-

We introduce a novel class of credit risk models in which the drift of the

survival process of a firm is a linear function of the factors. The prices of

defaultable bonds and credit default swaps (CDS) are linear-rational in the

factors. The price of a CDS option can be uniformly approximated by polynomials

in the factors. Multi-name models can produce simultaneous defaults, generate

positively as well as negatively correlated default intensities, and

accommodate stochastic interest rates. A calibration study illustrates the

versatility of these models by fitting CDS spread time series. A numerical

analysis validates the efficiency of the option price approximation method.

-

The determination of acceptability prices of contingent claims requires the

choice of a stochastic model for the underlying asset price dynamics. Given

this model, optimal bid and ask prices can be found by stochastic optimization.

However, the model for the underlying asset price process is typically based on

data and found by a statistical estimation procedure. We define a confidence

set of possible estimated models by a nonparametric neighborhood of a baseline

model. This neighborhood serves as ambiguity set for a multi-stage stochastic

optimization problem under model uncertainty. We obtain distributionally robust

solutions of the acceptability pricing problem and derive the dual problem

formulation. Moreover, we prove a general large deviations result for the

nested distance, which allows to relate the bid and ask prices under model

ambiguity to the quality of the observed data.

-

We consider the valuation of contingent claims with delayed dynamics in a

Black \& Scholes complete market model. We find a pricing formula that can be

decomposed into terms reflecting the market values of the past and the present,

showing how the valuation of future cashflows cannot abstract away from the

contribution of the past. As a practical application, we provide an explicit

expression for the market value of human capital in a setting with wage

rigidity.

-

We study the small-time behaviour of the rough Bergomi model, introduced by

Bayer, Friz and Gatheral (2016), and prove a large deviations principle for a

rescaled version of the normalised log stock price process, which then allows

us to characterise the small-time behaviour of the implied volatility.

-

We propose a randomised version of the Heston model-a widely used stochastic

volatility model in mathematical finance-assuming that the starting point of

the variance process is a random variable. In such a system, we study the

small-and large-time behaviours of the implied volatility, and show that the

proposed randomisation generates a short-maturity smile much steeper (`with

explosion') than in the standard Heston model, thereby palliating the

deficiency of classical stochastic volatility models in short time. We

precisely quantify the speed of explosion of the smile for short maturities in

terms of the right tail of the initial distribution, and in particular show

that an explosion rate of~$t^\gamma$ ($\gamma\in[0,1/2]$) for the squared

implied volatility--as observed on market data--can be obtained by a suitable

choice of randomisation. The proofs are based on large deviations techniques

and the theory of regular variations.

-

The Multi Variate Mixture Dynamics model is a tractable, dynamical,

arbitrage-free multivariate model characterized by transparency on the

dependence structure, since closed form formulae for terminal correlations,

average correlations and copula function are available. It also allows for

complete decorrelation between assets and instantaneous variances. Each single

asset is modelled according to a lognormal mixture dynamics model, and this

univariate version is widely used in the industry due to its flexibility and

accuracy. The same property holds for the multivariate process of all assets,

whose density is a mixture of multivariate basic densities. This allows for

consistency of single asset and index/portfolio smile. In this paper, we

generalize the MVMD model by introducing shifted dynamics and we propose a

definition of implied correlation under this model. We investigate whether the

model is able to consistently reproduce the implied volatility of FX cross

rates once the single components are calibrated to univariate shifted lognormal

mixture dynamics models. We consider in particular the case of the Chinese

renminbi FX rate, showing that the shifted MVMD model correctly recovers the

CNY/EUR smile given the EUR/USD smile and the USD/CNY smile, thus highlighting

that the model can also work as an arbitrage free volatility smile

extrapolation tool for cross currencies that may not be liquid or fully

observable. We compare the performance of the shifted MVMD model in terms of

implied correlation with those of the shifted Simply Correlated Mixture

Dynamics model where the dynamics of the single assets are connected naively by

introducing correlation among their Brownian motions. Finally, we introduce a

model with uncertain volatilities and correlation. The Markovian projection of

this model is a generalization of the shifted MVMD model.

-

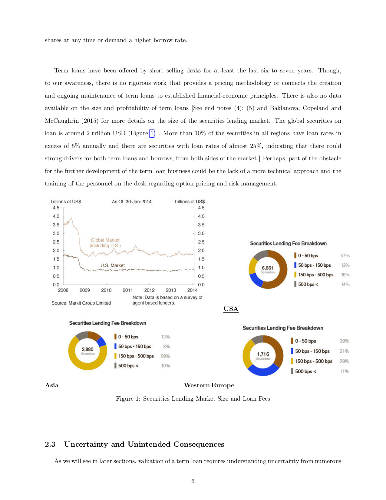

We develop models to price long term loans in the securities lending

business. These longer horizon deals can be viewed as contracts with

optionality embedded in them and can be priced using established methods from

derivatives theory, becoming to our limited knowledge, the first application

that can lead to greater synergies between the operations of derivative and

delta-one trading desks, perhaps even being able to combine certain aspects of

the day to day operations of these seemingly disparate entities. We run

numerical simulations to demonstrate the practical applicability of these

models. These models are part of one of the least explored yet profit laden

areas of modern investment management.

