-

We consider the problem of stopping a diffusion process with a payoff

functional that renders the problem time-inconsistent. We study stopping

decisions of naive agents who reoptimize continuously in time, as well as

equilibrium strategies of sophisticated agents who anticipate but lack control

over their future selves' behaviors. When the state process is one dimensional

and the payoff functional satisfies some regularity conditions, we prove that

any equilibrium can be obtained as a fixed point of an operator. This operator

represents strategic reasoning that takes the future selves' behaviors into

account. We then apply the general results to the case when the agents distort

probability and the diffusion process is a geometric Brownian motion. The

problem is inherently time-inconsistent as the level of distortion of a same

event changes over time. We show how the strategic reasoning may turn a naive

agent into a sophisticated one. Moreover, we derive stopping strategies of the

two types of agent for various parameter specifications of the problem,

illustrating rich behaviors beyond the extreme ones such as "never-stopping" or

"never-starting".

-

We model learning in a continuous-time Brownian setting where there is prior

ambiguity. The associated model of preference values robustness and is

time-consistent. It is applied to study optimal learning when the choice

between actions can be postponed, at a per-unit-time cost, in order to observe

a signal that provides information about an unknown parameter. The

corresponding optimal stopping problem is solved in closed-form, with a focus

on two specific settings: Ellsberg's two-urn thought experiment expanded to

allow learning before the choice of bets, and a robust version of the classical

problem of sequential testing of two simple hypotheses about the unknown drift

of a Wiener process. In both cases, the link between robustness and the demand

for learning is studied.

-

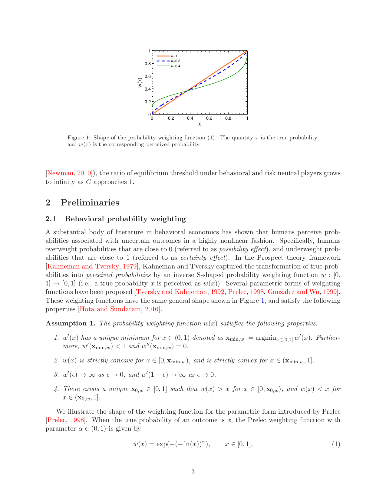

We study decentralized protection strategies against

Susceptible-Infected-Susceptible (SIS) epidemics on networks. We consider a

population game framework where nodes choose whether or not to vaccinate

themselves, and the epidemic risk is defined as the infection probability at

the endemic state of the epidemic under a degree-based mean-field

approximation. Motivated by studies in behavioral economics showing that humans

perceive probabilities and risks in a nonlinear fashion, we specifically

examine the impacts of such misperceptions on the Nash equilibrium protection

strategies. We first establish the existence and uniqueness of a threshold

equilibrium where nodes with degrees larger than a certain threshold vaccinate.

When the vaccination cost is sufficiently high, we show that behavioral biases

cause fewer players to vaccinate, and vice versa. We quantify this effect for a

class of networks with power-law degree distributions by proving tight bounds

on the ratio of equilibrium thresholds under behavioral and true perceptions of

probabilities. We further characterize the socially optimal vaccination policy

and investigate the inefficiency of Nash equilibrium.

-

How do macro-financial shocks affect investor behavior and market dynamics?

Recent evidence on experience effects suggests a long-lasting influence of

personally experienced outcomes on investor beliefs and investment, but also

significant differences across older and younger generations. We formalize

experience-based learning in an OLG model, where different cross-cohort

experiences generate persistent heterogeneity in beliefs, portfolio choices,

and trade. The model allows us to characterize a novel link between investor

demographics and the dependence of prices on past dividends, while also

generating known features of asset prices, such as excess volatility and return

predictability. The model produces new implications for the cross-section of

asset holdings, trade volume, and investors' heterogenous responses to recent

financial crises, which we show to be in line with the data.

-

We reconsider the microeconomic foundations of financial economics. Motivated

by the importance of Knightian Uncertainty in markets, we present a model that

does not carry any probabilistic structure ex ante, yet is based on a common

order. We derive the fundamental equivalence of economic viability of asset

prices and absence of arbitrage. We also obtain a modified version of the

Fundamental Theorem of Asset Pricing using the notion of sublinear pricing

measures. Different versions of the Efficient Market Hypothesis are related to

the assumptions one is willing to impose on the common order.

-

In Chinese societies, superstition is of paramount importance, and vehicle

license plates with desirable numbers can fetch very high prices in auctions.

Unlike other valuable items, license plates are not allocated an estimated

price before auction. I propose that the task of predicting plate prices can be

viewed as a natural language processing (NLP) task, as the value depends on the

meaning of each individual character on the plate and its semantics. I

construct a deep recurrent neural network (RNN) to predict the prices of

vehicle license plates in Hong Kong, based on the characters on a plate. I

demonstrate the importance of having a deep network and of retraining.

Evaluated on 13 years of historical auction prices, the deep RNN's predictions

can explain over 80 percent of price variations, outperforming previous models

by a significant margin. I also demonstrate how the model can be extended to

become a search engine for plates and to provide estimates of the expected

price distribution.

-

The structure of the International Trade Network (ITN), whose nodes and links

represent world countries and their trade relations respectively, affects key

economic processes worldwide, including globalization, economic integration,

industrial production, and the propagation of shocks and instabilities.

Characterizing the ITN via a simple yet accurate model is an open problem. The

traditional Gravity Model (GM) successfully reproduces the volume of trade

between connected countries, using macroeconomic properties such as GDP,

geographic distance, and possibly other factors. However, it predicts a network

with complete or homogeneous topology, thus failing to reproduce the highly

heterogeneous structure of the ITN. On the other hand, recent maximum-entropy

network models successfully reproduce the complex topology of the ITN, but

provide no information about trade volumes. Here we integrate these two

currently incompatible approaches via the introduction of an Enhanced Gravity

Model (EGM) of trade. The EGM is the simplest model combining the GM with the

network approach within a maximum-entropy framework. Via a unified and

principled mechanism that is transparent enough to be generalized to any

economic network, the EGM provides a new econometric framework wherein trade

probabilities and trade volumes can be separately controlled by any combination

of dyadic and country-specific macroeconomic variables. The model successfully

reproduces both the global topology and the local link weights of the ITN,

parsimoniously reconciling the conflicting approaches. It also indicates that

the probability that any two countries trade a certain volume should follow a

geometric or exponential distribution with an additional point mass at zero

volume.

-

In this paper, we extend the optimal securitisation model of Pag\`es [50] and

Possama\"i and Pag\`es [51] between an investor and a bank to a setting

allowing both moral hazard and adverse selection. Following the recent approach

to these problems of Cvitani\'c, Wan and Yang [14], we characterise explicitly

and rigorously the so-called credible set of the continuation and temptation

values of the bank, and obtain the value function of the investor as well as

the optimal contracts through a recursive system of first-order variational

inequalities with gradient constraints. We provide a detailed discussion of the

properties of the optimal menu of contracts.

