-

This tutorial provides a gentle introduction to the particle

Metropolis-Hastings (PMH) algorithm for parameter inference in nonlinear

state-space models together with a software implementation in the statistical

programming language R. We employ a step-by-step approach to develop an

implementation of the PMH algorithm (and the particle filter within) together

with the reader. This final implementation is also available as the package

pmhtutorial in the CRAN repository. Throughout the tutorial, we provide some

intuition as to how the algorithm operates and discuss some solutions to

problems that might occur in practice. To illustrate the use of PMH, we

consider parameter inference in a linear Gaussian state-space model with

synthetic data and a nonlinear stochastic volatility model with real-world

data.

-

We review the state of the art of clustering financial time series and the

study of their correlations alongside other interaction networks. The aim of

this review is to gather in one place the relevant material from different

fields, e.g. machine learning, information geometry, econophysics, statistical

physics, econometrics, behavioral finance. We hope it will help researchers to

use more effectively this alternative modeling of the financial time series.

Decision makers and quantitative researchers may also be able to leverage its

insights. Finally, we also hope that this review will form the basis of an open

toolbox to study correlations, hierarchies, networks and clustering in

financial markets.

-

In this paper, we build tests for the presence of residual noise in a model

where the market microstructure noise is a known parametric function of some

variables from the limit order book. The tests compare two distinct

quasi-maximum likelihood estimators of volatility, where the related model

includes a residual noise in the market microstructure noise or not. The limit

theory is investigated in a general nonparametric framework. In the presence of

residual noise, we examine the central limit theory of the related

quasi-maximum likelihood estimation approach.

-

We give complete algorithms and source code for constructing (multilevel)

statistical industry classifications, including methods for fixing the number

of clusters at each level (and the number of levels). Under the hood there are

clustering algorithms (e.g., k-means). However, what should we cluster?

Correlations? Returns? The answer turns out to be neither and our backtests

suggest that these details make a sizable difference. We also give an algorithm

and source code for building "hybrid" industry classifications by improving

off-the-shelf "fundamental" industry classifications by applying our

statistical industry classification methods to them. The presentation is

intended to be pedagogical and geared toward practical applications in

quantitative trading.

-

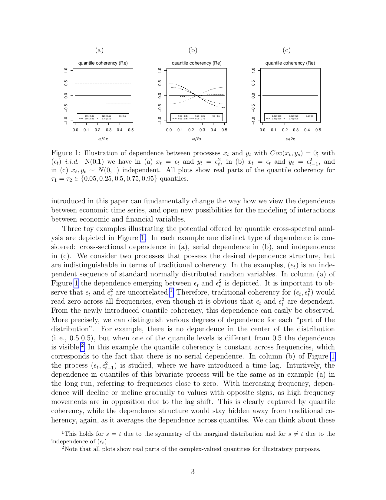

In this paper, we introduce quantile coherency to measure general dependence

structures emerging in the joint distribution in the frequency domain and argue

that this type of dependence is natural for economic time series but remains

invisible when only the traditional analysis is employed. We define estimators

which capture the general dependence structure, provide a detailed analysis of

their asymptotic properties and discuss how to conduct inference for a general

class of possibly nonlinear processes. In an empirical illustration we examine

the dependence of bivariate stock market returns and shed new light on

measurement of tail risk in financial markets. We also provide a modelling

exercise to illustrate how applied researchers can benefit from using quantile

coherency when assessing time series models.

-

In a very high-dimensional vector space, two randomly-chosen vectors are

almost orthogonal with high probability. Starting from this observation, we

develop a statistical factor model, the random factor model, in which factors

are chosen at random based on the random projection method. Randomness of

factors has the consequence that covariance matrix is well preserved in a

linear factor representation. It also enables derivation of probabilistic

bounds for the accuracy of the random factor representation of time-series,

their cross-correlations and covariances. As an application, we analyze

reproduction of time-series and their cross-correlation coefficients in the

well-diversified Russell 3,000 equity index.

-

We examine the effect of investor attention spillover on stock return

predictability. Using a novel measure, the News Network Triggered Attention

index (NNTA), we find that NNTA negatively predicts market returns with a

monthly in(out)-of-sample R-square of 5.97% (5.80%). In the cross-section, a

long-short portfolio based on news co-occurrence generates a significant

monthly alpha of 68 basis points. The results are robust to the inclusion of

alternative attention proxies, sentiment measures, other news- and

information-based predictors, across recession and expansion periods. We

further validate the attention spillover effect by showing that news

co-mentioning leads to greater increases in Google and Bloomberg search volumes

than unconditional news coverage. Our findings suggest that attention spillover

in a news-based network can lead to significant stock market overvaluations,

and especially when arbitrage is limited.

-

Precise financial series predicting has long been a difficult problem because

of unstableness and many noises within the series. Although Traditional time

series models like ARIMA and GARCH have been researched and proved to be

effective in predicting, their performances are still far from satisfying.