We develop a heuristic that can mitigate the loss of information that sets in

when parameters are estimated first and then the valuation is performed by

directly calculating the valuation using the historical time series. This can

lead to reduced models errors and greater financial stability. We illustrate

how the methodologies developed here could be useful for inventory management.

All these techniques could have applications for dealing with other financial

instruments, non-financial commodities and many forms of uncertainty. An

unintended consequence of our efforts, has become a review of the vast

literature on options pricing, which can be useful for anyone that attempts to

apply the corresponding techniques to the problems mentioned here.

Admittedly, our initial ambitions to produce a normative theory on long term

loan valuations are undone by the present state of affairs in social science

modeling. Though we consider many elements of a securities lending system at

face value, this cannot be termed a positive theory. For now, if it ends up

producing a useful theory, our work is done.

-

We derive valuations of a portfolio of financial instruments from a

securities lending perspective, under different assumptions, and show a

weighting scheme that converges to the true valuation. We illustrate conditions

under which our alternative weighting scheme converges faster to the true

valuation when compared to the minimum variance weighting. This weighting

scheme is applicable in any situation where multiple forecasts are made and we

need a methodology to combine them. Our valuations can be useful either to

derive a bidding strategy for an exclusive auction or to design an appropriate

auction mechanism, depending on which side of the fence a participant sits

(whether the interest is to procure the rights to use a portfolio for making

stock loans such as for a lending desk, or, to obtain additional revenue from a

portfolio such as from the point of view of a long only asset management firm).

Lastly, we run simulations to establish numerical examples for the set of

valuations and for various bidding strategies corresponding to different

auction settings.

-

This paper proposes to model asset price dynamics with a mixture of diffusion

processes where the instantaneous volatility of the underlying diffusion

process contains a random vector. The marginal probability distributions of the

proposed process can match exactly the risk-neutral distributions implied by

both spot vanilla options and forward start options. We can also derive the

explicit pricing formula for derivatives that have a closed-form solution under

Generalized Geometric Brownian Motion.

-

Game contingent claims (GCCs) generalize American contingent claims by

allowing the writer to recall the option as long as it is not exercised, at the

price of paying some penalty. In incomplete markets, an appealing approach is

to analyze GCCs like their European and American counterparts by solving option

holder's and writer's optimal investment problems in the underlying securities.

By this, partial hedging opportunities are taken into account. We extend

results in the literature by solving the stochastic game corresponding to GCCs

with both continuous time stopping and trading. Namely, we construct Nash

equilibria by rewriting the game as a non-zero-sum stopping game in which

players compare payoffs in terms of their exponential utility indifference

values. As a by-product, we also obtain an existence result for the optimal

exercise time of an American claim under utility indifference valuation by

relating it to the corresponding nonlinear Snell envelope.

-

Conditions of Stability for explicit finite difference scheme and some

results of numerical analysis for a unified 2 factor model of structural and

reduced form types for corporate bonds with fixed discrete coupon are provided.

It seems to be difficult to get solution formula for PDE model which

generalizes Agliardi's structural model [1] for discrete coupon bonds into a

unified 2 factor model of structural and reduced form types and we study a

numerical analysis for it by explicit finite difference scheme. These equations

are parabolic equations with 3 variables and they include mixed derivatives, so

the explicit finite difference scheme is not stable in general. We find

conditions for the explicit finite difference scheme to be stable, in the case

that it is stable, numerically compute the price of the bond and analyze its

credit spread and duration.

-

Binomial tree methods (BTM) and explicit difference schemes (EDS) for the

variational inequality model of American options with time dependent

coefficients are studied. When volatility is time dependent, it is not

reasonable to assume that the dynamics of the underlying asset's price forms a

binomial tree if a partition of time interval with equal parts is used. A time

interval partition method that allows binomial tree dynamics of the underlying

asset's price is provided. Conditions under which the prices of American option

by BTM and EDS have the monotonic property on time variable are found. Using

convergence of EDS for variational inequality model of American options to

viscosity solution the decreasing property of the price of American put options

and increasing property of the optimal exercise boundary on time variable are

proved. First, put options are considered. Then the linear homogeneity and

call-put symmetry of the price functions in the BTM and the EDS for the

variational inequality model of American options with time dependent

coefficients are studied and using them call options are studied.

-

We introduce a regularization approach to arbitrage-free factor-model

selection. The considered model selection problem seeks to learn the closest

arbitrage-free HJM-type model to any prespecified factor-model. An asymptotic

solution to this, a priori computationally intractable, problem is represented

as the limit of a 1-parameter family of optimizers to computationally tractable

model selection tasks. Each of these simplified model-selection tasks seeks to

learn the most similar model, to the prescribed factor-model, subject to a

penalty detecting when the reference measure is a local martingale-measure for

the entire underlying financial market. A simple expression for the penalty

terms is obtained in the bond market withing the affine-term structure setting,

and it is used to formulate a deep-learning approach to arbitrage-free affine

term-structure modelling. Numerical implementations are also performed to

evaluate the performance in the bond market.