-

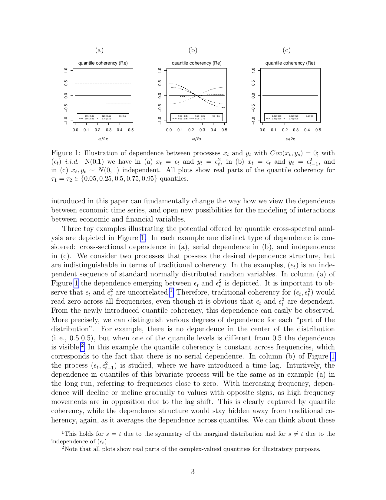

In this paper, we introduce quantile coherency to measure general dependence

structures emerging in the joint distribution in the frequency domain and argue

that this type of dependence is natural for economic time series but remains

invisible when only the traditional analysis is employed. We define estimators

which capture the general dependence structure, provide a detailed analysis of

their asymptotic properties and discuss how to conduct inference for a general

class of possibly nonlinear processes. In an empirical illustration we examine

the dependence of bivariate stock market returns and shed new light on

measurement of tail risk in financial markets. We also provide a modelling

exercise to illustrate how applied researchers can benefit from using quantile

coherency when assessing time series models.

-

A set of data with positive values follows a Pareto distribution if the

log-log plot of value versus rank is approximately a straight line. A Pareto

distribution satisfies Zipf's law if the log-log plot has a slope of -1. Since

many types of ranked data follow Zipf's law, it is considered a form of

universality. We propose a mathematical explanation for this phenomenon based

on Atlas models and first-order models, systems of positive continuous

semimartingales with parameters that depend only on rank. We show that the

stable distribution of an Atlas model will follow Zipf's law if and only if two

natural conditions, conservation and completeness, are satisfied. Since Atlas

models and first-order models can be constructed to approximate systems of

time-dependent rank-based data, our results can explain the universality of

Zipf's law for such systems. However, ranked data generated by other means may

follow non-Zipfian Pareto distributions. Hence, our results explain why Zipf's

law holds for word frequency, firm size, household wealth, and city size, while

it does not hold for earthquake magnitude, cumulative book sales, the intensity

of solar flares, and the intensity of wars, all of which follow non-Zipfian

Pareto distributions.

-

This paper provides a comprehensive analysis of welfare measures when

oligopolistic firms face multiple policy interventions and external changes

under general forms of market demands, production costs, and imperfect

competition. We present our results in terms of two welfare measures, namely,

marginal cost of public funds and incidence, in relation to multi-dimensional

pass-through. Our arguments are best understood with two-dimensional taxation

where homogeneous firms face unit and ad valorem taxes. The first part of the

paper studies this leading case. We show, e.g., that there exists a simple and

empirically relevant set of sufficient statistics for the marginal cost of

public funds, namely unit tax and ad valorem pass-through and industry demand

elasticity. We then specialize our general setting to the case of price or

quantity competition and show how the marginal cost of public funds and the

pass-through are expressed using elasticities and curvatures of regular and

inverse demands. Based on the results of the leading case, the second part of

the paper presents a generalization with the tax revenue function specified as

a general function parameterized by a vector of multi-dimensional tax

parameters. We then argue that our results are carried over to the case of

heterogeneous firms and other extensions.

-

This paper studies models in which hypothesis tests have trivial power, that

is, power smaller than size. This testing impossibility, or impossibility type

A, arises when any alternative is not distinguishable from the null. We also

study settings in which it is impossible to have almost surely bounded

confidence sets for a parameter of interest. This second type of impossibility

(type B) occurs under a condition weaker than the condition for type A

impossibility: the parameter of interest must be nearly unidentified. Our

theoretical framework connects many existing publications on impossible

inference that rely on different notions of topologies to show models are not

distinguishable or nearly unidentified. We also derive both types of

impossibility using the weak topology induced by convergence in distribution.

Impossibility in the weak topology is often easier to prove, it is applicable

for many widely-used tests, and it is useful for robust hypothesis testing. We

conclude by demonstrating impossible inference in multiple economic

applications of models with discontinuity and time-series models.

-

We consider a general nonzero-sum impulse game with two players. The main

mathematical contribution of the paper is a verification theorem which

provides, under some regularity conditions, a suitable system of

quasi-variational inequalities for the value functions and the optimal

strategies of the two players. As an application, we study an impulse game with

a one-dimensional state variable, following a real-valued scaled Brownian

motion, and two players with linear and symmetric running payoffs. We fully

characterize a Nash equilibrium and provide explicit expressions for the

optimal strategies and the value functions. We also prove some asymptotic

results with respect to the intervention costs. Finally, we consider two

further non-symmetric examples where a Nash equilibrium is found numerically.

-

High dimensional vector autoregressive (VAR) models require a large number of

parameters to be estimated and may suffer of inferential problems. We propose a

new Bayesian nonparametric (BNP) Lasso prior (BNP-Lasso) for high-dimensional

VAR models that can improve estimation efficiency and prediction accuracy. Our

hierarchical prior overcomes overparametrization and overfitting issues by

clustering the VAR coefficients into groups and by shrinking the coefficients

of each group toward a common location. Clustering and shrinking effects

induced by the BNP-Lasso prior are well suited for the extraction of causal

networks from time series, since they account for some stylized facts in

real-world networks, which are sparsity, communities structures and

heterogeneity in the edges intensity. In order to fully capture the richness of

the data and to achieve a better understanding of financial and macroeconomic

risk, it is therefore crucial that the model used to extract network accounts

for these stylized facts.

-

We consider a two player simultaneous-move game where the two players each

select any permissible $n$-sided die for a fixed integer $n$. A player wins if

the outcome of his roll is greater than that of his opponent. Remarkably, for

$n>3$, there is a unique Nash Equilibrium in pure strategies. The unique Nash

Equilibrium is for each player to throw the Standard $n$-sided die, where each

side has a different number. Our proof of uniqueness is constructive. We

introduce an algorithm with which, for any nonstandard die, we may generate

another die that beats it.

