis, we analyze the exact networked Markov process describing the SIR model, without resorting to mean-field approximations, and introduce a convex optimization framework to find an efficient allocation of resources to contain the expected number of accumulated infections over time. Numerical simulations are presented to illustrate the effectiveness of the obtained results.

This paper introduces a theoretical framework for the analysis and control of the stochastic susceptible-infected-removed (SIR) spreading process over a network of heterogeneous agents. In our analysis, we analyze the exact networked Markov process describing the SIR model, without resorting to mean-field approximations, and introduce a convex optimization framework to find an efficient allocation of resources to contain the expected number of accumulated infections over time. Numerical simulations are presented to illustrate the effectiveness of the obtained results.

Control problems not admitting the dynamic programming principle are known as time-inconsistent. The game-theoretic approach is to interpret such problems as intrapersonal dynamic games and look for subgame perfect Nash equilibria. A fundamental result of time-inconsistent stochastic control is a verification theorem saying that solving the extended HJB system is a sufficient condition for equilibrium. We show that solving the extended HJB system is a necessary condition for equilibrium, under regularity assumptions. The controlled process is a general It\^o diffusion.

Control problems not admitting the dynamic programming principle are known as time-inconsistent. The game-theoretic approach is to interpret such problems as intrapersonal dynamic games and look for subgame perfect Nash equilibria. A fundamental result of time-inconsistent stochastic control is a verification theorem saying that solving the extended HJB system is a sufficient condition for equilibrium. We show that solving the extended HJB system is a necessary condition for equilibrium, under regularity assumptions. The controlled process is a general It\^o diffusion.

We analyze the learning properties of the stochastic gradient method when multiple passes over the data and mini-batches are allowed. We study how regularization properties are controlled by the step-size, the number of passes and the mini-batch size. In particular, we consider the square loss and show that for a universal step-size choice, the number of passes acts as a regularization parameter, and optimal finite sample bounds can be achieved by early-stopping. Moreover, we show that larger step-sizes are allowed when considering mini-batches. Our analysis is based on a unifying approach, encompassing both batch and stochastic gradient methods as special cases. As a byproduct, we derive optimal convergence results for batch gradient methods (even in the non-attainable cases).

We analyze the learning properties of the stochastic gradient method when multiple passes over the data and mini-batches are allowed. We study how regularization properties are controlled by the step-size, the number of passes and the mini-batch size. In particular, we consider the square loss and show that for a universal step-size choice, the number of passes acts as a regularization parameter, and optimal finite sample bounds can be achieved by early-stopping. Moreover, we show that larger step-sizes are allowed when considering mini-batches. Our analysis is based on a unifying approach, encompassing both batch and stochastic gradient methods as special cases. As a byproduct, we derive optimal convergence results for batch gradient methods (even in the non-attainable cases).

We explore the lifting question in the context of cut-generating functions. Most of the prior literature on this question focuses on cut-generating functions that have the unique lifting property. We develop a general theory for understanding the lifting question for cut-generating functions that do not necessarily have the unique lifting property.

We explore the lifting question in the context of cut-generating functions. Most of the prior literature on this question focuses on cut-generating functions that have the unique lifting property. We develop a general theory for understanding the lifting question for cut-generating functions that do not necessarily have the unique lifting property.

This document presents a (mostly) chronologically ordered bibliography of scientific publications on the superiorization methodology and perturbation resilience of algorithms which is compiled and continuously updated by us at: http://math.haifa.ac.il/yair/bib-superiorization-censor.html. Since the beginnings of this topic we try to trace the work that has been published about it since its inception. To the best of our knowledge this bibliography represents all available publications on this topic to date, and while the URL is continuously updated we will revise this document and bring it up to date on arXiv approximately once a year. Abstracts of the cited works, and some links and downloadable files of preprints or reprints are available on the above mentioned Internet page. If you know of a related scientific work in any form that should be included here kindly write to me on: yair@math.haifa.ac.il with full bibliographic details, a DOI if available, and a PDF copy of the work if possible. The Internet page was initiated on March 7, 2015, and has been last updated on March 2, 2021. Comment: Some of the items have on the above mentioned Internet page more information and links than in this report. Acknowledgment: This work was supported by the ISF-NSFC joint research program grant No. 2874/19.

