-

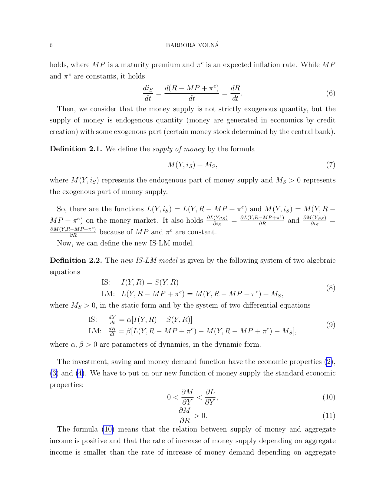

In this paper, we present own point of view how the unexpected fluctuations

of the long-term real interest rate can be explained. We describe a

macroeconomic environment by the modification of the fundamental macroeconomic

equilibrium model called the IS-LM model. Last but not least, we suggest a

possible cooperation between the fiscal and monetary policy to reduce these

fluctuations. Our modelling is demonstrated on an illustrative example.

-

How do macro-financial shocks affect investor behavior and market dynamics?

Recent evidence on experience effects suggests a long-lasting influence of

personally experienced outcomes on investor beliefs and investment, but also

significant differences across older and younger generations. We formalize

experience-based learning in an OLG model, where different cross-cohort

experiences generate persistent heterogeneity in beliefs, portfolio choices,

and trade. The model allows us to characterize a novel link between investor

demographics and the dependence of prices on past dividends, while also

generating known features of asset prices, such as excess volatility and return

predictability. The model produces new implications for the cross-section of

asset holdings, trade volume, and investors' heterogenous responses to recent

financial crises, which we show to be in line with the data.

-

In this theoretical paper, I propose creation of a venture bank, able to

multiply the capital of a venture capital firm by at least 47 times, without

requiring access to the Federal Reserve or other central bank apart from

settlement. This concept rests on obtaining default swap instruments on loans

in order to create the capital required, and expand Tier 1 and 2 base capital.

Profitability depends on overall portfolio performance, availability of equity

default swaps, cost of default swap, and the multiple of original capital (MOC)

adopted by the venture bank. A new derivative financial instrument, the equity

default swap (EDS), to cover loans made as venture investments. An EDS is

similar to a credit default swap (CDS) but with some unique features. The

features and operation of these new derivative instruments are outlined along

with audit requirements. This instrument would be traded on open-outcry

exchanges with special features to ensure orderly operation of the market. It

is the creation of public markets for EDSs that makes possible the use of

public market pricing to indirectly provide a potential market capitalization

for the underlying venture-bank investment. Full coverage insulates the

venture-bank from losses in most situations, and multiplies profitability quite

dramatically in all scenarios. Ten year returns above 20X are attainable.

Further, a new feature for EDS derivatives, a clawback lien, closes out the

equity default swap. Here it is optimized at 77%, and is to be paid back to the

underwriter at a future date to prevent perverse incentive to deliberately

fail. This new feature creates an Equity Default Clawback Swap (EDCS) which can

be used safely. This proposal also solves an old problem in banking, because it

matches the term of the loan with the term of the investment. I show that the

venture-bank investment and the EDCS underwriting business are profitable.

-

Long term investment is one of the major investment strategies. However,

calculating intrinsic value of some company and evaluating shares for long term

investment is not easy, since analyst have to care about a large number of

financial indicators and evaluate them in a right manner. So far, little help

in predicting the direction of the company value over the longer period of time

has been provided from the machines. In this paper we present a machine

learning aided approach to evaluate the equity's future price over the long

time. Our method is able to correctly predict whether some company's value will

be 10% higher or not over the period of one year in 76.5% of cases.

-

Inter-firm organizations, which play a driving role in the economy of a

country, can be represented in the form of a customer-supplier network. Such a

network exhibits a heavy-tailed degree distribution, disassortative mixing and

a prominent community structure. We analyze a large-scale data set of

customer-supplier relationships containing data from one million Japanese

firms. Using a directed network framework, we show that the production network

exhibits the characteristics listed above. We conduct detailed investigations

to characterize the communities in the network. The topology within smaller

communities is found to be very close to a tree-like structure but becomes

denser as the community size increases. A large fraction (~40%) of firms with

relatively small in- or out-degrees have customers or suppliers solely from

within their own communities, indicating interactions of a highly local nature.

The interaction strengths between communities as measured by the

inter-community link weights follow a highly heterogeneous distribution. We

further present the statistically significant over-expressions of different

prefectures and sectors within different communities.

-

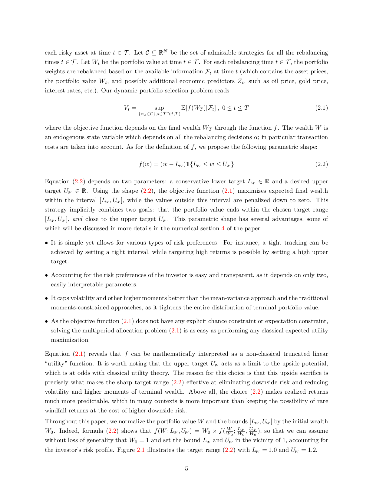

In this paper, we propose a novel investment strategy for portfolio

optimization problems. The proposed strategy maximizes the expected portfolio

value bounded within a targeted range, composed of a conservative lower target

representing a need for capital protection and a desired upper target

representing an investment goal. This strategy favorably shapes the entire

probability distribution of returns, as it simultaneously seeks a desired

expected return, cuts off downside risk and implicitly caps volatility and

higher moments. To illustrate the effectiveness of this investment strategy, we

study a multiperiod portfolio optimization problem with transaction costs and

develop a two-stage regression approach that improves the classical least

squares Monte Carlo (LSMC) algorithm when dealing with difficult payoffs, such

as highly concave, abruptly changing or discontinuous functions. Our numerical

results show substantial improvements over the classical LSMC algorithm for

both the constant relative risk-aversion (CRRA) utility approach and the

proposed skewed target range strategy (STRS). Our numerical results illustrate

the ability of the STRS to contain the portfolio value within the targeted

range. When compared with the CRRA utility approach, the STRS achieves a

similar mean-variance efficient frontier while delivering a better downside

risk-return trade-off.