-

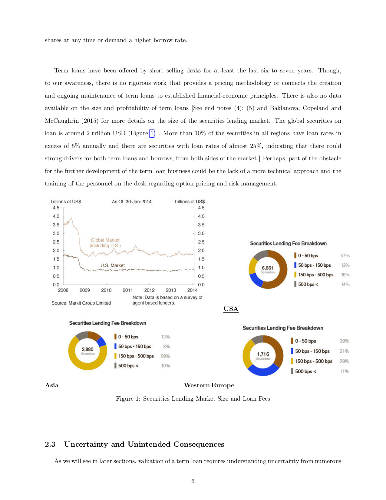

We develop models to price long term loans in the securities lending

business. These longer horizon deals can be viewed as contracts with

optionality embedded in them and can be priced using established methods from

derivatives theory, becoming to our limited knowledge, the first application

that can lead to greater synergies between the operations of derivative and

delta-one trading desks, perhaps even being able to combine certain aspects of

the day to day operations of these seemingly disparate entities. We run

numerical simulations to demonstrate the practical applicability of these

models. These models are part of one of the least explored yet profit laden

areas of modern investment management.

We develop a heuristic that can mitigate the loss of information that sets in

when parameters are estimated first and then the valuation is performed by

directly calculating the valuation using the historical time series. This can

lead to reduced models errors and greater financial stability. We illustrate

how the methodologies developed here could be useful for inventory management.

All these techniques could have applications for dealing with other financial

instruments, non-financial commodities and many forms of uncertainty. An

unintended consequence of our efforts, has become a review of the vast

literature on options pricing, which can be useful for anyone that attempts to

apply the corresponding techniques to the problems mentioned here.

Admittedly, our initial ambitions to produce a normative theory on long term

loan valuations are undone by the present state of affairs in social science

modeling. Though we consider many elements of a securities lending system at

face value, this cannot be termed a positive theory. For now, if it ends up

producing a useful theory, our work is done.

-

We represent the functioning of the housing market and study the relation

between income segregation, income inequality and house prices by introducing a

spatial Agent-Based Model (ABM). Differently from traditional models in urban

economics, we explicitly specify the behavior of buyers and sellers and the

price formation mechanism. Buyers who differ by income select among

heterogeneous neighborhoods using a probabilistic model of residential choice;

sellers employ an aspiration level heuristic to set their reservation offer

price; prices are determined through a continuous double auction. We first

provide an approximate analytical solution of the ABM, shedding light on the

structure of the model and on the effect of the parameters. We then simulate

the ABM and find that: (i) a more unequal income distribution lowers the prices

globally, but implies stronger segregation; (ii) a spike of the demand in one

part of the city increases the prices all over the city; (iii) subsidies are

more efficient than taxes in fostering social mixing.

-

Almost by definition, radical innovations create a need to revise existing

classification systems. In this paper, we argue that classification system

changes and patent reclassification are common and reveal interesting

information about technological evolution. To support our argument, we present

three sets of findings regarding classification volatility in the U.S. patent

classification system. First, we study the evolution of the number of distinct

classes. Reconstructed time series based on the current classification scheme

are very different from historical data. This suggests that using the current

classification to analyze the past produces a distorted view of the evolution

of the system. Second, we study the relative sizes of classes. The size

distribution is exponential so classes are of quite different sizes, but the

largest classes are not necessarily the oldest. To explain this pattern with a

simple stochastic growth model, we introduce the assumption that classes have a

regular chance to be split. Third, we study reclassification. The share of

patents that are in a different class now than they were at birth can be quite

high. Reclassification mostly occurs across classes belonging to the same

1-digit NBER category, but not always. We also document that reclassified

patents tend to be more cited than non-reclassified ones, even after

controlling for grant year and class of origin.

-

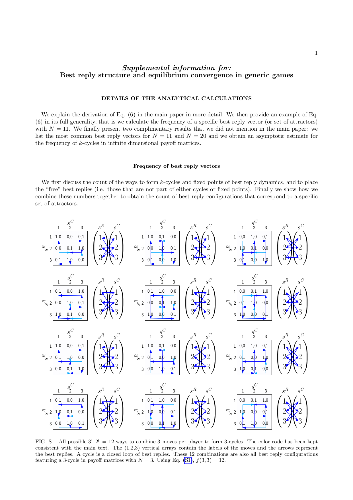

Game theory is widely used as a behavioral model for strategic interactions

in biology and social science. It is common practice to assume that players

quickly converge to an equilibrium, e.g. a Nash equilibrium. This can be

studied in terms of best reply dynamics, in which each player myopically uses

the best response to her opponent's last move. Existing research shows that

convergence can be problematic when there are best reply cycles. Here we

calculate how typical this is by studying the space of all possible two-player

normal form games and counting the frequency of best reply cycles. The two key

parameters are the number of moves, which defines how complicated the game is,

and the anti-correlation of the payoffs, which determines how competitive it

is. We find that as games get more complicated and more competitive, best reply

cycles become dominant. The existence of best reply cycles predicts

non-convergence of six different learning algorithms that have support from

human experiments. Our results imply that for complicated and competitive games

equilibrium is typically an unrealistic assumption. Alternatively, if for some

reason "real" games are special and do not possess cycles, we raise the

interesting question of why this should be so.

-

We used to marry people to whom we were somehow connected. Since we were more

connected to people similar to us, we were also likely to marry someone from

our own race. However, online dating has changed this pattern; people who meet

online tend to be complete strangers. We investigate the effects of those

previously absent ties on the diversity of modern societies.

We find that social integration occurs rapidly when a society benefits from

new connections. Our analysis of state-level data on interracial marriage and

broadband adoption (proxy for online dating) suggests that this integration

process is significant and ongoing.

-

Indirect inference requires simulating realisations of endogenous variables

from the model under study. When the endogenous variables are discontinuous

functions of the model parameters, the resulting indirect inference criterion

function is discontinuous and does not permit the use of derivative-based

optimisation routines. Using a change of variables technique, we propose a

novel simulation algorithm that alleviates the discontinuities inherent in such

indirect inference criterion functions, and permits the application of

derivative-based optimisation routines to estimate the unknown model

parameters. Unlike competing approaches, this approach does not rely on kernel

smoothing or bandwidth parameters. Several Monte Carlo examples that have

featured in the literature on indirect inference with discontinuous outcomes

illustrate the approach, and demonstrate the superior performance of this

approach over existing alternatives.

-

We consider how to optimally allocate investments in a portfolio of competing

technologies using the standard mean-variance framework of portfolio theory. We

assume that technologies follow the empirically observed relationship known as

Wright's law, also called a "learning curve" or "experience curve", which

postulates that costs drop as cumulative production increases. This introduces

a positive feedback between cost and investment that complicates the portfolio

problem, leading to multiple local optima, and causing a trade-off between

concentrating investments in one project to spur rapid progress vs.

diversifying over many projects to hedge against failure. We study the

two-technology case and characterize the optimal diversification in terms of

progress rates, variability, initial costs, initial experience, risk aversion,

discount rate and total demand. The efficient frontier framework is used to

visualize technology portfolios and show how feedback results in nonlinear

distortions of the feasible set. For the two-period case, in which learning and

uncertainty interact with discounting, we compare different scenarios and find

that the discount rate plays a critical role.