This document presents a (mostly) chronologically ordered bibliography of scientific publications on the superiorization methodology and perturbation resilience of algorithms which is compiled and continuously updated by us at: http://math.haifa.ac.il/yair/bib-superiorization-censor.html. Since the beginnings of this topic we try to trace the work that has been published about it since its inception. To the best of our knowledge this bibliography represents all available publications on this topic to date, and while the URL is continuously updated we will revise this document and bring it up to date on arXiv approximately once a year. Abstracts of the cited works, and some links and downloadable files of preprints or reprints are available on the above mentioned Internet page. If you know of a related scientific work in any form that should be included here kindly write to me on: yair@math.haifa.ac.il with full bibliographic details, a DOI if available, and a PDF copy of the work if possible. The Internet page was initiated on March 7, 2015, and has been last updated on March 2, 2021. Comment: Some of the items have on the above mentioned Internet page more information and links than in this report. Acknowledgment: This work was supported by the ISF-NSFC joint research program grant No. 2874/19.

Let $A$ be an $(m \times n)$ integral matrix, and let $P=\{ x : A x \leq b\}$ be an $n$-dimensional polytope. The width of $P$ is defined as $ w(P)=min\{ x\in \mathbb{Z}^n\setminus\{0\} :\: max_{x \in P} x^\top u - min_{x \in P} x^\top v \}$. Let $\Delta(A)$ and $\delta(A)$ denote the greatest and the smallest absolute values of a determinant among all $r(A) \times r(A)$ sub-matrices of $A$, where $r(A)$ is the rank of a matrix $A$. We prove that if every $r(A) \times r(A)$ sub-matrix of $A$ has a determinant equal to $\pm \Delta(A)$ or $0$ and $w(P)\ge (\Delta(A)-1)(n+1)$, then $P$ contains $n$ affine independent integer points. Also we have similar results for the case of \emph{$k$-modular} matrices. The matrix $A$ is called \emph{totally $k$-modular} if every square sub-matrix of $A$ has a determinant in the set $\{0,\, \pm k^r :\: r \in \mathbb{N} \}$. When $P$ is a simplex and $w(P)\ge \delta(A)-1$, we describe a polynomial time algorithm for finding an integer point in $P$. Finally we show that if $A$ is \emph{almost unimodular}, then integer program $\max \{c^\top x :\: x \in P \cap \mathbb{Z}^n \}$ can be solved in polynomial time. The matrix $A$ is called \emph{almost unimodular} if $\Delta(A) \leq 2$ and any $(r(A)-1)\times(r(A)-1)$ sub-matrix has a determinant from the set $\{0,\pm 1\}$.

Let $A$ be an $(m \times n)$ integral matrix, and let $P=\{ x : A x \leq b\}$ be an $n$-dimensional polytope. The width of $P$ is defined as $ w(P)=min\{ x\in \mathbb{Z}^n\setminus\{0\} :\: max_{x \in P} x^\top u - min_{x \in P} x^\top v \}$. Let $\Delta(A)$ and $\delta(A)$ denote the greatest and the smallest absolute values of a determinant among all $r(A) \times r(A)$ sub-matrices of $A$, where $r(A)$ is the rank of a matrix $A$. We prove that if every $r(A) \times r(A)$ sub-matrix of $A$ has a determinant equal to $\pm \Delta(A)$ or $0$ and $w(P)\ge (\Delta(A)-1)(n+1)$, then $P$ contains $n$ affine independent integer points. Also we have similar results for the case of \emph{$k$-modular} matrices. The matrix $A$ is called \emph{totally $k$-modular} if every square sub-matrix of $A$ has a determinant in the set $\{0,\, \pm k^r :\: r \in \mathbb{N} \}$. When $P$ is a simplex and $w(P)\ge \delta(A)-1$, we describe a polynomial time algorithm for finding an integer point in $P$. Finally we show that if $A$ is \emph{almost unimodular}, then integer program $\max \{c^\top x :\: x \in P \cap \mathbb{Z}^n \}$ can be solved in polynomial time. The matrix $A$ is called \emph{almost unimodular} if $\Delta(A) \leq 2$ and any $(r(A)-1)\times(r(A)-1)$ sub-matrix has a determinant from the set $\{0,\pm 1\}$.

