-

We demonstrate that the use of asymptotic expansion as prior knowledge in the

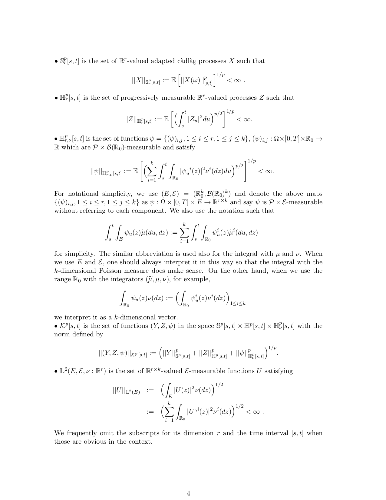

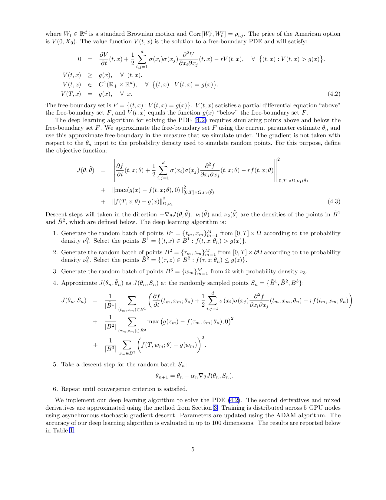

"deep BSDE solver", which is a deep learning method for high dimensional BSDEs

proposed by Weinan E, Han & Jentzen (2017), drastically reduces the loss

function and accelerates the speed of convergence. We illustrate the technique

and its implications by using Bergman's model with different lending and

borrowing rates as a typical model for FVA as well as a class of solvable BSDEs

with quadratic growth drivers. We also present an extension of the deep BSDE

solver for reflected BSDEs representing American option prices.

-

In this paper, for $\mu$ and $\nu$ two probability measures on $\mathbb{R}^d$

with finite moments of order $\rho\ge 1$, we define the respective projections

for the $W_\rho$-Wasserstein distance of $\mu$ and $\nu$ on the sets of

probability measures dominated by $\nu$ and of probability measures larger than

$\mu$ in the convex order. The $W_2$-projection of $\mu$ can be easily computed

when $\mu$ and $\nu$ have finite support by solving a quadratic optimization

problem with linear constraints. In dimension $d=1$, Gozlan et al.~(2018) have

shown that the projections do not depend on $\rho$. We explicit their quantile

functions in terms of those of $\mu$ and $\nu$. The motivation is the design of

sampling techniques preserving the convex order in order to approximate

Martingale Optimal Transport problems by using linear programming solvers. We

prove convergence of the Wasserstein projection based sampling methods as the

sample sizes tend to infinity and illustrate them by numerical experiments.

-

We derive a new high-order compact finite difference scheme for option

pricing in stochastic volatility jump models, e.g. in Bates model. In such

models the option price is determined as the solution of a partial

integro-differential equation. The scheme is fourth order accurate in space and

second order accurate in time. Numerical experiments for the European option

pricing problem are presented. We validate the stability of the scheme

numerically and compare its performance to standard finite difference and

finite element methods. The new scheme outperforms a standard discretisation

based on a second-order central finite difference approximation in all our

experiments. At the same time, it is very efficient, requiring only one initial

$LU$-factorisation of a sparse matrix to perform the option price valuation.

Compared to finite element approaches, it is very parsimonious in terms of

memory requirements and computational effort, since it achieves high-order

convergence without requiring additional unknowns, unlike finite element

methods with higher polynomial order basis functions. The new high-order

compact scheme can also be useful to upgrade existing implementations based on

standard finite differences in a straightforward manner to obtain a highly

efficient option pricing code.

-

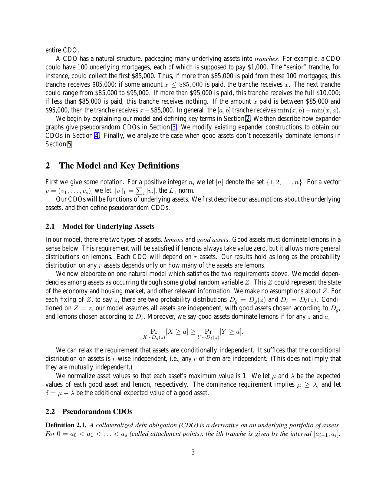

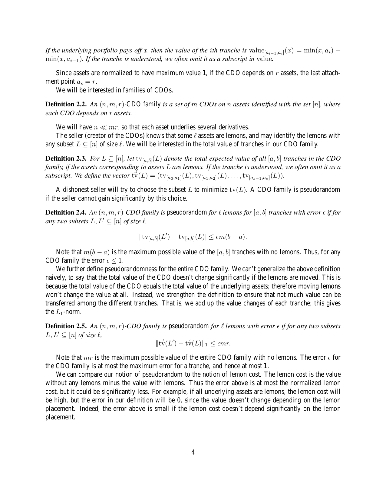

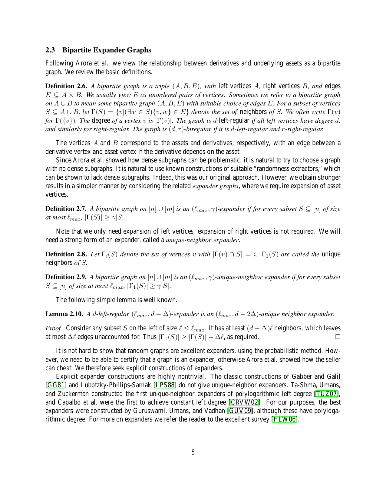

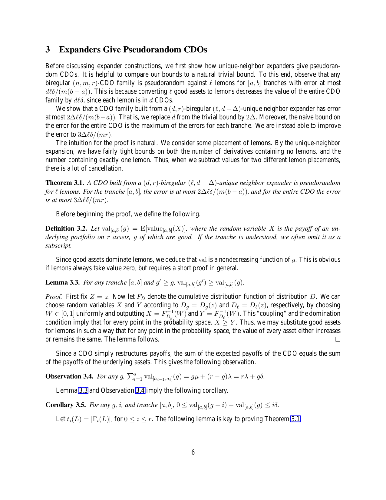

Arora, Barak, Brunnermeier, and Ge showed that taking computational

complexity into account, a dishonest seller could strategically place lemons in

financial derivatives to make them substantially less valuable to buyers. We

show that if the seller is required to construct derivatives of a certain form,

then this phenomenon disappears. In particular, we define and construct

pseudorandom derivative families, for which lemon placement only slightly

affects the values of the derivatives. Our constructions use expander graphs.