-

We provide a framework for determining the centralities of agents in a broad

family of random networks. Current understanding of network centrality is

largely restricted to deterministic settings, but practitioners frequently use

random network models to accommodate data limitations or prove asymptotic

results. Our main theorems show that on large random networks, centrality

measures are close to their expected values with high probability. We

illustrate the economic consequences of these results by presenting three

applications: (1) In network formation models based on community structure

(called stochastic block models), we show network segregation and differences

in community size produce inequality. Benefits from peer effects tend to accrue

disproportionately to bigger and better-connected communities. (2) When link

probabilities depend on geography, we can compute and compare the centralities

of agents in different locations. (3) In models where connections depend on

several independent characteristics, we give a formula that determines

centralities 'characteristic-by-characteristic'. The basic techniques from

these applications, which use the main theorems to reduce questions about

random networks to deterministic calculations, extend to many network games.

-

We present functional forms allowing a broader range of analytic solutions to

common economic equilibrium problems. These can increase the realism of

pen-and-paper solutions or speed large-scale numerical solutions as

computational subroutines. We use the latter approach to build a tractable

heterogeneous firm model of international trade accommodating economies of

scale in export and diseconomies of scale in production, providing a natural,

unified solution to several puzzles concerning trade costs. We briefly

highlight applications in a range of other fields. Our method of generating

analytic solutions is a discrete approximation to a logarithmically modified

Laplace transform of equilibrium conditions.

-

The range of a payoff function for an $n$-player finite strategic game is

investigated using a novel approach, the notion of extreme points of a

non-convex set. The shape of a noncooperative payoff region can be estimated

using extreme points and supporting hyperplanes of the cooperative payoff

region. A basic structural characteristic of a noncooperative payoff region is

that any of its subregions must be non-strictly convex if the subregion

contains a relative neighborhood of a point on its boundary. Besides, applying

the properties of extreme points of a noncooperative payoff region is a simple

and effective way to prove some results about Pareto efficiency and social

efficiency in game theory.

We model learning in a continuous-time Brownian setting where there is prior ambiguity. The associated model of preference values robustness and is time-consistent. It is applied to study optimal learning when the choice between actions can be postponed, at a per-unit-time cost, in order to observe a signal that provides information about an unknown parameter. The corresponding optimal stopping problem is solved in closed-form, with a focus on two specific settings: Ellsberg's two-urn thought experiment expanded to allow learning before the choice of bets, and a robust version of the classical problem of sequential testing of two simple hypotheses about the unknown drift of a Wiener process. In both cases, the link between robustness and the demand for learning is studied.

We model learning in a continuous-time Brownian setting where there is prior ambiguity. The associated model of preference values robustness and is time-consistent. It is applied to study optimal learning when the choice between actions can be postponed, at a per-unit-time cost, in order to observe a signal that provides information about an unknown parameter. The corresponding optimal stopping problem is solved in closed-form, with a focus on two specific settings: Ellsberg's two-urn thought experiment expanded to allow learning before the choice of bets, and a robust version of the classical problem of sequential testing of two simple hypotheses about the unknown drift of a Wiener process. In both cases, the link between robustness and the demand for learning is studied.

We study decentralized protection strategies against Susceptible-Infected-Susceptible (SIS) epidemics on networks. We consider a population game framework where nodes choose whether or not to vaccinate themselves, and the epidemic risk is defined as the infection probability at the endemic state of the epidemic under a degree-based mean-field approximation. Motivated by studies in behavioral economics showing that humans perceive probabilities and risks in a nonlinear fashion, we specifically examine the impacts of such misperceptions on the Nash equilibrium protection strategies. We first establish the existence and uniqueness of a threshold equilibrium where nodes with degrees larger than a certain threshold vaccinate. When the vaccination cost is sufficiently high, we show that behavioral biases cause fewer players to vaccinate, and vice versa. We quantify this effect for a class of networks with power-law degree distributions by proving tight bounds on the ratio of equilibrium thresholds under behavioral and true perceptions of probabilities. We further characterize the socially optimal vaccination policy and investigate the inefficiency of Nash equilibrium.

We study decentralized protection strategies against Susceptible-Infected-Susceptible (SIS) epidemics on networks. We consider a population game framework where nodes choose whether or not to vaccinate themselves, and the epidemic risk is defined as the infection probability at the endemic state of the epidemic under a degree-based mean-field approximation. Motivated by studies in behavioral economics showing that humans perceive probabilities and risks in a nonlinear fashion, we specifically examine the impacts of such misperceptions on the Nash equilibrium protection strategies. We first establish the existence and uniqueness of a threshold equilibrium where nodes with degrees larger than a certain threshold vaccinate. When the vaccination cost is sufficiently high, we show that behavioral biases cause fewer players to vaccinate, and vice versa. We quantify this effect for a class of networks with power-law degree distributions by proving tight bounds on the ratio of equilibrium thresholds under behavioral and true perceptions of probabilities. We further characterize the socially optimal vaccination policy and investigate the inefficiency of Nash equilibrium.

How do macro-financial shocks affect investor behavior and market dynamics? Recent evidence on experience effects suggests a long-lasting influence of personally experienced outcomes on investor beliefs and investment, but also significant differences across older and younger generations. We formalize experience-based learning in an OLG model, where different cross-cohort experiences generate persistent heterogeneity in beliefs, portfolio choices, and trade. The model allows us to characterize a novel link between investor demographics and the dependence of prices on past dividends, while also generating known features of asset prices, such as excess volatility and return predictability. The model produces new implications for the cross-section of asset holdings, trade volume, and investors' heterogenous responses to recent financial crises, which we show to be in line with the data.

How do macro-financial shocks affect investor behavior and market dynamics? Recent evidence on experience effects suggests a long-lasting influence of personally experienced outcomes on investor beliefs and investment, but also significant differences across older and younger generations. We formalize experience-based learning in an OLG model, where different cross-cohort experiences generate persistent heterogeneity in beliefs, portfolio choices, and trade. The model allows us to characterize a novel link between investor demographics and the dependence of prices on past dividends, while also generating known features of asset prices, such as excess volatility and return predictability. The model produces new implications for the cross-section of asset holdings, trade volume, and investors' heterogenous responses to recent financial crises, which we show to be in line with the data.

We reconsider the microeconomic foundations of financial economics. Motivated by the importance of Knightian Uncertainty in markets, we present a model that does not carry any probabilistic structure ex ante, yet is based on a common order. We derive the fundamental equivalence of economic viability of asset prices and absence of arbitrage. We also obtain a modified version of the Fundamental Theorem of Asset Pricing using the notion of sublinear pricing measures. Different versions of the Efficient Market Hypothesis are related to the assumptions one is willing to impose on the common order.