This paper investigates the behavior of the Min-Sum message passing scheme to solve systems of linear equations in the Laplacian matrices of graphs and to compute electric flows. Voltage and flow problems involve the minimization of quadratic functions and are fundamental primitives that arise in several domains. Algorithms that have been proposed are typically centralized and involve multiple graph-theoretic constructions or sampling mechanisms that make them difficult to implement and analyze. On the other hand, message passing routines are distributed, simple, and easy to implement. In this paper we establish a framework to analyze Min-Sum to solve voltage and flow problems. We characterize the error committed by the algorithm on general weighted graphs in terms of hitting times of random walks defined on the computation trees that support the operations of the algorithms with time. For $d$-regular graphs with equal weights, we show that the convergence of the algorithms is controlled by the total variation distance between the distributions of non-backtracking random walks defined on the original graph that start from neighboring nodes. The framework that we introduce extends the analysis of Min-Sum to settings where the contraction arguments previously considered in the literature (based on the assumption of walk summability or scaled diagonal dominance) can not be used, possibly in the presence of constraints.

This paper investigates the behavior of the Min-Sum message passing scheme to solve systems of linear equations in the Laplacian matrices of graphs and to compute electric flows. Voltage and flow problems involve the minimization of quadratic functions and are fundamental primitives that arise in several domains. Algorithms that have been proposed are typically centralized and involve multiple graph-theoretic constructions or sampling mechanisms that make them difficult to implement and analyze. On the other hand, message passing routines are distributed, simple, and easy to implement. In this paper we establish a framework to analyze Min-Sum to solve voltage and flow problems. We characterize the error committed by the algorithm on general weighted graphs in terms of hitting times of random walks defined on the computation trees that support the operations of the algorithms with time. For $d$-regular graphs with equal weights, we show that the convergence of the algorithms is controlled by the total variation distance between the distributions of non-backtracking random walks defined on the original graph that start from neighboring nodes. The framework that we introduce extends the analysis of Min-Sum to settings where the contraction arguments previously considered in the literature (based on the assumption of walk summability or scaled diagonal dominance) can not be used, possibly in the presence of constraints.

Accounting for model uncertainty in risk management and option pricing leads to infinite dimensional optimization problems which are both analytically and numerically intractable. In this article we study when this hurdle can be overcome for the so-called optimized certainty equivalent risk measure (OCE) -- including the average value-at-risk as a special case. First we focus on the case where the uncertainty is modeled by a nonlinear expectation penalizing distributions that are "far" in terms of optimal-transport distance (Wasserstein distance for instance) from a given baseline distribution. It turns out that the computation of the robust OCE reduces to a finite dimensional problem, which in some cases can even be solved explicitly. This principle also applies to the shortfall risk measure as well as for the pricing of European options. Further, we derive convex dual representations of the robust OCE for measurable claims without any assumptions on the set of distributions. Finally, we give conditions on the latter set under which the robust average value-at-risk is a tail risk measure.