-

We show that an American put option with delivery lags can be decomposed as a

European put option and another American-style derivative. The latter is an

option for which the investor receives the Greek Theta of the corresponding

European option as the running payoff, and decides an optimal stopping time to

terminate the contract. Based on the this decomposition, we further show that

the associated optimal exercise boundary exists, and is a strictly increasing

and smooth curve. We also analyze its asymptotic behavior for both large

maturity and small time lag using the free-boundary method.

-

Contrary to the common view that exact pricing is prohibitive owing to the

curse of dimensionality, this study proposes an efficient and unified method

for pricing options under multivariate Black-Scholes-Merton (BSM) models, such

as the basket, spread, and Asian options. The option price is expressed as a

quadrature integration of analytic multi-asset BSM prices under a single

Brownian motion. Then the state space is rotated in such a way that the

quadrature requires much coarser nodes than it would otherwise or low varying

dimensions are reduced. The accuracy and efficiency of the method is

illustrated through various numerical experiments.

-

The purpose of this paper is to analyze the problem of option pricing when

the short rate follows subdiffusive fractional Merton model. We incorporate the

stochastic nature of the short rate in our option valuation model and derive

explicit formula for call and put option and discuss the corresponding

fractional Black-Scholes equation. We present some properties of this pricing

model for the cases of $\alpha$ and $H$. Moreover, the numerical simulations

illustrate that our model is flexible and easy to implement.

-

Kristensen and Mele (2011) developed a new approach to obtain closed-form

approximations to continuous-time derivatives pricing models. The approach uses

a power series expansion of the pricing bias between an intractable model and

some known auxiliary model. Since the resulting approximation formula has

closed-form it is straightforward to obtain approximations of greeks. In this

thesis I will introduce Kristensen and Mele's methods and apply it to a variety

of stochastic volatility models of European style options as well as a model

for commodity futures. The focus of this thesis is the effect of different

model choices and different model parameter values on the numerical stability

of Kristensen and Mele's approximation.

-

Emerging market hard-currency bonds are an asset class of growing importance,

and contain exposure to an EM sovereign and the underlying industry. The

authors investigate how to model this as a modification of the well-known

first-to-default (FtD) basket, using the structural model, and find the

approach feasible.

-

We characterize the price of an Asian option, a financial contract, as a

fixed-point of a non-linear operator. In recent years, there has been interest

in incorporating changes of regime into the parameters describing the evolution

of the underlying asset price, namely the interest rate and the volatility, to

model sudden exogenous events in the economy. Asian options are particularly

interesting because the payoff depends on the integrated asset price. We study

the case of both floating- and fixed-strike Asian call options with arithmetic

averaging when the asset follows a regime-switching geometric Brownian motion

with coefficients that depend on a Markov chain. The typical approach to

finding the value of a financial option is to solve an associated system of

coupled partial differential equations. Alternatively, we propose an iterative

procedure that converges to the value of this contract with geometric rate

using a classical fixed-point theorem.

-

Within the context of the banking-related literature on contingent

convertible bonds, we comprehensively formalise the design and features of a

relatively new type of insurance-linked security, called a contingent

convertible catastrophe bond (CocoCat). We begin with a discussion of its

design and compare its relative merits to catastrophe bonds and

catastrophe-equity puts. Subsequently, we derive analytical valuation formulae

for index-linked CocoCats under the assumption of independence between natural

catastrophe and financial markets risks. We model natural catastrophe losses by

a time-inhomogeneous compound Poisson process, with the interest-rate process

governed by the Longstaff model. By using an exponential change of measure on

the loss process, as well as a Girsanov-like transformation to synthetically

remove the correlation between the share and interest-rate processes, we obtain

these analytical formulae. Using selected parameter values in line with earlier

research, we empirically analyse our valuation formulae for index-linked

CocoCats. An analysis of the results reveals that the CocoCat prices are most

sensitive to changing interest-rates, conversion fractions and the threshold

levels defining the trigger times.

-

Contingent Convertible bonds (CoCos) are debt instruments that convert into

equity or are written down in times of distress. Existing pricing models assume

conversion triggers based on market prices and on the assumption that markets

can always observe all relevant firm information. But all Cocos issued so far

have triggers based on accounting ratios and/or regulatory intervention. We

incorporate that markets receive information through noisy accounting reports

issued at discrete time instants, which allows us to distinguish between market

and accounting values, and between automatic triggers and regulator-mandated

conversions. Our second contribution is to incorporate that coupon payments are

contingent too: their payment is conditional on the Maximum Distributable

Amount not being exceeded. We examine the impact of CoCo design parameters,

asset volatility and accounting noise on the price of a CoCo; and investigate

the interaction between CoCo design features, the capital structure of the

issuing bank and their implications for risk taking and investment incentives.