We study our derivatives in a more general setting than Arora et al. In

particular, we analyze arbitrary tranches of the common collateralized debt

obligations (CDOs) when the underlying assets can have significant

dependencies.

-

Determining risk contributions of unit exposures to portfolio-wide economic

capital is an important task in financial risk management. Computing risk

contributions involves difficulties caused by rare-event simulations. In this

study, we address the problem of estimating risk contributions when the total

risk is measured by value-at-risk (VaR). Our proposed estimator of VaR

contributions is based on the Metropolis-Hasting (MH) algorithm, which is one

of the most prevalent Markov chain Monte Carlo (MCMC) methods. Unlike existing

estimators, our MH-based estimator consists of samples from conditional loss

distribution given a rare event of interest. This feature enhances sample

efficiency compared with the crude Monte Carlo method. Moreover, our method has

the consistency and asymptotic normality, and is widely applicable to various

risk models having joint loss density. Our numerical experiments based on

simulation and real-world data demonstrate that in various risk models, even

those having high-dimensional (approximately 500) inhomogeneous margins, our MH

estimator has smaller bias and mean squared error compared with existing

estimators.

-

Instantaneous volatility of logarithmic return in the lognormal fractional

SABR model is driven by the exponentiation of a correlated fractional Brownian

motion. Due to the mixed nature of driving Brownian and fractional Brownian

motions, probability density for such a model is less studied in the

literature. We show in this paper a bridge representation for the joint density

of the lognormal fractional SABR model in a Fourier space. Evaluating the

bridge representation along a properly chosen deterministic path yields a small

time asymptotic expansion to the leading order for the probability density of

the fractional SABR model. A direct generalization of the representation to

joint density at multiple times leads to a heuristic derivation of the large

deviations principle for the joint density in small time. Approximation of

implied volatility is readily obtained by applying the Laplace asymptotic

formula to the call or put prices and comparing coefficients.

-

We discuss in this note applications of the Multidimensional Positive

Definite Advection Transport Algorithm (MPDATA) to numerical solutions of

partial differential equations arising from stochastic models in quantitative

finance. In particular, we develop a framework for solving Black-Scholes-type

equations by first transforming them into advection-diffusion problems, and

numerically integrating using an iterative explicit finite-difference approach,

in which the Fickian term is represented as an additional advective term. We

discuss the correspondence between transport phenomena and financial models,

uncovering the possibility of expressing the no-arbitrage principle as a

conservation law. We depict second-order accuracy in time and space of the

embraced numerical scheme. This is done in a convergence analysis comparing

MPDATA numerical solutions with classic Black-Scholes analytical formulae for

the valuation of European options. We demonstrate in addition a way of applying

MPDATA to solve the free boundary problem (leading to a linear complementarity

problem) for the valuation of American options. We finally comment on the

potential the MPDATA framework has with respect to being applied in tandem with

more complex models typically used in quantitive finance.

-

In a very high-dimensional vector space, two randomly-chosen vectors are

almost orthogonal with high probability. Starting from this observation, we

develop a statistical factor model, the random factor model, in which factors

are chosen at random based on the random projection method. Randomness of

factors has the consequence that covariance matrix is well preserved in a

linear factor representation. It also enables derivation of probabilistic

bounds for the accuracy of the random factor representation of time-series,

their cross-correlations and covariances. As an application, we analyze

reproduction of time-series and their cross-correlation coefficients in the

well-diversified Russell 3,000 equity index.

-

Stochastic gradient descent in continuous time (SGDCT) provides a

computationally efficient method for the statistical learning of

continuous-time models, which are widely used in science, engineering, and

finance. The SGDCT algorithm follows a (noisy) descent direction along a

continuous stream of data. The parameter updates occur in continuous time and

satisfy a stochastic differential equation. This paper analyzes the asymptotic

convergence rate of the SGDCT algorithm by proving a central limit theorem

(CLT) for strongly convex objective functions and, under slightly stronger

conditions, for non-convex objective functions as well. An $L^{p}$ convergence

rate is also proven for the algorithm in the strongly convex case. The

mathematical analysis lies at the intersection of stochastic analysis and

statistical learning.