-

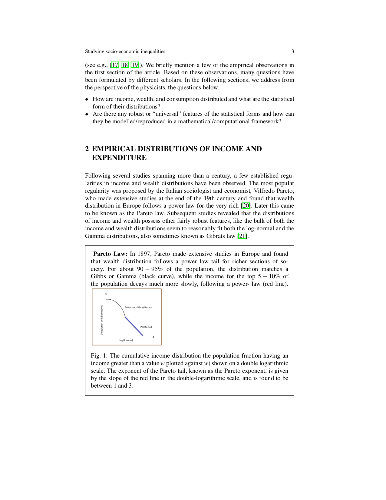

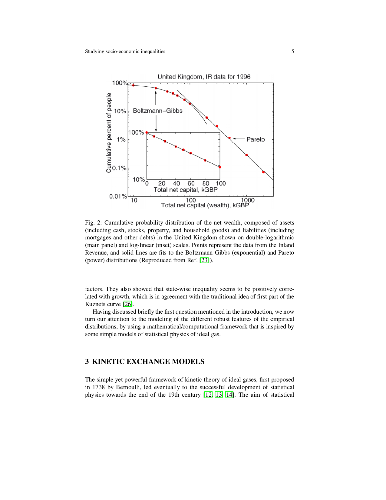

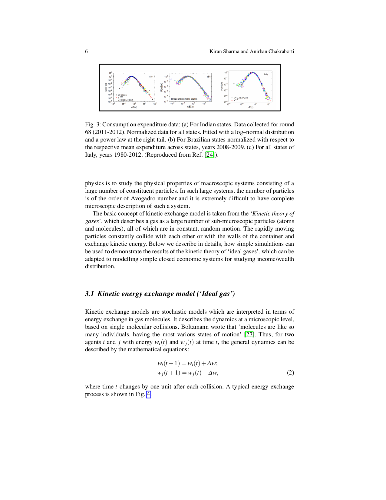

A brief overview of the models and data analyses of income, wealth,

consumption distributions by the physicists, are presented here. It has been

found empirically that the distributions of income and wealth possess fairly

robust features, like the bulk of both the income and wealth distributions seem

to reasonably fit both the log-normal and Gamma distributions, while the tail

of the distribution fits well to a power law (as first observed by sociologist

Pareto). We also present our recent studies of the unit-level expenditure on

consumption across multiple countries and multiple years, where it was found

that there exist invariant features of consumption distribution: the bulk is

log-normally distributed, followed by a power law tail at the limit. The

mechanisms leading to such inequalities and invariant features for the

distributions of socio-economic variables are not well-understood. We also

present some simple models from physics and demonstrate how they can be used to

explain some of these findings and their consequences.

-

We consider the problem of evaluating the quality of startup companies. This

can be quite challenging due to the rarity of successful startup companies and

the complexity of factors which impact such success. In this work we collect

data on tens of thousands of startup companies, their performance, the

backgrounds of their founders, and their investors. We develop a novel model

for the success of a startup company based on the first passage time of a

Brownian motion. The drift and diffusion of the Brownian motion associated with

a startup company are a function of features based its sector, founders, and

initial investors. All features are calculated using our massive dataset. Using

a Bayesian approach, we are able to obtain quantitative insights about the

features of successful startup companies from our model.

To test the performance of our model, we use it to build a portfolio of

companies where the goal is to maximize the probability of having at least one

company achieve an exit (IPO or acquisition), which we refer to as winning.

This $\textit{picking winners}$ framework is very general and can be used to

model many problems with low probability, high reward outcomes, such as

pharmaceutical companies choosing drugs to develop or studios selecting movies

to produce. We frame the construction of a picking winners portfolio as a

combinatorial optimization problem and show that a greedy solution has strong

performance guarantees. We apply the picking winners framework to the problem

of choosing a portfolio of startup companies. Using our model for the exit

probabilities, we are able to construct out of sample portfolios which achieve

exit rates as high as 60%, which is nearly double that of top venture capital

firms.

-

Designed to compete with fiat currencies, bitcoin proposes it is a

crypto-currency alternative. Bitcoin makes a number of false claims, including:

solving the double-spending problem is a good thing; bitcoin can be a reserve

currency for banking; hoarding equals saving, and that we should believe

bitcoin can expand by deflation to become a global transactional currency

supply. Bitcoin's developers combine technical implementation proficiency with

ignorance of currency and banking fundamentals. This has resulted in a failed

attempt to change finance. A set of recommendations to change finance are

provided in the Afterword: Investment/venture banking for the masses; Venture

banking to bring back what investment banks once were; Open-outcry exchange for

all CDS contracts; Attempting to develop CDS type contracts on investments in

startup and existing enterprises; and Improving the connection between startup

tech/ideas, business organization and investment.

-

This paper characterizes the equilibrium in a continuous time financial

market populated by heterogeneous agents who differ in their rate of relative

risk aversion and face convex portfolio constraints. The model is studied in an

application to margin constraints and found to match real world observations

about financial variables and leverage cycles. It is shown how margin

constraints increase the market price of risk and decrease the interest rate by

forcing more risk averse agents to hold more risky assets, producing a higher

equity risk premium. In addition, heterogeneity and margin constraints are

shown to produce both pro- and counter-cyclical leverage cycles. Beyond two

types, it is shown how constraints can cascade and how leverage can exhibit

highly non-linear dynamics. Finally, empirical results are given, documenting a

novel stylized fact which is predicted by the model, namely that the leverage

cycle is both pro- and counter-cyclical.