Finally, we use our model to explain the crash in CoCo prices after Deutsche

Bank's profit warning in February 2016.

-

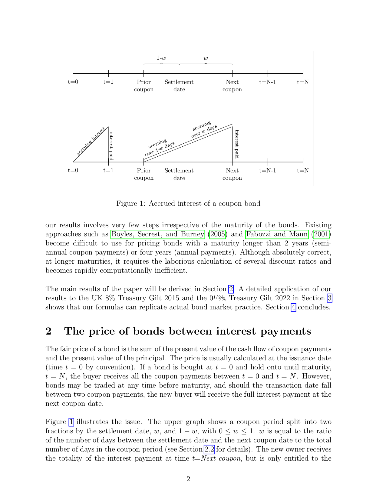

We derive a closed-form formula for computing bond prices between coupon

payments. Our results cover both the `Treasury' and the `Street' pricing

methods used by sovereign and corporate issuers. We apply our formulas to two

UK gilts, the 8% Treasury Gilt 2015, and the 0.5% Treasury Gilt 2022, and show

that we can obtain the dirty price of these bonds at any date with a minimum of

calculations, and without intensive computational resources.

-

Recent empirical studies suggest that the volatilities associated with

financial time series exhibit short-range correlations. This entails that the

volatility process is very rough and its autocorrelation exhibits sharp decay

at the origin. Another classic stylistic feature often assumed for the

volatility is that it is mean reverting. In this paper it is shown that the

price impact of a rapidly mean reverting rough volatility model coincides with

that associated with fast mean reverting Markov stochastic volatility models.

This reconciles the empirical observation of rough volatility paths with the

good fit of the implied volatility surface to models of fast mean reverting

Markov volatilities. Moreover, the result conforms with recent numerical

results regarding rough stochastic volatility models. It extends the scope of

models for which the asymptotic results of fast mean reverting Markov

volatilities are valid. The paper concludes with a general discussion of

fractional volatility asymptotics and their interrelation. The regimes

discussed there include fast and slow volatility factors with strong or small

volatility fluctuations and with the limits not commuting in general. The

notion of a characteristic term structure exponent is introduced, this exponent

governs the implied volatility term structure in the various asymptotic

regimes.

-

Recent empirical studies suggest that the volatility of an underlying price

process may have correlations that decay slowly under certain market

conditions. In this paper, the volatility is modeled as a stationary process

with long-range correlation properties in order to capture such a situation,

and we consider European option pricing. This means that the volatility process

is neither a Markov process nor a martingale. However, by exploiting the fact

that the price process is still a semimartingale and accordingly using the

martingale method, we can obtain an analytical expression for the option price

in the regime where the volatility process is fast mean-reverting. The

volatility process is modeled as a smooth and bounded function of a fractional

Ornstein-Uhlenbeck process. We give the expression for the implied volatility,

which has a fractional term structure.

-

We describe a robust calibration algorithm of a set of SSVI slices (i.e. a

set of 3 SSVI parameters $\theta, \rho, \varphi$ attached to each option

maturity available on the market), which grants that these slices are free of

Butterfly and Calendar-Spread arbitrage. Given such a set of consistent SSVI

parameters, we show that the most natural interpolation/extrapolation of the

parameters provides a full continuous volatility surface free of arbitrage. The

numerical implementation is straightforward, robust and quick, yielding an

effective, parsimonious solution to the smile problem, which has the potential

to become a benchmark one.

We introduce a novel class of credit risk models in which the drift of the survival process of a firm is a linear function of the factors. The prices of defaultable bonds and credit default swaps (CDS) are linear-rational in the factors. The price of a CDS option can be uniformly approximated by polynomials in the factors. Multi-name models can produce simultaneous defaults, generate positively as well as negatively correlated default intensities, and accommodate stochastic interest rates. A calibration study illustrates the versatility of these models by fitting CDS spread time series. A numerical analysis validates the efficiency of the option price approximation method.

We introduce a novel class of credit risk models in which the drift of the survival process of a firm is a linear function of the factors. The prices of defaultable bonds and credit default swaps (CDS) are linear-rational in the factors. The price of a CDS option can be uniformly approximated by polynomials in the factors. Multi-name models can produce simultaneous defaults, generate positively as well as negatively correlated default intensities, and accommodate stochastic interest rates. A calibration study illustrates the versatility of these models by fitting CDS spread time series. A numerical analysis validates the efficiency of the option price approximation method.

The determination of acceptability prices of contingent claims requires the choice of a stochastic model for the underlying asset price dynamics. Given this model, optimal bid and ask prices can be found by stochastic optimization. However, the model for the underlying asset price process is typically based on data and found by a statistical estimation procedure. We define a confidence set of possible estimated models by a nonparametric neighborhood of a baseline model. This neighborhood serves as ambiguity set for a multi-stage stochastic optimization problem under model uncertainty. We obtain distributionally robust solutions of the acceptability pricing problem and derive the dual problem formulation. Moreover, we prove a general large deviations result for the nested distance, which allows to relate the bid and ask prices under model ambiguity to the quality of the observed data.