Accounting for model uncertainty in risk management and option pricing leads to infinite dimensional optimization problems which are both analytically and numerically intractable. In this article we study when this hurdle can be overcome for the so-called optimized certainty equivalent risk measure (OCE) -- including the average value-at-risk as a special case. First we focus on the case where the uncertainty is modeled by a nonlinear expectation penalizing distributions that are "far" in terms of optimal-transport distance (Wasserstein distance for instance) from a given baseline distribution. It turns out that the computation of the robust OCE reduces to a finite dimensional problem, which in some cases can even be solved explicitly. This principle also applies to the shortfall risk measure as well as for the pricing of European options. Further, we derive convex dual representations of the robust OCE for measurable claims without any assumptions on the set of distributions. Finally, we give conditions on the latter set under which the robust average value-at-risk is a tail risk measure.

Large networks of queueing systems model important real-world systems such as MapReduce clusters, web-servers, hospitals, call centers and airport passenger terminals. To model such systems accurately, we must infer queueing parameters from data. Unfortunately, for many queueing networks there is no clear way to proceed with parameter inference from data. Approximate Bayesian computation could offer a straightforward way to infer parameters for such networks if we could simulate data quickly enough. We present a computationally efficient method for simulating from a very general set of queueing networks with the R package queuecomputer. Remarkable speedups of more than 2 orders of magnitude are observed relative to the popular DES packages simmer and simpy. We replicate output from these packages to validate the package. The package is modular and integrates well with the popular R package dplyr. Complex queueing networks with tandem, parallel and fork/join topologies can easily be built with these two packages together. We show how to use this package with two examples: a call center and an airport terminal.

Large networks of queueing systems model important real-world systems such as MapReduce clusters, web-servers, hospitals, call centers and airport passenger terminals. To model such systems accurately, we must infer queueing parameters from data. Unfortunately, for many queueing networks there is no clear way to proceed with parameter inference from data. Approximate Bayesian computation could offer a straightforward way to infer parameters for such networks if we could simulate data quickly enough. We present a computationally efficient method for simulating from a very general set of queueing networks with the R package queuecomputer. Remarkable speedups of more than 2 orders of magnitude are observed relative to the popular DES packages simmer and simpy. We replicate output from these packages to validate the package. The package is modular and integrates well with the popular R package dplyr. Complex queueing networks with tandem, parallel and fork/join topologies can easily be built with these two packages together. We show how to use this package with two examples: a call center and an airport terminal.

This paper develops an analytic framework to design both stress-controlled and displacement-controlled T-periodic loadings which make the quasistatic evolution of a one-dimensional network of elastoplastic springs converging to a unique periodic regime. The solution of such an evolution problem is a function t-> (e(t),p(t)), where e_i(t) and p_i(t) are the elastic and plastic deformations of spring i, defined on [t0,\infty) by the initial condition (e(t0),p(t0)). After we rigorously convert the problem into a Moreau sweeping process with a moving polyhedron C(t) in a vector space E of dimension d, it becomes natural to expect (based on a result by Krejci) that the solution t->(e(t),p(t)) always converges to a T-periodic function. The achievement of this paper is in spotting a class of loadings where the Krejci's limit doesn't depend on the initial condition (e(t0),p(t0)) and so all the trajectories approach the same T-periodic regime. The proposed class of sweeping processes is the one for which the normal vectors of any d different facets of the moving polyhedron C(t) are linearly independent. We further link this geometric condition to mechanical properties of the given network of springs. We discover that the normal vectors of any d different facets of the moving polyhedron C(t) are linearly independent, if the number of displacement-controlled loadings is two less the number of nodes of the given network of springs and when the magnitude of the stress-controlled loading is sufficiently large (but admissible). The result can be viewed as an analogue of the high-gain control method for elastoplastic systems. In continuum theory of plasticity, the respective result is known as Frederick-Armstrong theorem.