Machine Learning, as an emerging research field in recent years, has brought

about many incredible improvements in tasks such as regressing and classifying,

and it's also promising to exploit the methodology in financial time series

predicting. In this paper, the predicting precision of financial time series

between traditional time series models and mainstream machine learning models

including some state-of-the-art ones of deep learning are compared through

experiment using real stock index data from history. The result shows that

machine learning as a modern method far surpasses traditional models in

precision.

-

A fundamental problem in studying and modeling economic and financial systems

is represented by privacy issues, which put severe limitations on the amount of

accessible information. Here we introduce a novel, highly nontrivial method to

reconstruct the structural properties of complex weighted networks of this kind

using only partial information: the total number of nodes and links, and the

values of the strength for all nodes. The latter are used as fitness to

estimate the unknown node degrees through a standard configuration model. Then,

these estimated degrees and the strengths are used to calibrate an enhanced

configuration model in order to generate ensembles of networks intended to

represent the real system. The method, which is tested on real economic and

financial networks, while drastically reducing the amount of information needed

to infer network properties, turns out to be remarkably effective$-$thus

representing a valuable tool for gaining insights on privacy-protected

socioeconomic systems.

-

We propose a novel framework to investigate lead-lag relationships between

two financial assets. Our framework bridges a gap between continuous-time

modeling based on Brownian motion and the existing wavelet methods for lead-lag

analysis based on discrete-time models and enables us to analyze the

multi-scale structure of lead-lag effects. We also present a statistical

methodology for the scale-by-scale analysis of lead-lag effects in the proposed

framework and develop an asymptotic theory applicable to a situation including

stochastic volatilities and irregular sampling. Finally, we report several

numerical experiments to demonstrate how our framework works in practice.

-

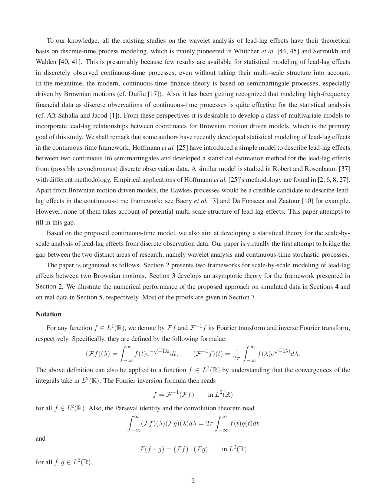

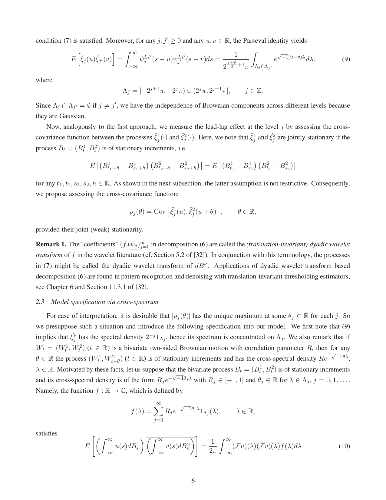

In this paper, we provide non-parametric statistical tools to test

stationarity of microstructure noise in general hidden Ito semimartingales, and

discuss how to measure liquidity risk using high frequency financial data. In

particular, we investigate the impact of non-stationary microstructure noise on

some volatility estimators, and design three complementary tests by exploiting

edge effects, information aggregation of local estimates and high-frequency

asymptotic approximation. The asymptotic distributions of these tests are

available under both stationary and non-stationary assumptions, thereby enable

us to conservatively control type-I errors and meanwhile ensure the proposed

tests enjoy the asymptotically optimal statistical power. Besides it also

enables us to empirically measure aggregate liquidity risks by these test

statistics. As byproducts, functional dependence and endogenous microstructure

noise are briefly discussed. Simulation with a realistic configuration

corroborates our theoretical results, and our empirical study indicates the

prevalence of non-stationary microstructure noise in New York Stock Exchange.

-

We conduct an extensive evaluation of price jump tests based on

high-frequency financial data. After providing a concise review of multiple

alternative tests, we document the size and power of all tests in a range of

empirically relevant scenarios. Particular focus is given to the robustness of

test performance to the presence of jumps in volatility and microstructure

noise, and to the impact of sampling frequency. The paper concludes by

providing guidelines for empirical researchers about which test to choose in

any given setting.

-

In this paper, we give a general time-varying parameter model, where the

multidimensional parameter possibly includes jumps. The quantity of interest is

defined as the integrated value over time of the parameter process $\Theta =

T^{-1} \int_0^T \theta_t^* dt$. We provide a local parametric estimator (LPE)

of $\Theta$ and conditions under which we can show the central limit theorem.

Roughly speaking those conditions correspond to some uniform limit theory in

the parametric version of the problem. The framework is restricted to the

specific convergence rate $n^{1/2}$. Several examples of LPE are studied:

estimation of volatility, powers of volatility, volatility when incorporating

trading information and time-varying MA(1).