The determination of acceptability prices of contingent claims requires the choice of a stochastic model for the underlying asset price dynamics. Given this model, optimal bid and ask prices can be found by stochastic optimization. However, the model for the underlying asset price process is typically based on data and found by a statistical estimation procedure. We define a confidence set of possible estimated models by a nonparametric neighborhood of a baseline model. This neighborhood serves as ambiguity set for a multi-stage stochastic optimization problem under model uncertainty. We obtain distributionally robust solutions of the acceptability pricing problem and derive the dual problem formulation. Moreover, we prove a general large deviations result for the nested distance, which allows to relate the bid and ask prices under model ambiguity to the quality of the observed data.

We consider the valuation of contingent claims with delayed dynamics in a Black \& Scholes complete market model. We find a pricing formula that can be decomposed into terms reflecting the market values of the past and the present, showing how the valuation of future cashflows cannot abstract away from the contribution of the past. As a practical application, we provide an explicit expression for the market value of human capital in a setting with wage rigidity.

We consider the valuation of contingent claims with delayed dynamics in a Black \& Scholes complete market model. We find a pricing formula that can be decomposed into terms reflecting the market values of the past and the present, showing how the valuation of future cashflows cannot abstract away from the contribution of the past. As a practical application, we provide an explicit expression for the market value of human capital in a setting with wage rigidity.

We study the small-time behaviour of the rough Bergomi model, introduced by Bayer, Friz and Gatheral (2016), and prove a large deviations principle for a rescaled version of the normalised log stock price process, which then allows us to characterise the small-time behaviour of the implied volatility.

We study the small-time behaviour of the rough Bergomi model, introduced by Bayer, Friz and Gatheral (2016), and prove a large deviations principle for a rescaled version of the normalised log stock price process, which then allows us to characterise the small-time behaviour of the implied volatility.

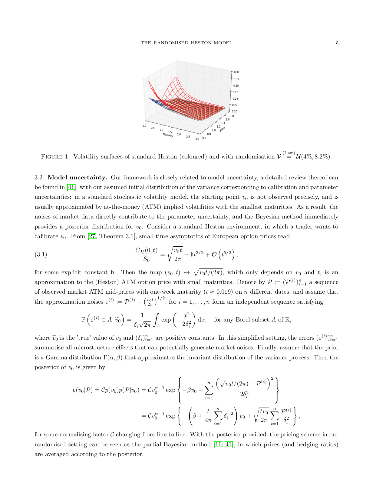

We propose a randomised version of the Heston model-a widely used stochastic volatility model in mathematical finance-assuming that the starting point of the variance process is a random variable. In such a system, we study the small-and large-time behaviours of the implied volatility, and show that the proposed randomisation generates a short-maturity smile much steeper (`with explosion') than in the standard Heston model, thereby palliating the deficiency of classical stochastic volatility models in short time. We precisely quantify the speed of explosion of the smile for short maturities in terms of the right tail of the initial distribution, and in particular show that an explosion rate of~$t^\gamma$ ($\gamma\in[0,1/2]$) for the squared implied volatility--as observed on market data--can be obtained by a suitable choice of randomisation. The proofs are based on large deviations techniques and the theory of regular variations.

We propose a randomised version of the Heston model-a widely used stochastic volatility model in mathematical finance-assuming that the starting point of the variance process is a random variable. In such a system, we study the small-and large-time behaviours of the implied volatility, and show that the proposed randomisation generates a short-maturity smile much steeper (`with explosion') than in the standard Heston model, thereby palliating the deficiency of classical stochastic volatility models in short time. We precisely quantify the speed of explosion of the smile for short maturities in terms of the right tail of the initial distribution, and in particular show that an explosion rate of~$t^\gamma$ ($\gamma\in[0,1/2]$) for the squared implied volatility--as observed on market data--can be obtained by a suitable choice of randomisation. The proofs are based on large deviations techniques and the theory of regular variations.

The Multi Variate Mixture Dynamics model is a tractable, dynamical, arbitrage-free multivariate model characterized by transparency on the dependence structure, since closed form formulae for terminal correlations, average correlations and copula function are available. It also allows for complete decorrelation between assets and instantaneous variances. Each single asset is modelled according to a lognormal mixture dynamics model, and this univariate version is widely used in the industry due to its flexibility and accuracy. The same property holds for the multivariate process of all assets, whose density is a mixture of multivariate basic densities. This allows for consistency of single asset and index/portfolio smile. In this paper, we generalize the MVMD model by introducing shifted dynamics and we propose a definition of implied correlation under this model. We investigate whether the model is able to consistently reproduce the implied volatility of FX cross rates once the single components are calibrated to univariate shifted lognormal mixture dynamics models. We consider in particular the case of the Chinese renminbi FX rate, showing that the shifted MVMD model correctly recovers the CNY/EUR smile given the EUR/USD smile and the USD/CNY smile, thus highlighting that the model can also work as an arbitrage free volatility smile extrapolation tool for cross currencies that may not be liquid or fully observable. We compare the performance of the shifted MVMD model in terms of implied correlation with those of the shifted Simply Correlated Mixture Dynamics model where the dynamics of the single assets are connected naively by introducing correlation among their Brownian motions. Finally, we introduce a model with uncertain volatilities and correlation. The Markovian projection of this model is a generalization of the shifted MVMD model.