-

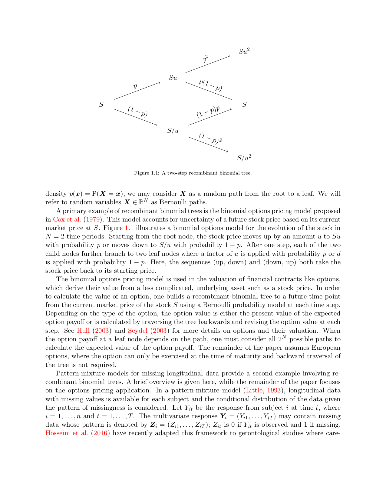

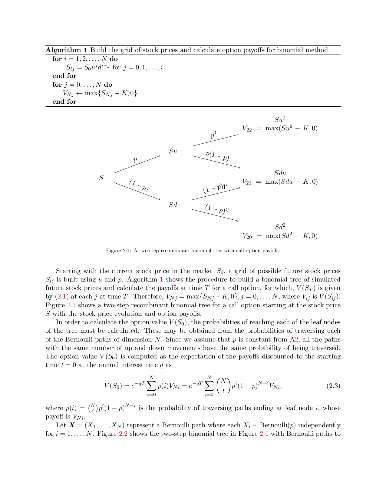

Recombinant binomial trees are binary trees where each non-leaf node has two

child nodes, but adjacent parents share a common child node. Such trees arise

in finance when pricing an option. For example, valuation of a European option

can be carried out by evaluating the expected value of asset payoffs with

respect to random paths in the tree. In many variants of the option valuation

problem, a closed form solution cannot be obtained and computational methods

are needed. The cost to exactly compute expected values over random paths grows

exponentially in the depth of the tree, rendering a serial computation of one

branch at a time impractical. We propose a parallelization method that

transforms the calculation of the expected value into an "embarrassingly

parallel" problem by mapping the branches of the binomial tree to the processes

in a multiprocessor computing environment. We also propose a parallel Monte

Carlo method which takes advantage of the mapping to achieve a reduced variance

over the basic Monte Carlo estimator. Performance results from R and Julia

implementations of the parallelization method on a distributed computing

cluster indicate that both the implementations are scalable, but Julia is

significantly faster than a similarly written R code. A simulation study is

carried out to verify the convergence and the variance reduction behavior in

the proposed Monte Carlo method.

-

We consider a class of stochastic path-dependent volatility models where the

stochastic volatility, whose square follows the Cox-Ingersoll-Ross model, is

multiplied by a (leverage) function of the spot price, its running maximum, and

time. We propose a Monte Carlo simulation scheme which combines a log-Euler

scheme for the spot process with the full truncation Euler scheme or the

backward Euler-Maruyama scheme for the squared stochastic volatility component.

Under some mild regularity assumptions and a condition on the Feller ratio, we

establish the strong convergence with order 1/2 (up to a logarithmic factor) of

the approximation process up to a critical time. The model studied in this

paper contains as special cases Heston-type stochastic-local volatility models,

the state-of-the-art in derivative pricing, and a relatively new class of

path-dependent volatility models. The present paper is the first to prove the

convergence of the popular Euler schemes with a positive rate, which is

moreover consistent with that for Lipschitz coefficients and hence optimal.

-

We study convergence properties of the full truncation Euler scheme for the

Cox-Ingersoll-Ross process in the regime where the boundary point zero is

inaccessible. Under some conditions on the model parameters (precisely, when

the Feller ratio is greater than three), we establish the strong order 1/2

convergence in $L^{p}$ of the scheme to the exact solution. This is consistent

with the optimal rate of strong convergence for Euler approximations of

stochastic differential equations with globally Lipschitz coefficients, despite

the fact that the diffusion coefficient in the Cox-Ingersoll-Ross model is not

Lipschitz.

-

We consider a Black-Scholes type equation arising on a pricing model for a

multi-asset option with general transaction costs. The pioneering work of

Leland is thus extended in two different ways: on the one hand, the problem is

multi-dimensional since it involves different underlying assets; on the other

hand, the transaction costs are not assumed to be constant (i.e. a fixed

proportion of the traded quantity). In this work, we generalize Leland's

condition and prove the existence of a viscosity solution for the corresponding

fully nonlinear initial value problem using Perron method. Moreover, we develop

a numerical ADI scheme to find an approximated solution. We apply this method

on a specific multi-asset derivative and we obtain the option price under

different pricing scenarios.

-

In this paper, we propose a novel investment strategy for portfolio

optimization problems. The proposed strategy maximizes the expected portfolio

value bounded within a targeted range, composed of a conservative lower target

representing a need for capital protection and a desired upper target

representing an investment goal. This strategy favorably shapes the entire

probability distribution of returns, as it simultaneously seeks a desired

expected return, cuts off downside risk and implicitly caps volatility and

higher moments. To illustrate the effectiveness of this investment strategy, we

study a multiperiod portfolio optimization problem with transaction costs and

develop a two-stage regression approach that improves the classical least

squares Monte Carlo (LSMC) algorithm when dealing with difficult payoffs, such

as highly concave, abruptly changing or discontinuous functions. Our numerical

results show substantial improvements over the classical LSMC algorithm for

both the constant relative risk-aversion (CRRA) utility approach and the

proposed skewed target range strategy (STRS). Our numerical results illustrate

the ability of the STRS to contain the portfolio value within the targeted

range. When compared with the CRRA utility approach, the STRS achieves a

similar mean-variance efficient frontier while delivering a better downside

risk-return trade-off.

-

This work provides a semi-analytic approximation method for decoupled

forwardbackward SDEs (FBSDEs) with jumps. In particular, we construct an

asymptotic expansion method for FBSDEs driven by the random Poisson measures

with {\sigma}-finite compensators as well as the standard Brownian motions

around the small-variance limit of the forward SDE. We provide a semi-analytic

solution technique as well as its error estimate for which we only need to

solve essentially a system of linear ODEs. In the case of a finite jump measure

with a bounded intensity, the method can also handle state-dependent and hence

non-Poissonian jumps, which are quite relevant for many practical applications.

-

A non-Euclidean generalization of conditional expectation is introduced and

characterized as the minimizer of expected intrinsic squared-distance from a

manifold-valued target. The computational tractable formulation expresses the

non-convex optimization problem as transformations of Euclidean conditional

expectation. This gives computationally tractable filtering equations for the

dynamics of the intrinsic conditional expectation of a manifold-valued signal

and is used to obtain accurate numerical forecasts of efficient portfolios by

incorporating their geometric structure into the estimates.

-

High-dimensional PDEs have been a longstanding computational challenge. We

propose to solve high-dimensional PDEs by approximating the solution with a

deep neural network which is trained to satisfy the differential operator,

initial condition, and boundary conditions. Our algorithm is meshfree, which is

key since meshes become infeasible in higher dimensions. Instead of forming a

mesh, the neural network is trained on batches of randomly sampled time and

space points. The algorithm is tested on a class of high-dimensional free

boundary PDEs, which we are able to accurately solve in up to $200$ dimensions.

The algorithm is also tested on a high-dimensional Hamilton-Jacobi-Bellman PDE

and Burgers' equation. The deep learning algorithm approximates the general

solution to the Burgers' equation for a continuum of different boundary

conditions and physical conditions (which can be viewed as a high-dimensional

space). We call the algorithm a "Deep Galerkin Method (DGM)" since it is

similar in spirit to Galerkin methods, with the solution approximated by a

neural network instead of a linear combination of basis functions. In addition,

we prove a theorem regarding the approximation power of neural networks for a

class of quasilinear parabolic PDEs.