This paper develops an analytic framework to design both stress-controlled and displacement-controlled T-periodic loadings which make the quasistatic evolution of a one-dimensional network of elastoplastic springs converging to a unique periodic regime. The solution of such an evolution problem is a function t-> (e(t),p(t)), where e_i(t) and p_i(t) are the elastic and plastic deformations of spring i, defined on [t0,\infty) by the initial condition (e(t0),p(t0)). After we rigorously convert the problem into a Moreau sweeping process with a moving polyhedron C(t) in a vector space E of dimension d, it becomes natural to expect (based on a result by Krejci) that the solution t->(e(t),p(t)) always converges to a T-periodic function. The achievement of this paper is in spotting a class of loadings where the Krejci's limit doesn't depend on the initial condition (e(t0),p(t0)) and so all the trajectories approach the same T-periodic regime. The proposed class of sweeping processes is the one for which the normal vectors of any d different facets of the moving polyhedron C(t) are linearly independent. We further link this geometric condition to mechanical properties of the given network of springs. We discover that the normal vectors of any d different facets of the moving polyhedron C(t) are linearly independent, if the number of displacement-controlled loadings is two less the number of nodes of the given network of springs and when the magnitude of the stress-controlled loading is sufficiently large (but admissible). The result can be viewed as an analogue of the high-gain control method for elastoplastic systems. In continuum theory of plasticity, the respective result is known as Frederick-Armstrong theorem.

The classic Alternating Direction Method of Multipliers (ADMM) is a popular framework to solve linear-equality constrained problems. In this paper, we extend the ADMM naturally to nonlinear equality-constrained problems, called neADMM. The difficulty of neADMM is to solve nonconvex subproblems. We provide globally optimal solutions to them in two important applications. Experiments on synthetic and real-world datasets demonstrate excellent performance and scalability of our proposed neADMM over existing state-of-the-start methods.

The classic Alternating Direction Method of Multipliers (ADMM) is a popular framework to solve linear-equality constrained problems. In this paper, we extend the ADMM naturally to nonlinear equality-constrained problems, called neADMM. The difficulty of neADMM is to solve nonconvex subproblems. We provide globally optimal solutions to them in two important applications. Experiments on synthetic and real-world datasets demonstrate excellent performance and scalability of our proposed neADMM over existing state-of-the-start methods.

In stochastic simulation, input uncertainty (IU) is caused by the error in estimating the input distributions using finite real-world data. When it comes to simulation-based Ranking and Selection (R&S), ignoring IU could lead to the failure of many existing selection procedures. In this paper, we study R&S under IU by allowing the possibility of acquiring additional data. Two classical R&S formulations are extended to account for IU: (i) for fixed confidence, we consider when data arrive sequentially so that IU can be reduced over time; (ii) for fixed budget, a joint budget is assumed to be available for both collecting input data and running simulations. New procedures are proposed for each formulation using the frameworks of Sequential Elimination and Optimal Computing Budget Allocation, with theoretical guarantees provided accordingly (e.g., upper bound on the expected running time and finite-sample bound on the probability of false selection). Numerical results demonstrate the effectiveness of our procedures through a multi-stage production-inventory problem.

In stochastic simulation, input uncertainty (IU) is caused by the error in estimating the input distributions using finite real-world data. When it comes to simulation-based Ranking and Selection (R&S), ignoring IU could lead to the failure of many existing selection procedures. In this paper, we study R&S under IU by allowing the possibility of acquiring additional data. Two classical R&S formulations are extended to account for IU: (i) for fixed confidence, we consider when data arrive sequentially so that IU can be reduced over time; (ii) for fixed budget, a joint budget is assumed to be available for both collecting input data and running simulations. New procedures are proposed for each formulation using the frameworks of Sequential Elimination and Optimal Computing Budget Allocation, with theoretical guarantees provided accordingly (e.g., upper bound on the expected running time and finite-sample bound on the probability of false selection). Numerical results demonstrate the effectiveness of our procedures through a multi-stage production-inventory problem.

We derive a closed form description of the convex hull of mixed-integer bilinear covering set with bounds on the integer variables. This convex hull description is determined by considering some orthogonal disjunctive sets defined in a certain way. This description does not introduce any new variables, but consists of exponentially many inequalities. An extended formulation with a few extra variables and much smaller number of constraints is presented. We also derive a linear time separation algorithm for finding the facet defining inequalities of this convex hull. We study the effectiveness of the new inequalities and the extended formulation using some examples.