The Multi Variate Mixture Dynamics model is a tractable, dynamical, arbitrage-free multivariate model characterized by transparency on the dependence structure, since closed form formulae for terminal correlations, average correlations and copula function are available. It also allows for complete decorrelation between assets and instantaneous variances. Each single asset is modelled according to a lognormal mixture dynamics model, and this univariate version is widely used in the industry due to its flexibility and accuracy. The same property holds for the multivariate process of all assets, whose density is a mixture of multivariate basic densities. This allows for consistency of single asset and index/portfolio smile. In this paper, we generalize the MVMD model by introducing shifted dynamics and we propose a definition of implied correlation under this model. We investigate whether the model is able to consistently reproduce the implied volatility of FX cross rates once the single components are calibrated to univariate shifted lognormal mixture dynamics models. We consider in particular the case of the Chinese renminbi FX rate, showing that the shifted MVMD model correctly recovers the CNY/EUR smile given the EUR/USD smile and the USD/CNY smile, thus highlighting that the model can also work as an arbitrage free volatility smile extrapolation tool for cross currencies that may not be liquid or fully observable. We compare the performance of the shifted MVMD model in terms of implied correlation with those of the shifted Simply Correlated Mixture Dynamics model where the dynamics of the single assets are connected naively by introducing correlation among their Brownian motions. Finally, we introduce a model with uncertain volatilities and correlation. The Markovian projection of this model is a generalization of the shifted MVMD model.

We develop models to price long term loans in the securities lending business. These longer horizon deals can be viewed as contracts with optionality embedded in them and can be priced using established methods from derivatives theory, becoming to our limited knowledge, the first application that can lead to greater synergies between the operations of derivative and delta-one trading desks, perhaps even being able to combine certain aspects of the day to day operations of these seemingly disparate entities. We run numerical simulations to demonstrate the practical applicability of these models. These models are part of one of the least explored yet profit laden areas of modern investment management. We develop a heuristic that can mitigate the loss of information that sets in when parameters are estimated first and then the valuation is performed by directly calculating the valuation using the historical time series. This can lead to reduced models errors and greater financial stability. We illustrate how the methodologies developed here could be useful for inventory management. All these techniques could have applications for dealing with other financial instruments, non-financial commodities and many forms of uncertainty. An unintended consequence of our efforts, has become a review of the vast literature on options pricing, which can be useful for anyone that attempts to apply the corresponding techniques to the problems mentioned here. Admittedly, our initial ambitions to produce a normative theory on long term loan valuations are undone by the present state of affairs in social science modeling. Though we consider many elements of a securities lending system at face value, this cannot be termed a positive theory. For now, if it ends up producing a useful theory, our work is done.

We develop models to price long term loans in the securities lending business. These longer horizon deals can be viewed as contracts with optionality embedded in them and can be priced using established methods from derivatives theory, becoming to our limited knowledge, the first application that can lead to greater synergies between the operations of derivative and delta-one trading desks, perhaps even being able to combine certain aspects of the day to day operations of these seemingly disparate entities. We run numerical simulations to demonstrate the practical applicability of these models. These models are part of one of the least explored yet profit laden areas of modern investment management. We develop a heuristic that can mitigate the loss of information that sets in when parameters are estimated first and then the valuation is performed by directly calculating the valuation using the historical time series. This can lead to reduced models errors and greater financial stability. We illustrate how the methodologies developed here could be useful for inventory management. All these techniques could have applications for dealing with other financial instruments, non-financial commodities and many forms of uncertainty. An unintended consequence of our efforts, has become a review of the vast literature on options pricing, which can be useful for anyone that attempts to apply the corresponding techniques to the problems mentioned here. Admittedly, our initial ambitions to produce a normative theory on long term loan valuations are undone by the present state of affairs in social science modeling. Though we consider many elements of a securities lending system at face value, this cannot be termed a positive theory. For now, if it ends up producing a useful theory, our work is done.

We derive valuations of a portfolio of financial instruments from a securities lending perspective, under different assumptions, and show a weighting scheme that converges to the true valuation. We illustrate conditions under which our alternative weighting scheme converges faster to the true valuation when compared to the minimum variance weighting. This weighting scheme is applicable in any situation where multiple forecasts are made and we need a methodology to combine them. Our valuations can be useful either to derive a bidding strategy for an exclusive auction or to design an appropriate auction mechanism, depending on which side of the fence a participant sits (whether the interest is to procure the rights to use a portfolio for making stock loans such as for a lending desk, or, to obtain additional revenue from a portfolio such as from the point of view of a long only asset management firm). Lastly, we run simulations to establish numerical examples for the set of valuations and for various bidding strategies corresponding to different auction settings.