-

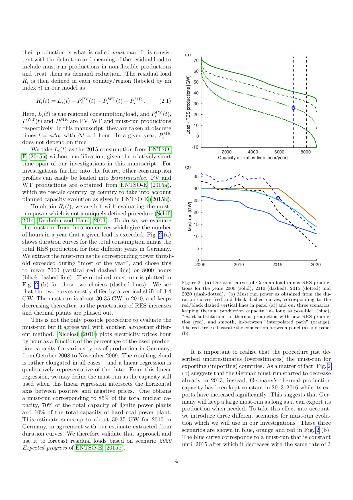

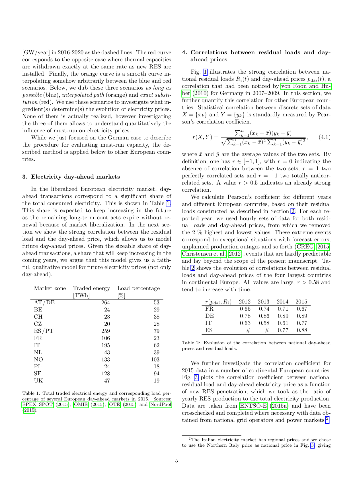

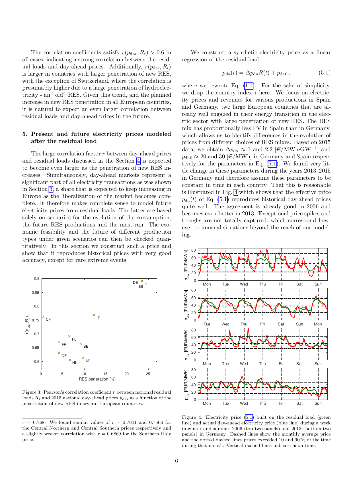

The paradox of the energy transition is that the low marginal costs of new

renewable energy sources (RES) drag electricity prices down and discourage

investments in flexible productions that are needed to compensate for the lack

of dispatchability of the new RES. The energy transition thus discourages the

investments that are required for its own harmonious expansion. To investigate

how this paradox can be overcome, we argue that, under certain assumptions,

future electricity prices are rather accurately modeled from the residual load

obtained by subtracting non-flexible productions from the load. Armed with the

resulting economic indicator, we investigate future revenues for European power

plants with various degree of flexibility. We find that, if neither carbon

taxes nor fuel prices change, flexible productions would be financially

rewarded better and sooner if the energy transition proceeds faster but at more

or less constant total production, i.e. by reducing the production of thermal

power plants at the same rate as the RES production increases. Less flexible

productions, on the other hand, would see their revenue grow more moderately.

Our results indicate that a faster energy transition with a quicker withdrawal

of thermal power plants would reward flexible productions faster.

-

This note comprises a negative resolution of the Efficient Market Hypothesis.

-

Different technological domains have significantly different rates of

performance improvement. Prior theory indicates that such differing rates

should influence the relative speed of diffusion of the products embodying the

different technologies since improvement in performance during the diffusion

process increases the desirability of the product diffusing. However, there has

not been a broad empirical attempt to examine this effect and to clarify the

underlying cause. Therefore, this paper reviews the theoretical basis and

focuses upon empirical tests of this effect across multiple products and their

underlying technologies. The results for 18 different diffusing products show

the expected relationship-faster diffusion for products based on more rapidly

improving technological domains- between technological improvement and

diffusion with strong statistical significance. The empirical examination also

demonstrates that technological improvement does not slow down in the latter

parts of diffusion when penetration does slow down. This finding indicates that

diffusion slow down in the latter stages is due to market saturation effects

and is not due to slowdown of performance improvement.

-

Financial markets provide a natural quantitative lab for understanding some

of the most advanced human behaviours. Among them is the use of mathematical

tools known as financial instruments. Besides money, the two most fundamental

financial instruments are bonds and equities. More than 30 years ago Mehra and

Prescott found the numerical performance of equities relative to government

bonds could not be explained by consumption-based (mainstream) economic

theories. This empirical observation, known as the Equity Premium Puzzle, has

been defying mainstream economics ever since. The recent financial crisis

revealed an even deeper need for understanding financial products. We show how

understanding the rational nature of product design resolves the Equity Premium

Puzzle. In doing so we obtain an experimentally tested theory of product

design.

-

Cooperation is a persistent behavioral pattern of entities pooling and

sharing resources. Its ubiquity in nature poses a conundrum. Whenever two

entities cooperate, one must willingly relinquish something of value to the

other. Why is this apparent altruism favored in evolution? Classical solutions

assume a net fitness gain in a cooperative transaction which, through

reciprocity or relatedness, finds its way back from recipient to donor. We seek

the source of this fitness gain. Our analysis rests on the insight that

evolutionary processes are typically multiplicative and noisy. Fluctuations

have a net negative effect on the long-time growth rate of resources but no

effect on the growth rate of their expectation value. This is an example of

non-ergodicity. By reducing the amplitude of fluctuations, pooling and sharing

increases the long-time growth rate for cooperating entities, meaning that

cooperators outgrow similar non-cooperators. We identify this increase in

growth rate as the net fitness gain, consistent with the concept of geometric

mean fitness in the biological literature. This constitutes a fundamental

mechanism for the evolution of cooperation. Its minimal assumptions make it a

candidate explanation of cooperation in settings too simple for other fitness

gains, such as emergent function and specialization, to be probable. One such

example is the transition from single cells to early multicellular life.

-

The functioning of the cryptocurrency Bitcoin relies on the open availability

of the entire history of its transactions. This makes it a particularly

interesting socio-economic system to analyse from the point of view of network

science. Here we analyse the evolution of the network of Bitcoin transactions

between users. We achieve this by using the complete transaction history from

December 5th 2011 to December 23rd 2013. This period includes three bubbles

experienced by the Bitcoin price. In particular, we focus on the global and

local structural properties of the user network and their variation in relation

to the different period of price surge and decline. By analysing the temporal

variation of the heterogeneity of the connectivity patterns we gain insights on

the different mechanisms that take place during bubbles, and find that hubs

(i.e., the most connected nodes) had a fundamental role in triggering the burst

of the second bubble. Finally, we examine the local topological structures of

interactions between users, we discover that the relative frequency of triadic

interactions experiences a strong change before, during and after a bubble, and

suggest that the importance of the hubs grows during the bubble. These results

provide further evidence that the behaviour of the hubs during bubbles

significantly increases the systemic risk of the Bitcoin network, and discuss

the implications on public policy interventions.

-

We analyze total, asymmetric and frequency connectedness between the oil and

forex markets using high-frequency intra-day data over 2007 -- 2015.

Methodologically, we extend the Diebold-Yilmaz spillover index in two ways to

account for asymmetric and frequency connectedness. Empirically, our results

show that by combining crude oil with the set of currencies a total

connectedness of the portfolio is lower than the total connectedness of the

forex market itself. Further, in terms of asymmetries we show that bad

volatility dominates connectedness on the forex market. However, when we add

oil into a hypothetical portfolio of oil and foreign currencies, asymmetry in

connectedness between the two classes of assets reverses in favor of the good

volatility. Finally, the frequency connectedness analysis reveals that dynamic

of the shorter and longer term connectedness dramatically differs. While

shorter-term connectedness is usually low, the long-term connectedness sharply

rises during the global financial crisis, European debt crisis, and after the

oil price drop in 2014. Hence, the long-term connectedness reflects worrisome

beliefs of investors and correlates with the increased market uncertainty.