We reconsider the microeconomic foundations of financial economics. Motivated by the importance of Knightian Uncertainty in markets, we present a model that does not carry any probabilistic structure ex ante, yet is based on a common order. We derive the fundamental equivalence of economic viability of asset prices and absence of arbitrage. We also obtain a modified version of the Fundamental Theorem of Asset Pricing using the notion of sublinear pricing measures. Different versions of the Efficient Market Hypothesis are related to the assumptions one is willing to impose on the common order.

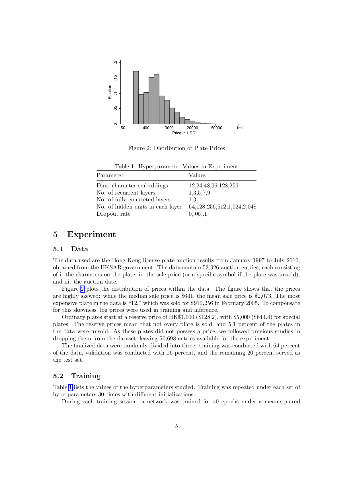

In Chinese societies, superstition is of paramount importance, and vehicle license plates with desirable numbers can fetch very high prices in auctions. Unlike other valuable items, license plates are not allocated an estimated price before auction. I propose that the task of predicting plate prices can be viewed as a natural language processing (NLP) task, as the value depends on the meaning of each individual character on the plate and its semantics. I construct a deep recurrent neural network (RNN) to predict the prices of vehicle license plates in Hong Kong, based on the characters on a plate. I demonstrate the importance of having a deep network and of retraining. Evaluated on 13 years of historical auction prices, the deep RNN's predictions can explain over 80 percent of price variations, outperforming previous models by a significant margin. I also demonstrate how the model can be extended to become a search engine for plates and to provide estimates of the expected price distribution.

In Chinese societies, superstition is of paramount importance, and vehicle license plates with desirable numbers can fetch very high prices in auctions. Unlike other valuable items, license plates are not allocated an estimated price before auction. I propose that the task of predicting plate prices can be viewed as a natural language processing (NLP) task, as the value depends on the meaning of each individual character on the plate and its semantics. I construct a deep recurrent neural network (RNN) to predict the prices of vehicle license plates in Hong Kong, based on the characters on a plate. I demonstrate the importance of having a deep network and of retraining. Evaluated on 13 years of historical auction prices, the deep RNN's predictions can explain over 80 percent of price variations, outperforming previous models by a significant margin. I also demonstrate how the model can be extended to become a search engine for plates and to provide estimates of the expected price distribution.

The structure of the International Trade Network (ITN), whose nodes and links represent world countries and their trade relations respectively, affects key economic processes worldwide, including globalization, economic integration, industrial production, and the propagation of shocks and instabilities. Characterizing the ITN via a simple yet accurate model is an open problem. The traditional Gravity Model (GM) successfully reproduces the volume of trade between connected countries, using macroeconomic properties such as GDP, geographic distance, and possibly other factors. However, it predicts a network with complete or homogeneous topology, thus failing to reproduce the highly heterogeneous structure of the ITN. On the other hand, recent maximum-entropy network models successfully reproduce the complex topology of the ITN, but provide no information about trade volumes. Here we integrate these two currently incompatible approaches via the introduction of an Enhanced Gravity Model (EGM) of trade. The EGM is the simplest model combining the GM with the network approach within a maximum-entropy framework. Via a unified and principled mechanism that is transparent enough to be generalized to any economic network, the EGM provides a new econometric framework wherein trade probabilities and trade volumes can be separately controlled by any combination of dyadic and country-specific macroeconomic variables. The model successfully reproduces both the global topology and the local link weights of the ITN, parsimoniously reconciling the conflicting approaches. It also indicates that the probability that any two countries trade a certain volume should follow a geometric or exponential distribution with an additional point mass at zero volume.

The structure of the International Trade Network (ITN), whose nodes and links represent world countries and their trade relations respectively, affects key economic processes worldwide, including globalization, economic integration, industrial production, and the propagation of shocks and instabilities. Characterizing the ITN via a simple yet accurate model is an open problem. The traditional Gravity Model (GM) successfully reproduces the volume of trade between connected countries, using macroeconomic properties such as GDP, geographic distance, and possibly other factors. However, it predicts a network with complete or homogeneous topology, thus failing to reproduce the highly heterogeneous structure of the ITN. On the other hand, recent maximum-entropy network models successfully reproduce the complex topology of the ITN, but provide no information about trade volumes. Here we integrate these two currently incompatible approaches via the introduction of an Enhanced Gravity Model (EGM) of trade. The EGM is the simplest model combining the GM with the network approach within a maximum-entropy framework. Via a unified and principled mechanism that is transparent enough to be generalized to any economic network, the EGM provides a new econometric framework wherein trade probabilities and trade volumes can be separately controlled by any combination of dyadic and country-specific macroeconomic variables. The model successfully reproduces both the global topology and the local link weights of the ITN, parsimoniously reconciling the conflicting approaches. It also indicates that the probability that any two countries trade a certain volume should follow a geometric or exponential distribution with an additional point mass at zero volume.

In this paper, we extend the optimal securitisation model of Pag\`es [50] and Possama\"i and Pag\`es [51] between an investor and a bank to a setting allowing both moral hazard and adverse selection. Following the recent approach to these problems of Cvitani\'c, Wan and Yang [14], we characterise explicitly and rigorously the so-called credible set of the continuation and temptation values of the bank, and obtain the value function of the investor as well as the optimal contracts through a recursive system of first-order variational inequalities with gradient constraints. We provide a detailed discussion of the properties of the optimal menu of contracts.

In this paper, we extend the optimal securitisation model of Pag\`es [50] and Possama\"i and Pag\`es [51] between an investor and a bank to a setting allowing both moral hazard and adverse selection. Following the recent approach to these problems of Cvitani\'c, Wan and Yang [14], we characterise explicitly and rigorously the so-called credible set of the continuation and temptation values of the bank, and obtain the value function of the investor as well as the optimal contracts through a recursive system of first-order variational inequalities with gradient constraints. We provide a detailed discussion of the properties of the optimal menu of contracts.

In this paper, we introduce quantile coherency to measure general dependence structures emerging in the joint distribution in the frequency domain and argue that this type of dependence is natural for economic time series but remains invisible when only the traditional analysis is employed. We define estimators which capture the general dependence structure, provide a detailed analysis of their asymptotic properties and discuss how to conduct inference for a general class of possibly nonlinear processes. In an empirical illustration we examine the dependence of bivariate stock market returns and shed new light on measurement of tail risk in financial markets. We also provide a modelling exercise to illustrate how applied researchers can benefit from using quantile coherency when assessing time series models.