We derive a closed form description of the convex hull of mixed-integer bilinear covering set with bounds on the integer variables. This convex hull description is determined by considering some orthogonal disjunctive sets defined in a certain way. This description does not introduce any new variables, but consists of exponentially many inequalities. An extended formulation with a few extra variables and much smaller number of constraints is presented. We also derive a linear time separation algorithm for finding the facet defining inequalities of this convex hull. We study the effectiveness of the new inequalities and the extended formulation using some examples.

We propose a new method for simplifying semidefinite programs (SDP) inspired by symmetry reduction. Specifically, we show if an orthogonal projection map satisfies certain invariance conditions, restricting to its range yields an equivalent primal-dual pair over a lower-dimensional symmetric cone---namely, the cone-of-squares of a Jordan subalgebra of symmetric matrices. We present a simple algorithm for minimizing the rank of this projection and hence the dimension of this subalgebra. We also show that minimizing rank optimizes the direct-sum decomposition of the algebra into simple ideals, yielding an optimal "block-diagonalization" of the SDP. Finally, we give combinatorial versions of our algorithm that execute at reduced computational cost and illustrate effectiveness of an implementation on examples. Through the theory of Jordan algebras, the proposed method easily extends to linear and second-order-cone programming and, more generally, symmetric cone optimization.

We propose a new method for simplifying semidefinite programs (SDP) inspired by symmetry reduction. Specifically, we show if an orthogonal projection map satisfies certain invariance conditions, restricting to its range yields an equivalent primal-dual pair over a lower-dimensional symmetric cone---namely, the cone-of-squares of a Jordan subalgebra of symmetric matrices. We present a simple algorithm for minimizing the rank of this projection and hence the dimension of this subalgebra. We also show that minimizing rank optimizes the direct-sum decomposition of the algebra into simple ideals, yielding an optimal "block-diagonalization" of the SDP. Finally, we give combinatorial versions of our algorithm that execute at reduced computational cost and illustrate effectiveness of an implementation on examples. Through the theory of Jordan algebras, the proposed method easily extends to linear and second-order-cone programming and, more generally, symmetric cone optimization.

We present a mathematical analysis of a non-convex energy landscape for robust subspace recovery. We prove that an underlying subspace is the only stationary point and local minimizer in a specified neighborhood under a deterministic condition on a dataset. If the deterministic condition is satisfied, we further show that a geodesic gradient descent method over the Grassmannian manifold can exactly recover the underlying subspace when the method is properly initialized. Proper initialization by principal component analysis is guaranteed with a simple deterministic condition. Under slightly stronger assumptions, the gradient descent method with a piecewise constant step-size scheme achieves linear convergence. The practicality of the deterministic condition is demonstrated on some statistical models of data, and the method achieves almost state-of-the-art recovery guarantees on the Haystack Model for different regimes of sample size and ambient dimension. In particular, when the ambient dimension is fixed and the sample size is large enough, we show that our gradient method can exactly recover the underlying subspace for any fixed fraction of outliers (less than 1).

We present a mathematical analysis of a non-convex energy landscape for robust subspace recovery. We prove that an underlying subspace is the only stationary point and local minimizer in a specified neighborhood under a deterministic condition on a dataset. If the deterministic condition is satisfied, we further show that a geodesic gradient descent method over the Grassmannian manifold can exactly recover the underlying subspace when the method is properly initialized. Proper initialization by principal component analysis is guaranteed with a simple deterministic condition. Under slightly stronger assumptions, the gradient descent method with a piecewise constant step-size scheme achieves linear convergence. The practicality of the deterministic condition is demonstrated on some statistical models of data, and the method achieves almost state-of-the-art recovery guarantees on the Haystack Model for different regimes of sample size and ambient dimension. In particular, when the ambient dimension is fixed and the sample size is large enough, we show that our gradient method can exactly recover the underlying subspace for any fixed fraction of outliers (less than 1).