-

This paper provides a holistic study of how stock prices vary in their

response to financial disclosures across different topics. Thereby, we

specifically shed light into the extensive amount of filings for which no a

priori categorization of their content exists. For this purpose, we utilize an

approach from data mining - namely, latent Dirichlet allocation - as a means of

topic modeling. This technique facilitates our task of automatically

categorizing, ex ante, the content of more than 70,000 regulatory 8-K filings

from U.S. companies. We then evaluate the subsequent stock market reaction. Our

empirical evidence suggests a considerable discrepancy among various types of

news stories in terms of their relevance and impact on financial markets. For

instance, we find a statistically significant abnormal return in response to

earnings results and credit rating, but also for disclosures regarding business

strategy, the health sector, as well as mergers and acquisitions. Our results

yield findings that benefit managers, investors and policy-makers by indicating

how regulatory filings should be structured and the topics most likely to

precede changes in stock valuations.

-

Two critical questions about intergenerational outcomes are: one, whether

significant barriers or traps exist between different social or economic

strata; and two, the extent to which intergenerational outcomes do (or can be

used to) affect individual investment and consumption decisions. We develop a

model to explicitly relate these two questions, and prove the first such `rat

race' theorem, showing that a fundamental relationship exists between high

levels of individual investment and the existence of a wealth trap, which traps

otherwise identical agents at a lower level of wealth. Our simple model of

intergenerational wealth dynamics involves agents which balance current

consumption with investment in a single descendant. Investments then determine

descendant wealth via a potentially nonlinear and discontinuous competitiveness

function about which we do not make concavity assumptions. From this model we

demonstrate how to infer such a competitiveness function from investments,

along with geometric criteria to determine individual decisions. Additionally

we investigate the stability of a wealth distribution, both to local

perturbations and to the introduction of new agents with no wealth.

-

Relationship lending is broadly interpreted as a strong partnership between a

lender and a borrower. Nevertheless, we still lack consensus regarding how to

quantify the strength of a lending relationship, while simple statistics such

as the frequency and volume of loans have been used as proxies in previous

studies. Here, we propose statistical tests to identify relationship lending as

a significant tie between banks. Application of the proposed method to the

Italian interbank networks reveals that the fraction of relationship lending

among all bilateral trades has been quite stable and that the relationship

lenders tend to impose high interest rates at the time of financial distress.

-

The crowd panic and its contagion play non-negligible roles at the time of

the stock crash, especially for China where inexperienced investors dominate

the market. However, existing models rarely consider investors in networking

stocks and accordingly miss the exact knowledge of how panic contagion leads to

abrupt crash. In this paper, by networking stocks of sharing common mutual

funds, a new methodology of investigating the market crash is presented. It is

surprisingly revealed that the herding, which origins in the mimic of seeking

for high diversity across investment strategies to lower individual risk, will

produce too-connected-to-fail stocks and reluctantly boosts the systemic risk

of the entire market. Though too-connected stocks might be relatively stable

during the crisis, they are so influential that a small downward fluctuation

will cascade to trigger severe drops of massive successor stocks, implying that

their falls might be unexpectedly amplified by the collective panic and result

in the market crash. Our findings suggest that the whole picture of portfolio

strategy has to be carefully supervised to reshape the stock network.

-

The concept of progress has characterized human society from millennia.

However, this concept is elusive and too often given for certain. The goal of

this paper is to suggest a general definition of human progress that satisfies,

whenever possible the conditions of independence, generality, epistemological

applicability and empirical correctness. This study proposes, within a

pragmatic approach, human progress as an inexhaustible process driven by an

ideal of maximum wellbeing of purposeful people which, on attainment of any of

its goals or objectives for increasing wellbeing, then seek another

consequential goal and objective, endlessly, which more closely approximates

its ideal fixed in new socioeconomic contexts over time and space. The human

progress, in the global, capitalistic, and post-humanistic Era, improves the

fundamental life-interests represented by health, wealth, expansion of

knowledge, technology and freedom directed to increase wellbeing throughout the

society. These factors support the acquisition by humanity of better and more

complex forms of life. However, this study shows the inconsistency of the

equation economic growth= progress because human progress also generates,

during its continuous process without limit, negative effects for human being,

environment and society.

-

This paper examines the time series properties of cryptocurrency assets, such

as Bitcoin, using established econometric inference techniques, namely models

of the GARCH family. The contribution of this study is twofold. I explore the

time series properties of cryptocurrencies, a new type of financial asset on

which there appears to be little or no literature. I suggest an improved

econometric specification to that which has been recently proposed in Chu et al

(2017), the first econometric study to examine the price dynamics of the most

popular cryptocurrencies. Questions regarding the reliability of their study

stem from the authors mis-diagnosing the distribution of GARCH innovations.

Checks are performed on whether innovations are Gaussian or GED by using

Kolmogorov type non-parametric tests and Khmaladze's martingale transformation.

Null of gaussianity is strongly rejected for all GARCH(p,q) models, with $p,q

\in \{1,\ldots,5 \}$, for all cryptocurrencies in sample. For tests of

normality, I make use of the Gauss-Kronrod quadrature. Parameters of GARCH

models are estimated with generalized error distribution innovations using

maximum likelihood. For calculating P-values, the parametric bootstrap method

is used. Arguing against Chu et al (2017), I show that there is a strong

empirical argument against modelling innovations under some common assumptions.

-

Capital investment literature implicitly assumes that exponential growth of

consumption can last indefinitely into the future. However, in the context of

climate finance with benefits on current investments deferred to centuries from

now, this process is fundamentally constrained by finite biophysical resources

of Earth. Similarly to a population dynamics, a negative feedback mechanism

will eventually prevent unlimited growth of consumption and reduce its rate. We

apply this basic insight to valuation of long-term social discount rates.

Combining the Ramsey optimal growth framework with the marginal-utility

approach and the Verhulst logistic model, we demonstrate that inevitable

slowing down of consumption growth leads to a declining long-term tail of the

discount curve. This dynamic effect becomes stronger than the well-known

"precautionary" effect related to uncertainty of a social planer in future

growth rates of consumption in the relatively near future, which has been

estimated here as about 100 years from now (the lower boundary). Our

formulation yields remarkably simple expressions for time-declining discount

rates which generalize the classic Ramsey formula. The derived results can help

to shape a more realistic long-term social discounting policy. Furthermore,

with the obvious redefinition of the key parameters of the model, the obtained

results are directly applicable for estimations of the expected long-term

population growth curve in stochastic environments.