In this paper, we introduce quantile coherency to measure general dependence structures emerging in the joint distribution in the frequency domain and argue that this type of dependence is natural for economic time series but remains invisible when only the traditional analysis is employed. We define estimators which capture the general dependence structure, provide a detailed analysis of their asymptotic properties and discuss how to conduct inference for a general class of possibly nonlinear processes. In an empirical illustration we examine the dependence of bivariate stock market returns and shed new light on measurement of tail risk in financial markets. We also provide a modelling exercise to illustrate how applied researchers can benefit from using quantile coherency when assessing time series models.

A set of data with positive values follows a Pareto distribution if the log-log plot of value versus rank is approximately a straight line. A Pareto distribution satisfies Zipf's law if the log-log plot has a slope of -1. Since many types of ranked data follow Zipf's law, it is considered a form of universality. We propose a mathematical explanation for this phenomenon based on Atlas models and first-order models, systems of positive continuous semimartingales with parameters that depend only on rank. We show that the stable distribution of an Atlas model will follow Zipf's law if and only if two natural conditions, conservation and completeness, are satisfied. Since Atlas models and first-order models can be constructed to approximate systems of time-dependent rank-based data, our results can explain the universality of Zipf's law for such systems. However, ranked data generated by other means may follow non-Zipfian Pareto distributions. Hence, our results explain why Zipf's law holds for word frequency, firm size, household wealth, and city size, while it does not hold for earthquake magnitude, cumulative book sales, the intensity of solar flares, and the intensity of wars, all of which follow non-Zipfian Pareto distributions.

A set of data with positive values follows a Pareto distribution if the log-log plot of value versus rank is approximately a straight line. A Pareto distribution satisfies Zipf's law if the log-log plot has a slope of -1. Since many types of ranked data follow Zipf's law, it is considered a form of universality. We propose a mathematical explanation for this phenomenon based on Atlas models and first-order models, systems of positive continuous semimartingales with parameters that depend only on rank. We show that the stable distribution of an Atlas model will follow Zipf's law if and only if two natural conditions, conservation and completeness, are satisfied. Since Atlas models and first-order models can be constructed to approximate systems of time-dependent rank-based data, our results can explain the universality of Zipf's law for such systems. However, ranked data generated by other means may follow non-Zipfian Pareto distributions. Hence, our results explain why Zipf's law holds for word frequency, firm size, household wealth, and city size, while it does not hold for earthquake magnitude, cumulative book sales, the intensity of solar flares, and the intensity of wars, all of which follow non-Zipfian Pareto distributions.

This paper provides a comprehensive analysis of welfare measures when oligopolistic firms face multiple policy interventions and external changes under general forms of market demands, production costs, and imperfect competition. We present our results in terms of two welfare measures, namely, marginal cost of public funds and incidence, in relation to multi-dimensional pass-through. Our arguments are best understood with two-dimensional taxation where homogeneous firms face unit and ad valorem taxes. The first part of the paper studies this leading case. We show, e.g., that there exists a simple and empirically relevant set of sufficient statistics for the marginal cost of public funds, namely unit tax and ad valorem pass-through and industry demand elasticity. We then specialize our general setting to the case of price or quantity competition and show how the marginal cost of public funds and the pass-through are expressed using elasticities and curvatures of regular and inverse demands. Based on the results of the leading case, the second part of the paper presents a generalization with the tax revenue function specified as a general function parameterized by a vector of multi-dimensional tax parameters. We then argue that our results are carried over to the case of heterogeneous firms and other extensions.

This paper provides a comprehensive analysis of welfare measures when oligopolistic firms face multiple policy interventions and external changes under general forms of market demands, production costs, and imperfect competition. We present our results in terms of two welfare measures, namely, marginal cost of public funds and incidence, in relation to multi-dimensional pass-through. Our arguments are best understood with two-dimensional taxation where homogeneous firms face unit and ad valorem taxes. The first part of the paper studies this leading case. We show, e.g., that there exists a simple and empirically relevant set of sufficient statistics for the marginal cost of public funds, namely unit tax and ad valorem pass-through and industry demand elasticity. We then specialize our general setting to the case of price or quantity competition and show how the marginal cost of public funds and the pass-through are expressed using elasticities and curvatures of regular and inverse demands. Based on the results of the leading case, the second part of the paper presents a generalization with the tax revenue function specified as a general function parameterized by a vector of multi-dimensional tax parameters. We then argue that our results are carried over to the case of heterogeneous firms and other extensions.

This paper studies models in which hypothesis tests have trivial power, that is, power smaller than size. This testing impossibility, or impossibility type A, arises when any alternative is not distinguishable from the null. We also study settings in which it is impossible to have almost surely bounded confidence sets for a parameter of interest. This second type of impossibility (type B) occurs under a condition weaker than the condition for type A impossibility: the parameter of interest must be nearly unidentified. Our theoretical framework connects many existing publications on impossible inference that rely on different notions of topologies to show models are not distinguishable or nearly unidentified. We also derive both types of impossibility using the weak topology induced by convergence in distribution. Impossibility in the weak topology is often easier to prove, it is applicable for many widely-used tests, and it is useful for robust hypothesis testing. We conclude by demonstrating impossible inference in multiple economic applications of models with discontinuity and time-series models.

This paper studies models in which hypothesis tests have trivial power, that is, power smaller than size. This testing impossibility, or impossibility type A, arises when any alternative is not distinguishable from the null. We also study settings in which it is impossible to have almost surely bounded confidence sets for a parameter of interest. This second type of impossibility (type B) occurs under a condition weaker than the condition for type A impossibility: the parameter of interest must be nearly unidentified. Our theoretical framework connects many existing publications on impossible inference that rely on different notions of topologies to show models are not distinguishable or nearly unidentified. We also derive both types of impossibility using the weak topology induced by convergence in distribution. Impossibility in the weak topology is often easier to prove, it is applicable for many widely-used tests, and it is useful for robust hypothesis testing. We conclude by demonstrating impossible inference in multiple economic applications of models with discontinuity and time-series models.

We consider a general nonzero-sum impulse game with two players. The main mathematical contribution of the paper is a verification theorem which provides, under some regularity conditions, a suitable system of quasi-variational inequalities for the value functions and the optimal strategies of the two players. As an application, we study an impulse game with a one-dimensional state variable, following a real-valued scaled Brownian motion, and two players with linear and symmetric running payoffs. We fully characterize a Nash equilibrium and provide explicit expressions for the optimal strategies and the value functions. We also prove some asymptotic results with respect to the intervention costs. Finally, we consider two further non-symmetric examples where a Nash equilibrium is found numerically.