We derive valuations of a portfolio of financial instruments from a securities lending perspective, under different assumptions, and show a weighting scheme that converges to the true valuation. We illustrate conditions under which our alternative weighting scheme converges faster to the true valuation when compared to the minimum variance weighting. This weighting scheme is applicable in any situation where multiple forecasts are made and we need a methodology to combine them. Our valuations can be useful either to derive a bidding strategy for an exclusive auction or to design an appropriate auction mechanism, depending on which side of the fence a participant sits (whether the interest is to procure the rights to use a portfolio for making stock loans such as for a lending desk, or, to obtain additional revenue from a portfolio such as from the point of view of a long only asset management firm). Lastly, we run simulations to establish numerical examples for the set of valuations and for various bidding strategies corresponding to different auction settings.

This paper proposes to model asset price dynamics with a mixture of diffusion processes where the instantaneous volatility of the underlying diffusion process contains a random vector. The marginal probability distributions of the proposed process can match exactly the risk-neutral distributions implied by both spot vanilla options and forward start options. We can also derive the explicit pricing formula for derivatives that have a closed-form solution under Generalized Geometric Brownian Motion.

This paper proposes to model asset price dynamics with a mixture of diffusion processes where the instantaneous volatility of the underlying diffusion process contains a random vector. The marginal probability distributions of the proposed process can match exactly the risk-neutral distributions implied by both spot vanilla options and forward start options. We can also derive the explicit pricing formula for derivatives that have a closed-form solution under Generalized Geometric Brownian Motion.

Game contingent claims (GCCs) generalize American contingent claims by allowing the writer to recall the option as long as it is not exercised, at the price of paying some penalty. In incomplete markets, an appealing approach is to analyze GCCs like their European and American counterparts by solving option holder's and writer's optimal investment problems in the underlying securities. By this, partial hedging opportunities are taken into account. We extend results in the literature by solving the stochastic game corresponding to GCCs with both continuous time stopping and trading. Namely, we construct Nash equilibria by rewriting the game as a non-zero-sum stopping game in which players compare payoffs in terms of their exponential utility indifference values. As a by-product, we also obtain an existence result for the optimal exercise time of an American claim under utility indifference valuation by relating it to the corresponding nonlinear Snell envelope.

Game contingent claims (GCCs) generalize American contingent claims by allowing the writer to recall the option as long as it is not exercised, at the price of paying some penalty. In incomplete markets, an appealing approach is to analyze GCCs like their European and American counterparts by solving option holder's and writer's optimal investment problems in the underlying securities. By this, partial hedging opportunities are taken into account. We extend results in the literature by solving the stochastic game corresponding to GCCs with both continuous time stopping and trading. Namely, we construct Nash equilibria by rewriting the game as a non-zero-sum stopping game in which players compare payoffs in terms of their exponential utility indifference values. As a by-product, we also obtain an existence result for the optimal exercise time of an American claim under utility indifference valuation by relating it to the corresponding nonlinear Snell envelope.

Binomial tree methods (BTM) and explicit difference schemes (EDS) for the variational inequality model of American options with time dependent coefficients are studied. When volatility is time dependent, it is not reasonable to assume that the dynamics of the underlying asset's price forms a binomial tree if a partition of time interval with equal parts is used. A time interval partition method that allows binomial tree dynamics of the underlying asset's price is provided. Conditions under which the prices of American option by BTM and EDS have the monotonic property on time variable are found. Using convergence of EDS for variational inequality model of American options to viscosity solution the decreasing property of the price of American put options and increasing property of the optimal exercise boundary on time variable are proved. First, put options are considered. Then the linear homogeneity and call-put symmetry of the price functions in the BTM and the EDS for the variational inequality model of American options with time dependent coefficients are studied and using them call options are studied.

Binomial tree methods (BTM) and explicit difference schemes (EDS) for the variational inequality model of American options with time dependent coefficients are studied. When volatility is time dependent, it is not reasonable to assume that the dynamics of the underlying asset's price forms a binomial tree if a partition of time interval with equal parts is used. A time interval partition method that allows binomial tree dynamics of the underlying asset's price is provided. Conditions under which the prices of American option by BTM and EDS have the monotonic property on time variable are found. Using convergence of EDS for variational inequality model of American options to viscosity solution the decreasing property of the price of American put options and increasing property of the optimal exercise boundary on time variable are proved. First, put options are considered. Then the linear homogeneity and call-put symmetry of the price functions in the BTM and the EDS for the variational inequality model of American options with time dependent coefficients are studied and using them call options are studied.

We characterize the price of an Asian option, a financial contract, as a fixed-point of a non-linear operator. In recent years, there has been interest in incorporating changes of regime into the parameters describing the evolution of the underlying asset price, namely the interest rate and the volatility, to model sudden exogenous events in the economy. Asian options are particularly interesting because the payoff depends on the integrated asset price. We study the case of both floating- and fixed-strike Asian call options with arithmetic averaging when the asset follows a regime-switching geometric Brownian motion with coefficients that depend on a Markov chain. The typical approach to finding the value of a financial option is to solve an associated system of coupled partial differential equations. Alternatively, we propose an iterative procedure that converges to the value of this contract with geometric rate using a classical fixed-point theorem.