-

We employ stochastic dynamic microsimulations to analyse and forecast the

pension cost dependency ratio for England and Wales from 1991 to 2061,

evaluating the impact of the ongoing state pension reforms and changes in

international migration patterns under different Brexit scenarios. To fully

account for the recently observed volatility in life expectancies, we propose

mortality rate model based on deep learning techniques, which discovers complex

patterns in data and extrapolated trends. Our results show that the recent

reforms can effectively stave off the "pension crisis" and bring back the

system on a sounder fiscal footing. At the same time, increasingly more workers

can expect to spend greater share of their lifespan in retirement, despite the

eligibility age rises. The population ageing due to the observed postponement

of death until senectitude often occurs with the compression of morbidity, and

thus will not, perforce, intrinsically strain healthcare costs. To a lesser

degree, the future pension cost dependency ratio will depend on the post-Brexit

relations between the UK and the EU, with "soft" alignment on the free movement

lowering the relative cost of the pension system compared to the "hard" one. In

the long term, however, the ratio has a rising tendency.

In this paper, we present own point of view how the unexpected fluctuations of the long-term real interest rate can be explained. We describe a macroeconomic environment by the modification of the fundamental macroeconomic equilibrium model called the IS-LM model. Last but not least, we suggest a possible cooperation between the fiscal and monetary policy to reduce these fluctuations. Our modelling is demonstrated on an illustrative example.

In this paper, we present own point of view how the unexpected fluctuations of the long-term real interest rate can be explained. We describe a macroeconomic environment by the modification of the fundamental macroeconomic equilibrium model called the IS-LM model. Last but not least, we suggest a possible cooperation between the fiscal and monetary policy to reduce these fluctuations. Our modelling is demonstrated on an illustrative example.

How do macro-financial shocks affect investor behavior and market dynamics? Recent evidence on experience effects suggests a long-lasting influence of personally experienced outcomes on investor beliefs and investment, but also significant differences across older and younger generations. We formalize experience-based learning in an OLG model, where different cross-cohort experiences generate persistent heterogeneity in beliefs, portfolio choices, and trade. The model allows us to characterize a novel link between investor demographics and the dependence of prices on past dividends, while also generating known features of asset prices, such as excess volatility and return predictability. The model produces new implications for the cross-section of asset holdings, trade volume, and investors' heterogenous responses to recent financial crises, which we show to be in line with the data.

How do macro-financial shocks affect investor behavior and market dynamics? Recent evidence on experience effects suggests a long-lasting influence of personally experienced outcomes on investor beliefs and investment, but also significant differences across older and younger generations. We formalize experience-based learning in an OLG model, where different cross-cohort experiences generate persistent heterogeneity in beliefs, portfolio choices, and trade. The model allows us to characterize a novel link between investor demographics and the dependence of prices on past dividends, while also generating known features of asset prices, such as excess volatility and return predictability. The model produces new implications for the cross-section of asset holdings, trade volume, and investors' heterogenous responses to recent financial crises, which we show to be in line with the data.

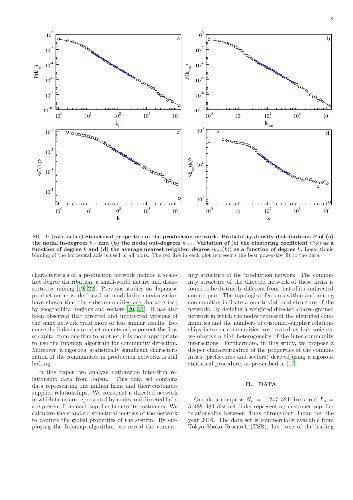

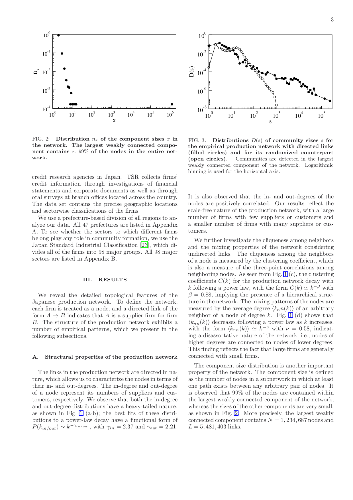

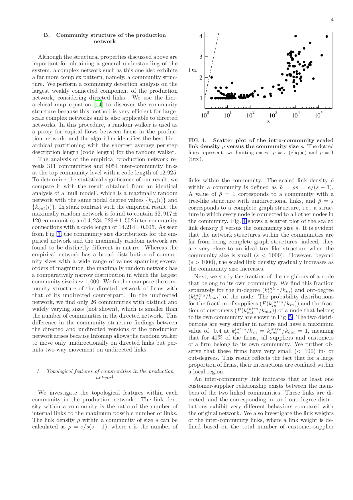

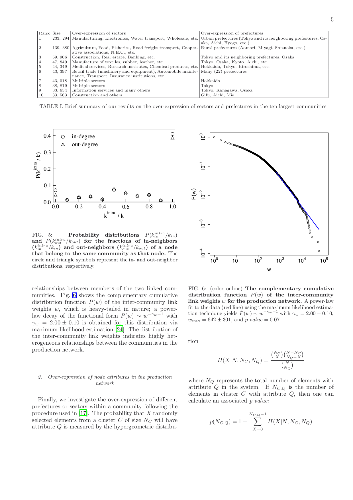

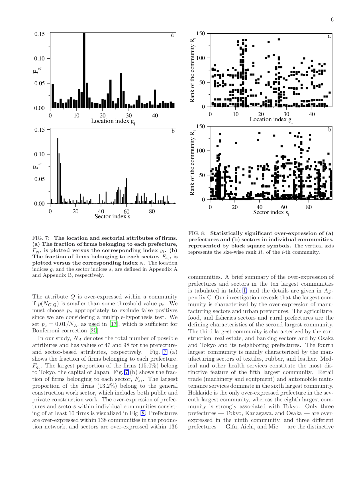

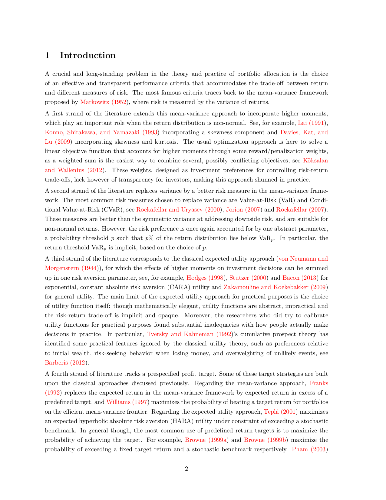

Inter-firm organizations, which play a driving role in the economy of a country, can be represented in the form of a customer-supplier network. Such a network exhibits a heavy-tailed degree distribution, disassortative mixing and a prominent community structure. We analyze a large-scale data set of customer-supplier relationships containing data from one million Japanese firms. Using a directed network framework, we show that the production network exhibits the characteristics listed above. We conduct detailed investigations to characterize the communities in the network. The topology within smaller communities is found to be very close to a tree-like structure but becomes denser as the community size increases. A large fraction (~40%) of firms with relatively small in- or out-degrees have customers or suppliers solely from within their own communities, indicating interactions of a highly local nature. The interaction strengths between communities as measured by the inter-community link weights follow a highly heterogeneous distribution. We further present the statistically significant over-expressions of different prefectures and sectors within different communities.