-

This paper proposes and analyses a new multilevel Monte Carlo method for the

estimation of mean exit times for multi-dimensional Brownian diffusions, and

associated functionals which correspond to solutions to high-dimensional

parabolic PDEs through the Feynman-Kac formula. In particular, it is proved

that the complexity to achieve an $\varepsilon$ root-mean-square error is

$O(\varepsilon^{-2}\, |\!\log \varepsilon|^3)$.

-

The multilevel Monte Carlo path simulation method introduced by Giles ({\it

Operations Research}, 56(3):607-617, 2008) exploits strong convergence

properties to improve the computational complexity by combining simulations

with different levels of resolution. In this paper we analyse its efficiency

when using the Milstein discretisation; this has an improved order of strong

convergence compared to the standard Euler-Maruyama method, and it is proved

that this leads to an improved order of convergence of the variance of the

multilevel estimator. Numerical results are also given for basket options to

illustrate the relevance of the analysis.

-

Conditions of Stability for explicit finite difference scheme and some

results of numerical analysis for a unified 2 factor model of structural and

reduced form types for corporate bonds with fixed discrete coupon are provided.

It seems to be difficult to get solution formula for PDE model which

generalizes Agliardi's structural model [1] for discrete coupon bonds into a

unified 2 factor model of structural and reduced form types and we study a

numerical analysis for it by explicit finite difference scheme. These equations

are parabolic equations with 3 variables and they include mixed derivatives, so

the explicit finite difference scheme is not stable in general. We find

conditions for the explicit finite difference scheme to be stable, in the case

that it is stable, numerically compute the price of the bond and analyze its

credit spread and duration.

-

We present a new and easy-to-implement sequential sampling method for CGMY

processes with either finite or infinite variation, exploiting the time change

representation of the CGMY model and a decomposition of its time change. We

find that the time change can be decomposed into two independent components.

While the first component is a \emph{finite} \emph{generalized gamma

convolution} process whose increments can be sampled by either the exact double

CFTP ("coupling from the past") method or an approximation scheme with high

speed and accuracy, the second component can easily be made arbitrarily small

in the $L^1$ sense. Simulation results show that the proposed method is

advantageous over two existing methods under a model calibrated to historical

option price data.

-

We propose a new backtesting framework for Expected Shortfall that could be

used by the regulator. Instead of looking at the estimated capital reserve and

the realised cash-flow separately, one could bind them into the secured

position, for which risk measurement is much easier. Using this simple concept

combined with monotonicity of Expected Shortfall with respect to its target

confidence level we introduce a natural and efficient backtesting framework.

Our test statistics is given by the biggest number of worst realisations for

the secured position that add up to a negative total. Surprisingly, this simple

quantity could be used to construct an efficient backtesting framework for

unconditional coverage of Expected Shortfall in a natural extension of the

regulatory traffic-light approach for Value-at-Risk. While being easy to

calculate, the test statistic is based on the underlying duality between

coherent risk measures and scale-invariant performance measures.

-

This article addresses the problem of approximating the price of options on

discrete and continuous arithmetic average of the underlying, i.e. discretely

and continuously monitored Asian options, in local volatility models. A

path-integral-type expression for option prices is obtained using a Brownian

bridge representation for the transition density between consecutive sampling

times and a Laplace asymptotic formula. In the limit where the sampling time

window approaches zero, the option price is found to be approximated by a

constrained variational problem on paths in time-price space. We refer to the

optimizing path as the most-likely path (MLP). Approximation for the implied

normal volatility follows accordingly. The small-time asymptotics and the

existence of the MLP are also recovered rigorously using large deviation

theory.

-

We consider the optimal stopping problem with non-linear $f$-expectation

(induced by a BSDE) without making any regularity assumptions on the reward

process $\xi$. and with general filtration. We show that the value family can

be aggregated by an optional process $Y$. We characterize the process $Y$ as

the $\mathcal{E}^f$-Snell envelope of $\xi$. We also establish an infinitesimal

characterization of the value process $Y$ in terms of a Reflected BSDE with

$\xi$ as the obstacle. To do this, we first establish a comparison theorem for

irregular RBSDEs. We give an application to the pricing of American options

with irregular pay-off in an imperfect market model.

-

Dupire's functional It\^o calculus provides an alternative approach to the

classical Malliavin calculus for the computation of sensitivities, also called

Greeks, of path-dependent derivatives prices. In this paper, we introduce a

measure of path-dependence of functionals within the functional It\^o calculus

framework. Namely, we consider the Lie bracket of the space and time functional

derivatives, which we use to classify functionals accordingly to their degree

of path-dependence. We then revisit the problem of efficient numerical

computation of Greeks for path-dependent derivatives using integration by parts

techniques. Special attention is paid to path-dependent functionals with zero

Lie bracket, called locally weakly path-dependent functionals in our

classification. Hence, we derive the weighted-expectation formulas for their

Greeks. In the more general case of fully path-dependent functionals, we show

that, equipped with the functional It\^o calculus, we are able to analyze the

effect of the Lie bracket on the computation of Greeks. Moreover, we are also

able to consider the more general dynamics of path-dependent volatility. These

were not achieved using Malliavin calculus.

We derive a new high-order compact finite difference scheme for option pricing in stochastic volatility jump models, e.g. in Bates model. In such models the option price is determined as the solution of a partial integro-differential equation. The scheme is fourth order accurate in space and second order accurate in time. Numerical experiments for the European option pricing problem are presented. We validate the stability of the scheme numerically and compare its performance to standard finite difference and finite element methods. The new scheme outperforms a standard discretisation based on a second-order central finite difference approximation in all our experiments. At the same time, it is very efficient, requiring only one initial $LU$-factorisation of a sparse matrix to perform the option price valuation. Compared to finite element approaches, it is very parsimonious in terms of memory requirements and computational effort, since it achieves high-order convergence without requiring additional unknowns, unlike finite element methods with higher polynomial order basis functions. The new high-order compact scheme can also be useful to upgrade existing implementations based on standard finite differences in a straightforward manner to obtain a highly efficient option pricing code.