We characterize the price of an Asian option, a financial contract, as a fixed-point of a non-linear operator. In recent years, there has been interest in incorporating changes of regime into the parameters describing the evolution of the underlying asset price, namely the interest rate and the volatility, to model sudden exogenous events in the economy. Asian options are particularly interesting because the payoff depends on the integrated asset price. We study the case of both floating- and fixed-strike Asian call options with arithmetic averaging when the asset follows a regime-switching geometric Brownian motion with coefficients that depend on a Markov chain. The typical approach to finding the value of a financial option is to solve an associated system of coupled partial differential equations. Alternatively, we propose an iterative procedure that converges to the value of this contract with geometric rate using a classical fixed-point theorem.

We derive a closed-form formula for computing bond prices between coupon payments. Our results cover both the `Treasury' and the `Street' pricing methods used by sovereign and corporate issuers. We apply our formulas to two UK gilts, the 8% Treasury Gilt 2015, and the 0.5% Treasury Gilt 2022, and show that we can obtain the dirty price of these bonds at any date with a minimum of calculations, and without intensive computational resources.

We derive a closed-form formula for computing bond prices between coupon payments. Our results cover both the `Treasury' and the `Street' pricing methods used by sovereign and corporate issuers. We apply our formulas to two UK gilts, the 8% Treasury Gilt 2015, and the 0.5% Treasury Gilt 2022, and show that we can obtain the dirty price of these bonds at any date with a minimum of calculations, and without intensive computational resources.

Recent empirical studies suggest that the volatilities associated with financial time series exhibit short-range correlations. This entails that the volatility process is very rough and its autocorrelation exhibits sharp decay at the origin. Another classic stylistic feature often assumed for the volatility is that it is mean reverting. In this paper it is shown that the price impact of a rapidly mean reverting rough volatility model coincides with that associated with fast mean reverting Markov stochastic volatility models. This reconciles the empirical observation of rough volatility paths with the good fit of the implied volatility surface to models of fast mean reverting Markov volatilities. Moreover, the result conforms with recent numerical results regarding rough stochastic volatility models. It extends the scope of models for which the asymptotic results of fast mean reverting Markov volatilities are valid. The paper concludes with a general discussion of fractional volatility asymptotics and their interrelation. The regimes discussed there include fast and slow volatility factors with strong or small volatility fluctuations and with the limits not commuting in general. The notion of a characteristic term structure exponent is introduced, this exponent governs the implied volatility term structure in the various asymptotic regimes.

Recent empirical studies suggest that the volatilities associated with financial time series exhibit short-range correlations. This entails that the volatility process is very rough and its autocorrelation exhibits sharp decay at the origin. Another classic stylistic feature often assumed for the volatility is that it is mean reverting. In this paper it is shown that the price impact of a rapidly mean reverting rough volatility model coincides with that associated with fast mean reverting Markov stochastic volatility models. This reconciles the empirical observation of rough volatility paths with the good fit of the implied volatility surface to models of fast mean reverting Markov volatilities. Moreover, the result conforms with recent numerical results regarding rough stochastic volatility models. It extends the scope of models for which the asymptotic results of fast mean reverting Markov volatilities are valid. The paper concludes with a general discussion of fractional volatility asymptotics and their interrelation. The regimes discussed there include fast and slow volatility factors with strong or small volatility fluctuations and with the limits not commuting in general. The notion of a characteristic term structure exponent is introduced, this exponent governs the implied volatility term structure in the various asymptotic regimes.

Recent empirical studies suggest that the volatility of an underlying price process may have correlations that decay slowly under certain market conditions. In this paper, the volatility is modeled as a stationary process with long-range correlation properties in order to capture such a situation, and we consider European option pricing. This means that the volatility process is neither a Markov process nor a martingale. However, by exploiting the fact that the price process is still a semimartingale and accordingly using the martingale method, we can obtain an analytical expression for the option price in the regime where the volatility process is fast mean-reverting. The volatility process is modeled as a smooth and bounded function of a fractional Ornstein-Uhlenbeck process. We give the expression for the implied volatility, which has a fractional term structure.

Recent empirical studies suggest that the volatility of an underlying price process may have correlations that decay slowly under certain market conditions. In this paper, the volatility is modeled as a stationary process with long-range correlation properties in order to capture such a situation, and we consider European option pricing. This means that the volatility process is neither a Markov process nor a martingale. However, by exploiting the fact that the price process is still a semimartingale and accordingly using the martingale method, we can obtain an analytical expression for the option price in the regime where the volatility process is fast mean-reverting. The volatility process is modeled as a smooth and bounded function of a fractional Ornstein-Uhlenbeck process. We give the expression for the implied volatility, which has a fractional term structure.