We consider a general nonzero-sum impulse game with two players. The main mathematical contribution of the paper is a verification theorem which provides, under some regularity conditions, a suitable system of quasi-variational inequalities for the value functions and the optimal strategies of the two players. As an application, we study an impulse game with a one-dimensional state variable, following a real-valued scaled Brownian motion, and two players with linear and symmetric running payoffs. We fully characterize a Nash equilibrium and provide explicit expressions for the optimal strategies and the value functions. We also prove some asymptotic results with respect to the intervention costs. Finally, we consider two further non-symmetric examples where a Nash equilibrium is found numerically.

We consider a two player simultaneous-move game where the two players each select any permissible $n$-sided die for a fixed integer $n$. A player wins if the outcome of his roll is greater than that of his opponent. Remarkably, for $n>3$, there is a unique Nash Equilibrium in pure strategies. The unique Nash Equilibrium is for each player to throw the Standard $n$-sided die, where each side has a different number. Our proof of uniqueness is constructive. We introduce an algorithm with which, for any nonstandard die, we may generate another die that beats it.

We consider a two player simultaneous-move game where the two players each select any permissible $n$-sided die for a fixed integer $n$. A player wins if the outcome of his roll is greater than that of his opponent. Remarkably, for $n>3$, there is a unique Nash Equilibrium in pure strategies. The unique Nash Equilibrium is for each player to throw the Standard $n$-sided die, where each side has a different number. Our proof of uniqueness is constructive. We introduce an algorithm with which, for any nonstandard die, we may generate another die that beats it.

We develop models to price long term loans in the securities lending business. These longer horizon deals can be viewed as contracts with optionality embedded in them and can be priced using established methods from derivatives theory, becoming to our limited knowledge, the first application that can lead to greater synergies between the operations of derivative and delta-one trading desks, perhaps even being able to combine certain aspects of the day to day operations of these seemingly disparate entities. We run numerical simulations to demonstrate the practical applicability of these models. These models are part of one of the least explored yet profit laden areas of modern investment management. We develop a heuristic that can mitigate the loss of information that sets in when parameters are estimated first and then the valuation is performed by directly calculating the valuation using the historical time series. This can lead to reduced models errors and greater financial stability. We illustrate how the methodologies developed here could be useful for inventory management. All these techniques could have applications for dealing with other financial instruments, non-financial commodities and many forms of uncertainty. An unintended consequence of our efforts, has become a review of the vast literature on options pricing, which can be useful for anyone that attempts to apply the corresponding techniques to the problems mentioned here. Admittedly, our initial ambitions to produce a normative theory on long term loan valuations are undone by the present state of affairs in social science modeling. Though we consider many elements of a securities lending system at face value, this cannot be termed a positive theory. For now, if it ends up producing a useful theory, our work is done.

We develop models to price long term loans in the securities lending business. These longer horizon deals can be viewed as contracts with optionality embedded in them and can be priced using established methods from derivatives theory, becoming to our limited knowledge, the first application that can lead to greater synergies between the operations of derivative and delta-one trading desks, perhaps even being able to combine certain aspects of the day to day operations of these seemingly disparate entities. We run numerical simulations to demonstrate the practical applicability of these models. These models are part of one of the least explored yet profit laden areas of modern investment management. We develop a heuristic that can mitigate the loss of information that sets in when parameters are estimated first and then the valuation is performed by directly calculating the valuation using the historical time series. This can lead to reduced models errors and greater financial stability. We illustrate how the methodologies developed here could be useful for inventory management. All these techniques could have applications for dealing with other financial instruments, non-financial commodities and many forms of uncertainty. An unintended consequence of our efforts, has become a review of the vast literature on options pricing, which can be useful for anyone that attempts to apply the corresponding techniques to the problems mentioned here. Admittedly, our initial ambitions to produce a normative theory on long term loan valuations are undone by the present state of affairs in social science modeling. Though we consider many elements of a securities lending system at face value, this cannot be termed a positive theory. For now, if it ends up producing a useful theory, our work is done.

We represent the functioning of the housing market and study the relation between income segregation, income inequality and house prices by introducing a spatial Agent-Based Model (ABM). Differently from traditional models in urban economics, we explicitly specify the behavior of buyers and sellers and the price formation mechanism. Buyers who differ by income select among heterogeneous neighborhoods using a probabilistic model of residential choice; sellers employ an aspiration level heuristic to set their reservation offer price; prices are determined through a continuous double auction. We first provide an approximate analytical solution of the ABM, shedding light on the structure of the model and on the effect of the parameters. We then simulate the ABM and find that: (i) a more unequal income distribution lowers the prices globally, but implies stronger segregation; (ii) a spike of the demand in one part of the city increases the prices all over the city; (iii) subsidies are more efficient than taxes in fostering social mixing.

We represent the functioning of the housing market and study the relation between income segregation, income inequality and house prices by introducing a spatial Agent-Based Model (ABM). Differently from traditional models in urban economics, we explicitly specify the behavior of buyers and sellers and the price formation mechanism. Buyers who differ by income select among heterogeneous neighborhoods using a probabilistic model of residential choice; sellers employ an aspiration level heuristic to set their reservation offer price; prices are determined through a continuous double auction. We first provide an approximate analytical solution of the ABM, shedding light on the structure of the model and on the effect of the parameters. We then simulate the ABM and find that: (i) a more unequal income distribution lowers the prices globally, but implies stronger segregation; (ii) a spike of the demand in one part of the city increases the prices all over the city; (iii) subsidies are more efficient than taxes in fostering social mixing.

Almost by definition, radical innovations create a need to revise existing classification systems. In this paper, we argue that classification system changes and patent reclassification are common and reveal interesting information about technological evolution. To support our argument, we present three sets of findings regarding classification volatility in the U.S. patent classification system. First, we study the evolution of the number of distinct classes. Reconstructed time series based on the current classification scheme are very different from historical data. This suggests that using the current classification to analyze the past produces a distorted view of the evolution of the system. Second, we study the relative sizes of classes. The size distribution is exponential so classes are of quite different sizes, but the largest classes are not necessarily the oldest. To explain this pattern with a simple stochastic growth model, we introduce the assumption that classes have a regular chance to be split. Third, we study reclassification. The share of patents that are in a different class now than they were at birth can be quite high. Reclassification mostly occurs across classes belonging to the same 1-digit NBER category, but not always. We also document that reclassified patents tend to be more cited than non-reclassified ones, even after controlling for grant year and class of origin.