We derive a new high-order compact finite difference scheme for option pricing in stochastic volatility jump models, e.g. in Bates model. In such models the option price is determined as the solution of a partial integro-differential equation. The scheme is fourth order accurate in space and second order accurate in time. Numerical experiments for the European option pricing problem are presented. We validate the stability of the scheme numerically and compare its performance to standard finite difference and finite element methods. The new scheme outperforms a standard discretisation based on a second-order central finite difference approximation in all our experiments. At the same time, it is very efficient, requiring only one initial $LU$-factorisation of a sparse matrix to perform the option price valuation. Compared to finite element approaches, it is very parsimonious in terms of memory requirements and computational effort, since it achieves high-order convergence without requiring additional unknowns, unlike finite element methods with higher polynomial order basis functions. The new high-order compact scheme can also be useful to upgrade existing implementations based on standard finite differences in a straightforward manner to obtain a highly efficient option pricing code.

Arora, Barak, Brunnermeier, and Ge showed that taking computational complexity into account, a dishonest seller could strategically place lemons in financial derivatives to make them substantially less valuable to buyers. We show that if the seller is required to construct derivatives of a certain form, then this phenomenon disappears. In particular, we define and construct pseudorandom derivative families, for which lemon placement only slightly affects the values of the derivatives. Our constructions use expander graphs. We study our derivatives in a more general setting than Arora et al. In particular, we analyze arbitrary tranches of the common collateralized debt obligations (CDOs) when the underlying assets can have significant dependencies.

Arora, Barak, Brunnermeier, and Ge showed that taking computational complexity into account, a dishonest seller could strategically place lemons in financial derivatives to make them substantially less valuable to buyers. We show that if the seller is required to construct derivatives of a certain form, then this phenomenon disappears. In particular, we define and construct pseudorandom derivative families, for which lemon placement only slightly affects the values of the derivatives. Our constructions use expander graphs. We study our derivatives in a more general setting than Arora et al. In particular, we analyze arbitrary tranches of the common collateralized debt obligations (CDOs) when the underlying assets can have significant dependencies.

Determining risk contributions of unit exposures to portfolio-wide economic capital is an important task in financial risk management. Computing risk contributions involves difficulties caused by rare-event simulations. In this study, we address the problem of estimating risk contributions when the total risk is measured by value-at-risk (VaR). Our proposed estimator of VaR contributions is based on the Metropolis-Hasting (MH) algorithm, which is one of the most prevalent Markov chain Monte Carlo (MCMC) methods. Unlike existing estimators, our MH-based estimator consists of samples from conditional loss distribution given a rare event of interest. This feature enhances sample efficiency compared with the crude Monte Carlo method. Moreover, our method has the consistency and asymptotic normality, and is widely applicable to various risk models having joint loss density. Our numerical experiments based on simulation and real-world data demonstrate that in various risk models, even those having high-dimensional (approximately 500) inhomogeneous margins, our MH estimator has smaller bias and mean squared error compared with existing estimators.

Determining risk contributions of unit exposures to portfolio-wide economic capital is an important task in financial risk management. Computing risk contributions involves difficulties caused by rare-event simulations. In this study, we address the problem of estimating risk contributions when the total risk is measured by value-at-risk (VaR). Our proposed estimator of VaR contributions is based on the Metropolis-Hasting (MH) algorithm, which is one of the most prevalent Markov chain Monte Carlo (MCMC) methods. Unlike existing estimators, our MH-based estimator consists of samples from conditional loss distribution given a rare event of interest. This feature enhances sample efficiency compared with the crude Monte Carlo method. Moreover, our method has the consistency and asymptotic normality, and is widely applicable to various risk models having joint loss density. Our numerical experiments based on simulation and real-world data demonstrate that in various risk models, even those having high-dimensional (approximately 500) inhomogeneous margins, our MH estimator has smaller bias and mean squared error compared with existing estimators.

Instantaneous volatility of logarithmic return in the lognormal fractional SABR model is driven by the exponentiation of a correlated fractional Brownian motion. Due to the mixed nature of driving Brownian and fractional Brownian motions, probability density for such a model is less studied in the literature. We show in this paper a bridge representation for the joint density of the lognormal fractional SABR model in a Fourier space. Evaluating the bridge representation along a properly chosen deterministic path yields a small time asymptotic expansion to the leading order for the probability density of the fractional SABR model. A direct generalization of the representation to joint density at multiple times leads to a heuristic derivation of the large deviations principle for the joint density in small time. Approximation of implied volatility is readily obtained by applying the Laplace asymptotic formula to the call or put prices and comparing coefficients.

Instantaneous volatility of logarithmic return in the lognormal fractional SABR model is driven by the exponentiation of a correlated fractional Brownian motion. Due to the mixed nature of driving Brownian and fractional Brownian motions, probability density for such a model is less studied in the literature. We show in this paper a bridge representation for the joint density of the lognormal fractional SABR model in a Fourier space. Evaluating the bridge representation along a properly chosen deterministic path yields a small time asymptotic expansion to the leading order for the probability density of the fractional SABR model. A direct generalization of the representation to joint density at multiple times leads to a heuristic derivation of the large deviations principle for the joint density in small time. Approximation of implied volatility is readily obtained by applying the Laplace asymptotic formula to the call or put prices and comparing coefficients.

We discuss in this note applications of the Multidimensional Positive Definite Advection Transport Algorithm (MPDATA) to numerical solutions of partial differential equations arising from stochastic models in quantitative finance. In particular, we develop a framework for solving Black-Scholes-type equations by first transforming them into advection-diffusion problems, and numerically integrating using an iterative explicit finite-difference approach, in which the Fickian term is represented as an additional advective term. We discuss the correspondence between transport phenomena and financial models, uncovering the possibility of expressing the no-arbitrage principle as a conservation law. We depict second-order accuracy in time and space of the embraced numerical scheme. This is done in a convergence analysis comparing MPDATA numerical solutions with classic Black-Scholes analytical formulae for the valuation of European options. We demonstrate in addition a way of applying MPDATA to solve the free boundary problem (leading to a linear complementarity problem) for the valuation of American options. We finally comment on the potential the MPDATA framework has with respect to being applied in tandem with more complex models typically used in quantitive finance.