Inter-firm organizations, which play a driving role in the economy of a country, can be represented in the form of a customer-supplier network. Such a network exhibits a heavy-tailed degree distribution, disassortative mixing and a prominent community structure. We analyze a large-scale data set of customer-supplier relationships containing data from one million Japanese firms. Using a directed network framework, we show that the production network exhibits the characteristics listed above. We conduct detailed investigations to characterize the communities in the network. The topology within smaller communities is found to be very close to a tree-like structure but becomes denser as the community size increases. A large fraction (~40%) of firms with relatively small in- or out-degrees have customers or suppliers solely from within their own communities, indicating interactions of a highly local nature. The interaction strengths between communities as measured by the inter-community link weights follow a highly heterogeneous distribution. We further present the statistically significant over-expressions of different prefectures and sectors within different communities.

In this paper, we propose a novel investment strategy for portfolio optimization problems. The proposed strategy maximizes the expected portfolio value bounded within a targeted range, composed of a conservative lower target representing a need for capital protection and a desired upper target representing an investment goal. This strategy favorably shapes the entire probability distribution of returns, as it simultaneously seeks a desired expected return, cuts off downside risk and implicitly caps volatility and higher moments. To illustrate the effectiveness of this investment strategy, we study a multiperiod portfolio optimization problem with transaction costs and develop a two-stage regression approach that improves the classical least squares Monte Carlo (LSMC) algorithm when dealing with difficult payoffs, such as highly concave, abruptly changing or discontinuous functions. Our numerical results show substantial improvements over the classical LSMC algorithm for both the constant relative risk-aversion (CRRA) utility approach and the proposed skewed target range strategy (STRS). Our numerical results illustrate the ability of the STRS to contain the portfolio value within the targeted range. When compared with the CRRA utility approach, the STRS achieves a similar mean-variance efficient frontier while delivering a better downside risk-return trade-off.

In this paper, we propose a novel investment strategy for portfolio optimization problems. The proposed strategy maximizes the expected portfolio value bounded within a targeted range, composed of a conservative lower target representing a need for capital protection and a desired upper target representing an investment goal. This strategy favorably shapes the entire probability distribution of returns, as it simultaneously seeks a desired expected return, cuts off downside risk and implicitly caps volatility and higher moments. To illustrate the effectiveness of this investment strategy, we study a multiperiod portfolio optimization problem with transaction costs and develop a two-stage regression approach that improves the classical least squares Monte Carlo (LSMC) algorithm when dealing with difficult payoffs, such as highly concave, abruptly changing or discontinuous functions. Our numerical results show substantial improvements over the classical LSMC algorithm for both the constant relative risk-aversion (CRRA) utility approach and the proposed skewed target range strategy (STRS). Our numerical results illustrate the ability of the STRS to contain the portfolio value within the targeted range. When compared with the CRRA utility approach, the STRS achieves a similar mean-variance efficient frontier while delivering a better downside risk-return trade-off.

A brief overview of the models and data analyses of income, wealth, consumption distributions by the physicists, are presented here. It has been found empirically that the distributions of income and wealth possess fairly robust features, like the bulk of both the income and wealth distributions seem to reasonably fit both the log-normal and Gamma distributions, while the tail of the distribution fits well to a power law (as first observed by sociologist Pareto). We also present our recent studies of the unit-level expenditure on consumption across multiple countries and multiple years, where it was found that there exist invariant features of consumption distribution: the bulk is log-normally distributed, followed by a power law tail at the limit. The mechanisms leading to such inequalities and invariant features for the distributions of socio-economic variables are not well-understood. We also present some simple models from physics and demonstrate how they can be used to explain some of these findings and their consequences.

A brief overview of the models and data analyses of income, wealth, consumption distributions by the physicists, are presented here. It has been found empirically that the distributions of income and wealth possess fairly robust features, like the bulk of both the income and wealth distributions seem to reasonably fit both the log-normal and Gamma distributions, while the tail of the distribution fits well to a power law (as first observed by sociologist Pareto). We also present our recent studies of the unit-level expenditure on consumption across multiple countries and multiple years, where it was found that there exist invariant features of consumption distribution: the bulk is log-normally distributed, followed by a power law tail at the limit. The mechanisms leading to such inequalities and invariant features for the distributions of socio-economic variables are not well-understood. We also present some simple models from physics and demonstrate how they can be used to explain some of these findings and their consequences.

We consider the problem of evaluating the quality of startup companies. This can be quite challenging due to the rarity of successful startup companies and the complexity of factors which impact such success. In this work we collect data on tens of thousands of startup companies, their performance, the backgrounds of their founders, and their investors. We develop a novel model for the success of a startup company based on the first passage time of a Brownian motion. The drift and diffusion of the Brownian motion associated with a startup company are a function of features based its sector, founders, and initial investors. All features are calculated using our massive dataset. Using a Bayesian approach, we are able to obtain quantitative insights about the features of successful startup companies from our model. To test the performance of our model, we use it to build a portfolio of companies where the goal is to maximize the probability of having at least one company achieve an exit (IPO or acquisition), which we refer to as winning. This $\textit{picking winners}$ framework is very general and can be used to model many problems with low probability, high reward outcomes, such as pharmaceutical companies choosing drugs to develop or studios selecting movies to produce. We frame the construction of a picking winners portfolio as a combinatorial optimization problem and show that a greedy solution has strong performance guarantees. We apply the picking winners framework to the problem of choosing a portfolio of startup companies. Using our model for the exit probabilities, we are able to construct out of sample portfolios which achieve exit rates as high as 60%, which is nearly double that of top venture capital firms.