Almost by definition, radical innovations create a need to revise existing classification systems. In this paper, we argue that classification system changes and patent reclassification are common and reveal interesting information about technological evolution. To support our argument, we present three sets of findings regarding classification volatility in the U.S. patent classification system. First, we study the evolution of the number of distinct classes. Reconstructed time series based on the current classification scheme are very different from historical data. This suggests that using the current classification to analyze the past produces a distorted view of the evolution of the system. Second, we study the relative sizes of classes. The size distribution is exponential so classes are of quite different sizes, but the largest classes are not necessarily the oldest. To explain this pattern with a simple stochastic growth model, we introduce the assumption that classes have a regular chance to be split. Third, we study reclassification. The share of patents that are in a different class now than they were at birth can be quite high. Reclassification mostly occurs across classes belonging to the same 1-digit NBER category, but not always. We also document that reclassified patents tend to be more cited than non-reclassified ones, even after controlling for grant year and class of origin.

Game theory is widely used as a behavioral model for strategic interactions in biology and social science. It is common practice to assume that players quickly converge to an equilibrium, e.g. a Nash equilibrium. This can be studied in terms of best reply dynamics, in which each player myopically uses the best response to her opponent's last move. Existing research shows that convergence can be problematic when there are best reply cycles. Here we calculate how typical this is by studying the space of all possible two-player normal form games and counting the frequency of best reply cycles. The two key parameters are the number of moves, which defines how complicated the game is, and the anti-correlation of the payoffs, which determines how competitive it is. We find that as games get more complicated and more competitive, best reply cycles become dominant. The existence of best reply cycles predicts non-convergence of six different learning algorithms that have support from human experiments. Our results imply that for complicated and competitive games equilibrium is typically an unrealistic assumption. Alternatively, if for some reason "real" games are special and do not possess cycles, we raise the interesting question of why this should be so.

Game theory is widely used as a behavioral model for strategic interactions in biology and social science. It is common practice to assume that players quickly converge to an equilibrium, e.g. a Nash equilibrium. This can be studied in terms of best reply dynamics, in which each player myopically uses the best response to her opponent's last move. Existing research shows that convergence can be problematic when there are best reply cycles. Here we calculate how typical this is by studying the space of all possible two-player normal form games and counting the frequency of best reply cycles. The two key parameters are the number of moves, which defines how complicated the game is, and the anti-correlation of the payoffs, which determines how competitive it is. We find that as games get more complicated and more competitive, best reply cycles become dominant. The existence of best reply cycles predicts non-convergence of six different learning algorithms that have support from human experiments. Our results imply that for complicated and competitive games equilibrium is typically an unrealistic assumption. Alternatively, if for some reason "real" games are special and do not possess cycles, we raise the interesting question of why this should be so.

Indirect inference requires simulating realisations of endogenous variables from the model under study. When the endogenous variables are discontinuous functions of the model parameters, the resulting indirect inference criterion function is discontinuous and does not permit the use of derivative-based optimisation routines. Using a change of variables technique, we propose a novel simulation algorithm that alleviates the discontinuities inherent in such indirect inference criterion functions, and permits the application of derivative-based optimisation routines to estimate the unknown model parameters. Unlike competing approaches, this approach does not rely on kernel smoothing or bandwidth parameters. Several Monte Carlo examples that have featured in the literature on indirect inference with discontinuous outcomes illustrate the approach, and demonstrate the superior performance of this approach over existing alternatives.

Indirect inference requires simulating realisations of endogenous variables from the model under study. When the endogenous variables are discontinuous functions of the model parameters, the resulting indirect inference criterion function is discontinuous and does not permit the use of derivative-based optimisation routines. Using a change of variables technique, we propose a novel simulation algorithm that alleviates the discontinuities inherent in such indirect inference criterion functions, and permits the application of derivative-based optimisation routines to estimate the unknown model parameters. Unlike competing approaches, this approach does not rely on kernel smoothing or bandwidth parameters. Several Monte Carlo examples that have featured in the literature on indirect inference with discontinuous outcomes illustrate the approach, and demonstrate the superior performance of this approach over existing alternatives.

We consider how to optimally allocate investments in a portfolio of competing technologies using the standard mean-variance framework of portfolio theory. We assume that technologies follow the empirically observed relationship known as Wright's law, also called a "learning curve" or "experience curve", which postulates that costs drop as cumulative production increases. This introduces a positive feedback between cost and investment that complicates the portfolio problem, leading to multiple local optima, and causing a trade-off between concentrating investments in one project to spur rapid progress vs. diversifying over many projects to hedge against failure. We study the two-technology case and characterize the optimal diversification in terms of progress rates, variability, initial costs, initial experience, risk aversion, discount rate and total demand. The efficient frontier framework is used to visualize technology portfolios and show how feedback results in nonlinear distortions of the feasible set. For the two-period case, in which learning and uncertainty interact with discounting, we compare different scenarios and find that the discount rate plays a critical role.

We consider how to optimally allocate investments in a portfolio of competing technologies using the standard mean-variance framework of portfolio theory. We assume that technologies follow the empirically observed relationship known as Wright's law, also called a "learning curve" or "experience curve", which postulates that costs drop as cumulative production increases. This introduces a positive feedback between cost and investment that complicates the portfolio problem, leading to multiple local optima, and causing a trade-off between concentrating investments in one project to spur rapid progress vs. diversifying over many projects to hedge against failure. We study the two-technology case and characterize the optimal diversification in terms of progress rates, variability, initial costs, initial experience, risk aversion, discount rate and total demand. The efficient frontier framework is used to visualize technology portfolios and show how feedback results in nonlinear distortions of the feasible set. For the two-period case, in which learning and uncertainty interact with discounting, we compare different scenarios and find that the discount rate plays a critical role.

The range of a payoff function for an $n$-player finite strategic game is investigated using a novel approach, the notion of extreme points of a non-convex set. The shape of a noncooperative payoff region can be estimated using extreme points and supporting hyperplanes of the cooperative payoff region. A basic structural characteristic of a noncooperative payoff region is that any of its subregions must be non-strictly convex if the subregion contains a relative neighborhood of a point on its boundary. Besides, applying the properties of extreme points of a noncooperative payoff region is a simple and effective way to prove some results about Pareto efficiency and social efficiency in game theory.

The range of a payoff function for an $n$-player finite strategic game is investigated using a novel approach, the notion of extreme points of a non-convex set. The shape of a noncooperative payoff region can be estimated using extreme points and supporting hyperplanes of the cooperative payoff region. A basic structural characteristic of a noncooperative payoff region is that any of its subregions must be non-strictly convex if the subregion contains a relative neighborhood of a point on its boundary. Besides, applying the properties of extreme points of a noncooperative payoff region is a simple and effective way to prove some results about Pareto efficiency and social efficiency in game theory.