We discuss in this note applications of the Multidimensional Positive Definite Advection Transport Algorithm (MPDATA) to numerical solutions of partial differential equations arising from stochastic models in quantitative finance. In particular, we develop a framework for solving Black-Scholes-type equations by first transforming them into advection-diffusion problems, and numerically integrating using an iterative explicit finite-difference approach, in which the Fickian term is represented as an additional advective term. We discuss the correspondence between transport phenomena and financial models, uncovering the possibility of expressing the no-arbitrage principle as a conservation law. We depict second-order accuracy in time and space of the embraced numerical scheme. This is done in a convergence analysis comparing MPDATA numerical solutions with classic Black-Scholes analytical formulae for the valuation of European options. We demonstrate in addition a way of applying MPDATA to solve the free boundary problem (leading to a linear complementarity problem) for the valuation of American options. We finally comment on the potential the MPDATA framework has with respect to being applied in tandem with more complex models typically used in quantitive finance.

In a very high-dimensional vector space, two randomly-chosen vectors are almost orthogonal with high probability. Starting from this observation, we develop a statistical factor model, the random factor model, in which factors are chosen at random based on the random projection method. Randomness of factors has the consequence that covariance matrix is well preserved in a linear factor representation. It also enables derivation of probabilistic bounds for the accuracy of the random factor representation of time-series, their cross-correlations and covariances. As an application, we analyze reproduction of time-series and their cross-correlation coefficients in the well-diversified Russell 3,000 equity index.

In a very high-dimensional vector space, two randomly-chosen vectors are almost orthogonal with high probability. Starting from this observation, we develop a statistical factor model, the random factor model, in which factors are chosen at random based on the random projection method. Randomness of factors has the consequence that covariance matrix is well preserved in a linear factor representation. It also enables derivation of probabilistic bounds for the accuracy of the random factor representation of time-series, their cross-correlations and covariances. As an application, we analyze reproduction of time-series and their cross-correlation coefficients in the well-diversified Russell 3,000 equity index.

Recombinant binomial trees are binary trees where each non-leaf node has two child nodes, but adjacent parents share a common child node. Such trees arise in finance when pricing an option. For example, valuation of a European option can be carried out by evaluating the expected value of asset payoffs with respect to random paths in the tree. In many variants of the option valuation problem, a closed form solution cannot be obtained and computational methods are needed. The cost to exactly compute expected values over random paths grows exponentially in the depth of the tree, rendering a serial computation of one branch at a time impractical. We propose a parallelization method that transforms the calculation of the expected value into an "embarrassingly parallel" problem by mapping the branches of the binomial tree to the processes in a multiprocessor computing environment. We also propose a parallel Monte Carlo method which takes advantage of the mapping to achieve a reduced variance over the basic Monte Carlo estimator. Performance results from R and Julia implementations of the parallelization method on a distributed computing cluster indicate that both the implementations are scalable, but Julia is significantly faster than a similarly written R code. A simulation study is carried out to verify the convergence and the variance reduction behavior in the proposed Monte Carlo method.

Recombinant binomial trees are binary trees where each non-leaf node has two child nodes, but adjacent parents share a common child node. Such trees arise in finance when pricing an option. For example, valuation of a European option can be carried out by evaluating the expected value of asset payoffs with respect to random paths in the tree. In many variants of the option valuation problem, a closed form solution cannot be obtained and computational methods are needed. The cost to exactly compute expected values over random paths grows exponentially in the depth of the tree, rendering a serial computation of one branch at a time impractical. We propose a parallelization method that transforms the calculation of the expected value into an "embarrassingly parallel" problem by mapping the branches of the binomial tree to the processes in a multiprocessor computing environment. We also propose a parallel Monte Carlo method which takes advantage of the mapping to achieve a reduced variance over the basic Monte Carlo estimator. Performance results from R and Julia implementations of the parallelization method on a distributed computing cluster indicate that both the implementations are scalable, but Julia is significantly faster than a similarly written R code. A simulation study is carried out to verify the convergence and the variance reduction behavior in the proposed Monte Carlo method.

We consider a class of stochastic path-dependent volatility models where the stochastic volatility, whose square follows the Cox-Ingersoll-Ross model, is multiplied by a (leverage) function of the spot price, its running maximum, and time. We propose a Monte Carlo simulation scheme which combines a log-Euler scheme for the spot process with the full truncation Euler scheme or the backward Euler-Maruyama scheme for the squared stochastic volatility component. Under some mild regularity assumptions and a condition on the Feller ratio, we establish the strong convergence with order 1/2 (up to a logarithmic factor) of the approximation process up to a critical time. The model studied in this paper contains as special cases Heston-type stochastic-local volatility models, the state-of-the-art in derivative pricing, and a relatively new class of path-dependent volatility models. The present paper is the first to prove the convergence of the popular Euler schemes with a positive rate, which is moreover consistent with that for Lipschitz coefficients and hence optimal.

We consider a class of stochastic path-dependent volatility models where the stochastic volatility, whose square follows the Cox-Ingersoll-Ross model, is multiplied by a (leverage) function of the spot price, its running maximum, and time. We propose a Monte Carlo simulation scheme which combines a log-Euler scheme for the spot process with the full truncation Euler scheme or the backward Euler-Maruyama scheme for the squared stochastic volatility component. Under some mild regularity assumptions and a condition on the Feller ratio, we establish the strong convergence with order 1/2 (up to a logarithmic factor) of the approximation process up to a critical time. The model studied in this paper contains as special cases Heston-type stochastic-local volatility models, the state-of-the-art in derivative pricing, and a relatively new class of path-dependent volatility models. The present paper is the first to prove the convergence of the popular Euler schemes with a positive rate, which is moreover consistent with that for Lipschitz coefficients and hence optimal.