We consider the problem of evaluating the quality of startup companies. This can be quite challenging due to the rarity of successful startup companies and the complexity of factors which impact such success. In this work we collect data on tens of thousands of startup companies, their performance, the backgrounds of their founders, and their investors. We develop a novel model for the success of a startup company based on the first passage time of a Brownian motion. The drift and diffusion of the Brownian motion associated with a startup company are a function of features based its sector, founders, and initial investors. All features are calculated using our massive dataset. Using a Bayesian approach, we are able to obtain quantitative insights about the features of successful startup companies from our model. To test the performance of our model, we use it to build a portfolio of companies where the goal is to maximize the probability of having at least one company achieve an exit (IPO or acquisition), which we refer to as winning. This $\textit{picking winners}$ framework is very general and can be used to model many problems with low probability, high reward outcomes, such as pharmaceutical companies choosing drugs to develop or studios selecting movies to produce. We frame the construction of a picking winners portfolio as a combinatorial optimization problem and show that a greedy solution has strong performance guarantees. We apply the picking winners framework to the problem of choosing a portfolio of startup companies. Using our model for the exit probabilities, we are able to construct out of sample portfolios which achieve exit rates as high as 60%, which is nearly double that of top venture capital firms.

This paper characterizes the equilibrium in a continuous time financial market populated by heterogeneous agents who differ in their rate of relative risk aversion and face convex portfolio constraints. The model is studied in an application to margin constraints and found to match real world observations about financial variables and leverage cycles. It is shown how margin constraints increase the market price of risk and decrease the interest rate by forcing more risk averse agents to hold more risky assets, producing a higher equity risk premium. In addition, heterogeneity and margin constraints are shown to produce both pro- and counter-cyclical leverage cycles. Beyond two types, it is shown how constraints can cascade and how leverage can exhibit highly non-linear dynamics. Finally, empirical results are given, documenting a novel stylized fact which is predicted by the model, namely that the leverage cycle is both pro- and counter-cyclical.

This paper characterizes the equilibrium in a continuous time financial market populated by heterogeneous agents who differ in their rate of relative risk aversion and face convex portfolio constraints. The model is studied in an application to margin constraints and found to match real world observations about financial variables and leverage cycles. It is shown how margin constraints increase the market price of risk and decrease the interest rate by forcing more risk averse agents to hold more risky assets, producing a higher equity risk premium. In addition, heterogeneity and margin constraints are shown to produce both pro- and counter-cyclical leverage cycles. Beyond two types, it is shown how constraints can cascade and how leverage can exhibit highly non-linear dynamics. Finally, empirical results are given, documenting a novel stylized fact which is predicted by the model, namely that the leverage cycle is both pro- and counter-cyclical.

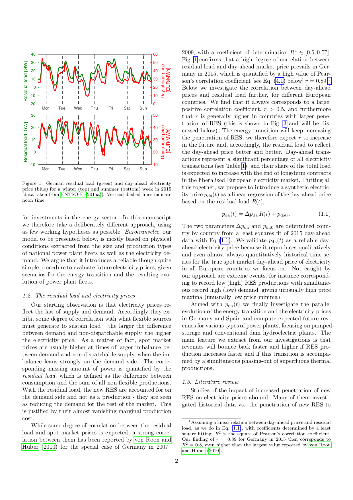

The paradox of the energy transition is that the low marginal costs of new renewable energy sources (RES) drag electricity prices down and discourage investments in flexible productions that are needed to compensate for the lack of dispatchability of the new RES. The energy transition thus discourages the investments that are required for its own harmonious expansion. To investigate how this paradox can be overcome, we argue that, under certain assumptions, future electricity prices are rather accurately modeled from the residual load obtained by subtracting non-flexible productions from the load. Armed with the resulting economic indicator, we investigate future revenues for European power plants with various degree of flexibility. We find that, if neither carbon taxes nor fuel prices change, flexible productions would be financially rewarded better and sooner if the energy transition proceeds faster but at more or less constant total production, i.e. by reducing the production of thermal power plants at the same rate as the RES production increases. Less flexible productions, on the other hand, would see their revenue grow more moderately. Our results indicate that a faster energy transition with a quicker withdrawal of thermal power plants would reward flexible productions faster.

The paradox of the energy transition is that the low marginal costs of new renewable energy sources (RES) drag electricity prices down and discourage investments in flexible productions that are needed to compensate for the lack of dispatchability of the new RES. The energy transition thus discourages the investments that are required for its own harmonious expansion. To investigate how this paradox can be overcome, we argue that, under certain assumptions, future electricity prices are rather accurately modeled from the residual load obtained by subtracting non-flexible productions from the load. Armed with the resulting economic indicator, we investigate future revenues for European power plants with various degree of flexibility. We find that, if neither carbon taxes nor fuel prices change, flexible productions would be financially rewarded better and sooner if the energy transition proceeds faster but at more or less constant total production, i.e. by reducing the production of thermal power plants at the same rate as the RES production increases. Less flexible productions, on the other hand, would see their revenue grow more moderately. Our results indicate that a faster energy transition with a quicker withdrawal of thermal power plants would reward flexible productions faster.

This note comprises a negative resolution of the Efficient Market Hypothesis.

This note comprises a negative resolution of the Efficient Market Hypothesis.

Financial markets provide a natural quantitative lab for understanding some of the most advanced human behaviours. Among them is the use of mathematical tools known as financial instruments. Besides money, the two most fundamental financial instruments are bonds and equities. More than 30 years ago Mehra and Prescott found the numerical performance of equities relative to government bonds could not be explained by consumption-based (mainstream) economic theories. This empirical observation, known as the Equity Premium Puzzle, has been defying mainstream economics ever since. The recent financial crisis revealed an even deeper need for understanding financial products. We show how understanding the rational nature of product design resolves the Equity Premium Puzzle. In doing so we obtain an experimentally tested theory of product design.

Financial markets provide a natural quantitative lab for understanding some of the most advanced human behaviours. Among them is the use of mathematical tools known as financial instruments. Besides money, the two most fundamental financial instruments are bonds and equities. More than 30 years ago Mehra and Prescott found the numerical performance of equities relative to government bonds could not be explained by consumption-based (mainstream) economic theories. This empirical observation, known as the Equity Premium Puzzle, has been defying mainstream economics ever since. The recent financial crisis revealed an even deeper need for understanding financial products. We show how understanding the rational nature of product design resolves the Equity Premium Puzzle. In doing so we obtain an experimentally tested theory of product design.