We study convergence properties of the full truncation Euler scheme for the Cox-Ingersoll-Ross process in the regime where the boundary point zero is inaccessible. Under some conditions on the model parameters (precisely, when the Feller ratio is greater than three), we establish the strong order 1/2 convergence in $L^{p}$ of the scheme to the exact solution. This is consistent with the optimal rate of strong convergence for Euler approximations of stochastic differential equations with globally Lipschitz coefficients, despite the fact that the diffusion coefficient in the Cox-Ingersoll-Ross model is not Lipschitz.

We study convergence properties of the full truncation Euler scheme for the Cox-Ingersoll-Ross process in the regime where the boundary point zero is inaccessible. Under some conditions on the model parameters (precisely, when the Feller ratio is greater than three), we establish the strong order 1/2 convergence in $L^{p}$ of the scheme to the exact solution. This is consistent with the optimal rate of strong convergence for Euler approximations of stochastic differential equations with globally Lipschitz coefficients, despite the fact that the diffusion coefficient in the Cox-Ingersoll-Ross model is not Lipschitz.

We consider a Black-Scholes type equation arising on a pricing model for a multi-asset option with general transaction costs. The pioneering work of Leland is thus extended in two different ways: on the one hand, the problem is multi-dimensional since it involves different underlying assets; on the other hand, the transaction costs are not assumed to be constant (i.e. a fixed proportion of the traded quantity). In this work, we generalize Leland's condition and prove the existence of a viscosity solution for the corresponding fully nonlinear initial value problem using Perron method. Moreover, we develop a numerical ADI scheme to find an approximated solution. We apply this method on a specific multi-asset derivative and we obtain the option price under different pricing scenarios.

We consider a Black-Scholes type equation arising on a pricing model for a multi-asset option with general transaction costs. The pioneering work of Leland is thus extended in two different ways: on the one hand, the problem is multi-dimensional since it involves different underlying assets; on the other hand, the transaction costs are not assumed to be constant (i.e. a fixed proportion of the traded quantity). In this work, we generalize Leland's condition and prove the existence of a viscosity solution for the corresponding fully nonlinear initial value problem using Perron method. Moreover, we develop a numerical ADI scheme to find an approximated solution. We apply this method on a specific multi-asset derivative and we obtain the option price under different pricing scenarios.

In this paper, we propose a novel investment strategy for portfolio optimization problems. The proposed strategy maximizes the expected portfolio value bounded within a targeted range, composed of a conservative lower target representing a need for capital protection and a desired upper target representing an investment goal. This strategy favorably shapes the entire probability distribution of returns, as it simultaneously seeks a desired expected return, cuts off downside risk and implicitly caps volatility and higher moments. To illustrate the effectiveness of this investment strategy, we study a multiperiod portfolio optimization problem with transaction costs and develop a two-stage regression approach that improves the classical least squares Monte Carlo (LSMC) algorithm when dealing with difficult payoffs, such as highly concave, abruptly changing or discontinuous functions. Our numerical results show substantial improvements over the classical LSMC algorithm for both the constant relative risk-aversion (CRRA) utility approach and the proposed skewed target range strategy (STRS). Our numerical results illustrate the ability of the STRS to contain the portfolio value within the targeted range. When compared with the CRRA utility approach, the STRS achieves a similar mean-variance efficient frontier while delivering a better downside risk-return trade-off.

In this paper, we propose a novel investment strategy for portfolio optimization problems. The proposed strategy maximizes the expected portfolio value bounded within a targeted range, composed of a conservative lower target representing a need for capital protection and a desired upper target representing an investment goal. This strategy favorably shapes the entire probability distribution of returns, as it simultaneously seeks a desired expected return, cuts off downside risk and implicitly caps volatility and higher moments. To illustrate the effectiveness of this investment strategy, we study a multiperiod portfolio optimization problem with transaction costs and develop a two-stage regression approach that improves the classical least squares Monte Carlo (LSMC) algorithm when dealing with difficult payoffs, such as highly concave, abruptly changing or discontinuous functions. Our numerical results show substantial improvements over the classical LSMC algorithm for both the constant relative risk-aversion (CRRA) utility approach and the proposed skewed target range strategy (STRS). Our numerical results illustrate the ability of the STRS to contain the portfolio value within the targeted range. When compared with the CRRA utility approach, the STRS achieves a similar mean-variance efficient frontier while delivering a better downside risk-return trade-off.

This work provides a semi-analytic approximation method for decoupled forwardbackward SDEs (FBSDEs) with jumps. In particular, we construct an asymptotic expansion method for FBSDEs driven by the random Poisson measures with {\sigma}-finite compensators as well as the standard Brownian motions around the small-variance limit of the forward SDE. We provide a semi-analytic solution technique as well as its error estimate for which we only need to solve essentially a system of linear ODEs. In the case of a finite jump measure with a bounded intensity, the method can also handle state-dependent and hence non-Poissonian jumps, which are quite relevant for many practical applications.

This work provides a semi-analytic approximation method for decoupled forwardbackward SDEs (FBSDEs) with jumps. In particular, we construct an asymptotic expansion method for FBSDEs driven by the random Poisson measures with {\sigma}-finite compensators as well as the standard Brownian motions around the small-variance limit of the forward SDE. We provide a semi-analytic solution technique as well as its error estimate for which we only need to solve essentially a system of linear ODEs. In the case of a finite jump measure with a bounded intensity, the method can also handle state-dependent and hence non-Poissonian jumps, which are quite relevant for many practical applications.

High-dimensional PDEs have been a longstanding computational challenge. We propose to solve high-dimensional PDEs by approximating the solution with a deep neural network which is trained to satisfy the differential operator, initial condition, and boundary conditions. Our algorithm is meshfree, which is key since meshes become infeasible in higher dimensions. Instead of forming a mesh, the neural network is trained on batches of randomly sampled time and space points. The algorithm is tested on a class of high-dimensional free boundary PDEs, which we are able to accurately solve in up to $200$ dimensions. The algorithm is also tested on a high-dimensional Hamilton-Jacobi-Bellman PDE and Burgers' equation. The deep learning algorithm approximates the general solution to the Burgers' equation for a continuum of different boundary conditions and physical conditions (which can be viewed as a high-dimensional space). We call the algorithm a "Deep Galerkin Method (DGM)" since it is similar in spirit to Galerkin methods, with the solution approximated by a neural network instead of a linear combination of basis functions. In addition, we prove a theorem regarding the approximation power of neural networks for a class of quasilinear parabolic PDEs.

High-dimensional PDEs have been a longstanding computational challenge. We propose to solve high-dimensional PDEs by approximating the solution with a deep neural network which is trained to satisfy the differential operator, initial condition, and boundary conditions. Our algorithm is meshfree, which is key since meshes become infeasible in higher dimensions. Instead of forming a mesh, the neural network is trained on batches of randomly sampled time and space points. The algorithm is tested on a class of high-dimensional free boundary PDEs, which we are able to accurately solve in up to $200$ dimensions. The algorithm is also tested on a high-dimensional Hamilton-Jacobi-Bellman PDE and Burgers' equation. The deep learning algorithm approximates the general solution to the Burgers' equation for a continuum of different boundary conditions and physical conditions (which can be viewed as a high-dimensional space). We call the algorithm a "Deep Galerkin Method (DGM)" since it is similar in spirit to Galerkin methods, with the solution approximated by a neural network instead of a linear combination of basis functions. In addition, we prove a theorem regarding the approximation power of neural networks for a class of quasilinear parabolic PDEs.

The multilevel Monte Carlo path simulation method introduced by Giles ({\it Operations Research}, 56(3):607-617, 2008) exploits strong convergence properties to improve the computational complexity by combining simulations with different levels of resolution. In this paper we analyse its efficiency when using the Milstein discretisation; this has an improved order of strong convergence compared to the standard Euler-Maruyama method, and it is proved that this leads to an improved order of convergence of the variance of the multilevel estimator. Numerical results are also given for basket options to illustrate the relevance of the analysis.

The multilevel Monte Carlo path simulation method introduced by Giles ({\it Operations Research}, 56(3):607-617, 2008) exploits strong convergence properties to improve the computational complexity by combining simulations with different levels of resolution. In this paper we analyse its efficiency when using the Milstein discretisation; this has an improved order of strong convergence compared to the standard Euler-Maruyama method, and it is proved that this leads to an improved order of convergence of the variance of the multilevel estimator. Numerical results are also given for basket options to illustrate the relevance of the analysis.

We present a new and easy-to-implement sequential sampling method for CGMY processes with either finite or infinite variation, exploiting the time change representation of the CGMY model and a decomposition of its time change. We find that the time change can be decomposed into two independent components. While the first component is a \emph{finite} \emph{generalized gamma convolution} process whose increments can be sampled by either the exact double CFTP ("coupling from the past") method or an approximation scheme with high speed and accuracy, the second component can easily be made arbitrarily small in the $L^1$ sense. Simulation results show that the proposed method is advantageous over two existing methods under a model calibrated to historical option price data.

We present a new and easy-to-implement sequential sampling method for CGMY processes with either finite or infinite variation, exploiting the time change representation of the CGMY model and a decomposition of its time change. We find that the time change can be decomposed into two independent components. While the first component is a \emph{finite} \emph{generalized gamma convolution} process whose increments can be sampled by either the exact double CFTP ("coupling from the past") method or an approximation scheme with high speed and accuracy, the second component can easily be made arbitrarily small in the $L^1$ sense. Simulation results show that the proposed method is advantageous over two existing methods under a model calibrated to historical option price data.

This article addresses the problem of approximating the price of options on discrete and continuous arithmetic average of the underlying, i.e. discretely and continuously monitored Asian options, in local volatility models. A path-integral-type expression for option prices is obtained using a Brownian bridge representation for the transition density between consecutive sampling times and a Laplace asymptotic formula. In the limit where the sampling time window approaches zero, the option price is found to be approximated by a constrained variational problem on paths in time-price space. We refer to the optimizing path as the most-likely path (MLP). Approximation for the implied normal volatility follows accordingly. The small-time asymptotics and the existence of the MLP are also recovered rigorously using large deviation theory.

This article addresses the problem of approximating the price of options on discrete and continuous arithmetic average of the underlying, i.e. discretely and continuously monitored Asian options, in local volatility models. A path-integral-type expression for option prices is obtained using a Brownian bridge representation for the transition density between consecutive sampling times and a Laplace asymptotic formula. In the limit where the sampling time window approaches zero, the option price is found to be approximated by a constrained variational problem on paths in time-price space. We refer to the optimizing path as the most-likely path (MLP). Approximation for the implied normal volatility follows accordingly. The small-time asymptotics and the existence of the MLP are also recovered rigorously using large deviation theory.

We consider the optimal stopping problem with non-linear $f$-expectation (induced by a BSDE) without making any regularity assumptions on the reward process $\xi$. and with general filtration. We show that the value family can be aggregated by an optional process $Y$. We characterize the process $Y$ as the $\mathcal{E}^f$-Snell envelope of $\xi$. We also establish an infinitesimal characterization of the value process $Y$ in terms of a Reflected BSDE with $\xi$ as the obstacle. To do this, we first establish a comparison theorem for irregular RBSDEs. We give an application to the pricing of American options with irregular pay-off in an imperfect market model.

We consider the optimal stopping problem with non-linear $f$-expectation (induced by a BSDE) without making any regularity assumptions on the reward process $\xi$. and with general filtration. We show that the value family can be aggregated by an optional process $Y$. We characterize the process $Y$ as the $\mathcal{E}^f$-Snell envelope of $\xi$. We also establish an infinitesimal characterization of the value process $Y$ in terms of a Reflected BSDE with $\xi$ as the obstacle. To do this, we first establish a comparison theorem for irregular RBSDEs. We give an application to the pricing of American options with irregular pay-off in an imperfect market model.