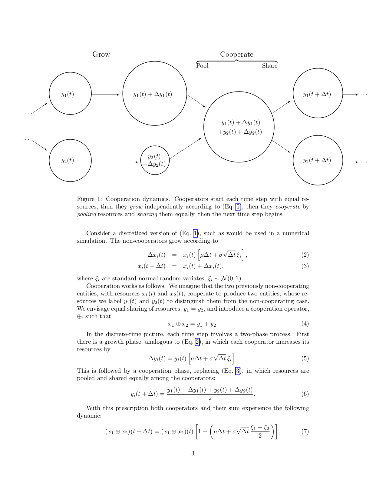

Cooperation is a persistent behavioral pattern of entities pooling and sharing resources. Its ubiquity in nature poses a conundrum. Whenever two entities cooperate, one must willingly relinquish something of value to the other. Why is this apparent altruism favored in evolution? Classical solutions assume a net fitness gain in a cooperative transaction which, through reciprocity or relatedness, finds its way back from recipient to donor. We seek the source of this fitness gain. Our analysis rests on the insight that evolutionary processes are typically multiplicative and noisy. Fluctuations have a net negative effect on the long-time growth rate of resources but no effect on the growth rate of their expectation value. This is an example of non-ergodicity. By reducing the amplitude of fluctuations, pooling and sharing increases the long-time growth rate for cooperating entities, meaning that cooperators outgrow similar non-cooperators. We identify this increase in growth rate as the net fitness gain, consistent with the concept of geometric mean fitness in the biological literature. This constitutes a fundamental mechanism for the evolution of cooperation. Its minimal assumptions make it a candidate explanation of cooperation in settings too simple for other fitness gains, such as emergent function and specialization, to be probable. One such example is the transition from single cells to early multicellular life.

Cooperation is a persistent behavioral pattern of entities pooling and sharing resources. Its ubiquity in nature poses a conundrum. Whenever two entities cooperate, one must willingly relinquish something of value to the other. Why is this apparent altruism favored in evolution? Classical solutions assume a net fitness gain in a cooperative transaction which, through reciprocity or relatedness, finds its way back from recipient to donor. We seek the source of this fitness gain. Our analysis rests on the insight that evolutionary processes are typically multiplicative and noisy. Fluctuations have a net negative effect on the long-time growth rate of resources but no effect on the growth rate of their expectation value. This is an example of non-ergodicity. By reducing the amplitude of fluctuations, pooling and sharing increases the long-time growth rate for cooperating entities, meaning that cooperators outgrow similar non-cooperators. We identify this increase in growth rate as the net fitness gain, consistent with the concept of geometric mean fitness in the biological literature. This constitutes a fundamental mechanism for the evolution of cooperation. Its minimal assumptions make it a candidate explanation of cooperation in settings too simple for other fitness gains, such as emergent function and specialization, to be probable. One such example is the transition from single cells to early multicellular life.

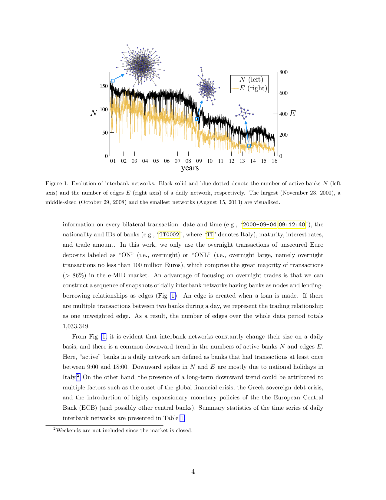

Relationship lending is broadly interpreted as a strong partnership between a lender and a borrower. Nevertheless, we still lack consensus regarding how to quantify the strength of a lending relationship, while simple statistics such as the frequency and volume of loans have been used as proxies in previous studies. Here, we propose statistical tests to identify relationship lending as a significant tie between banks. Application of the proposed method to the Italian interbank networks reveals that the fraction of relationship lending among all bilateral trades has been quite stable and that the relationship lenders tend to impose high interest rates at the time of financial distress.

Relationship lending is broadly interpreted as a strong partnership between a lender and a borrower. Nevertheless, we still lack consensus regarding how to quantify the strength of a lending relationship, while simple statistics such as the frequency and volume of loans have been used as proxies in previous studies. Here, we propose statistical tests to identify relationship lending as a significant tie between banks. Application of the proposed method to the Italian interbank networks reveals that the fraction of relationship lending among all bilateral trades has been quite stable and that the relationship lenders tend to impose high interest rates at the time of financial distress.

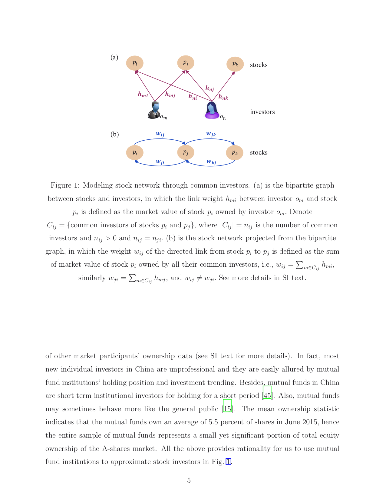

The crowd panic and its contagion play non-negligible roles at the time of the stock crash, especially for China where inexperienced investors dominate the market. However, existing models rarely consider investors in networking stocks and accordingly miss the exact knowledge of how panic contagion leads to abrupt crash. In this paper, by networking stocks of sharing common mutual funds, a new methodology of investigating the market crash is presented. It is surprisingly revealed that the herding, which origins in the mimic of seeking for high diversity across investment strategies to lower individual risk, will produce too-connected-to-fail stocks and reluctantly boosts the systemic risk of the entire market. Though too-connected stocks might be relatively stable during the crisis, they are so influential that a small downward fluctuation will cascade to trigger severe drops of massive successor stocks, implying that their falls might be unexpectedly amplified by the collective panic and result in the market crash. Our findings suggest that the whole picture of portfolio strategy has to be carefully supervised to reshape the stock network.

The crowd panic and its contagion play non-negligible roles at the time of the stock crash, especially for China where inexperienced investors dominate the market. However, existing models rarely consider investors in networking stocks and accordingly miss the exact knowledge of how panic contagion leads to abrupt crash. In this paper, by networking stocks of sharing common mutual funds, a new methodology of investigating the market crash is presented. It is surprisingly revealed that the herding, which origins in the mimic of seeking for high diversity across investment strategies to lower individual risk, will produce too-connected-to-fail stocks and reluctantly boosts the systemic risk of the entire market. Though too-connected stocks might be relatively stable during the crisis, they are so influential that a small downward fluctuation will cascade to trigger severe drops of massive successor stocks, implying that their falls might be unexpectedly amplified by the collective panic and result in the market crash. Our findings suggest that the whole picture of portfolio strategy has to be carefully supervised to reshape the stock network.