-

We prove strong consistency and asymptotic normality of least squares

estimators for the subcritical Heston model based on continuous time

observations. We also present some numerical illustrations of our results.

-

Researchers developed the Economic Complexity Index (ECI) as a measure of the

overall sophistication of a country's products. They argued that this measure

explains economic growth better than the conventional variables such as human

capital. This paper suggests a simpler measure of production complexity, the

logarithm of product diversification, which has a natural foundation in

information theory: it measures the information needed to encode the knowledge

required to make a country's products. This measure explains well the income

differences between countries. It has a basic link with ECI that is strongly

supported by the data.

-

In this paper we estimate the mean-variance (MV) portfolio in the

high-dimensional case using the recent results from the theory of random

matrices. We construct a linear shrinkage estimator which is distribution-free

and is optimal in the sense of maximizing with probability $1$ the asymptotic

out-of-sample expected utility, i.e., mean-variance objective function for

several values of risk aversion coefficient which in particular leads to the

maximization of the out-of sample expected utility, to the maximization of the

out-of-sample Sharpe ratio, and to the minimization of the out-of-sample

variance. Its asymptotic properties are investigated when the number of assets

$p$ together with the sample size $n$ tend to infinity such that $p/n

\rightarrow c\in (0,+\infty)$. The results are obtained under weak assumptions

imposed on the distribution of the asset returns, namely the existence of the

fourth moments is only required. Thereafter we perform numerical and empirical

studies where the small- and large-sample behavior of the derived estimator is

investigated. The suggested estimator shows significant improvements over the

naive diversification and it is robust to the deviations from normality.

-

In this paper we derive the optimal linear shrinkage estimator for the

high-dimensional mean vector using random matrix theory. The results are

obtained under the assumption that both the dimension $p$ and the sample size

$n$ tend to infinity in such a way that $p/n \to c\in(0,\infty)$. Under weak

conditions imposed on the underlying data generating mechanism, we find the

asymptotic equivalents to the optimal shrinkage intensities and estimate them

consistently. The proposed nonparametric estimator for the high-dimensional

mean vector has a simple structure and is proven to minimize asymptotically,

with probability $1$, the quadratic loss when $c\in(0,1)$. When $c\in(1,

\infty)$ we modify the estimator by using a feasible estimator for the

precision covariance matrix. To this end, an exhaustive simulation study and an

application to real data are provided where the proposed estimator is compared

with known benchmarks from the literature. It turns out that the existing

estimators of the mean vector, including the new proposal, converge to the

sample mean vector when the true mean vector has an unbounded Euclidean norm.

-

Financial markets are notoriously complex environments, presenting vast

amounts of noisy, yet potentially informative data. We consider the problem of

forecasting financial time series from a wide range of information sources

using online Gaussian Processes with Automatic Relevance Determination (ARD)

kernels. We measure the performance gain, quantified in terms of Normalised

Root Mean Square Error (NRMSE), Median Absolute Deviation (MAD) and Pearson

correlation, from fusing each of four separate data domains: time series

technicals, sentiment analysis, options market data and broker recommendations.

We show evidence that ARD kernels produce meaningful feature rankings that help

retain salient inputs and reduce input dimensionality, providing a framework

for sifting through financial complexity. We measure the performance gain from

fusing each domain's heterogeneous data streams into a single probabilistic

model. In particular our findings highlight the critical value of options data

in mapping out the curvature of price space and inspire an intuitive, novel

direction for research in financial prediction.

-

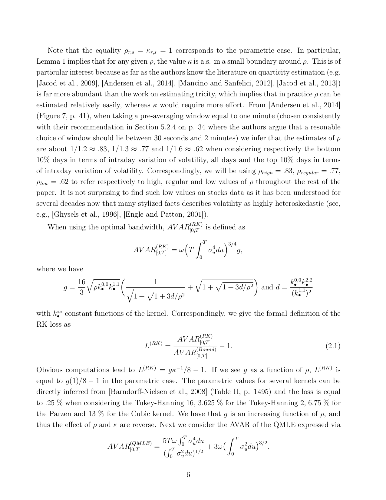

This paper shows how to carry out efficient asymptotic variance reduction

when estimating volatility in the presence of stochastic volatility and

microstructure noise with the realized kernels (RK) from [Barndorff-Nielsen et

al., 2008] and the quasi-maximum likelihood estimator (QMLE) studied in [Xiu,

2010]. To obtain such a reduction, we chop the data into B blocks, compute the

RK (or QMLE) on each block, and aggregate the block estimates. The ratio of

asymptotic variance over the bound of asymptotic efficiency converges as B

increases to the ratio in the parametric version of the problem, i.e. 1.0025 in

the case of the fastest RK Tukey-Hanning 16 and 1 for the QMLE. The impact of

stochastic sampling times and jump in the price process is examined carefully.

The finite sample performance of both estimators is investigated in

simulations, while empirical work illustrates the gain in practice.

-

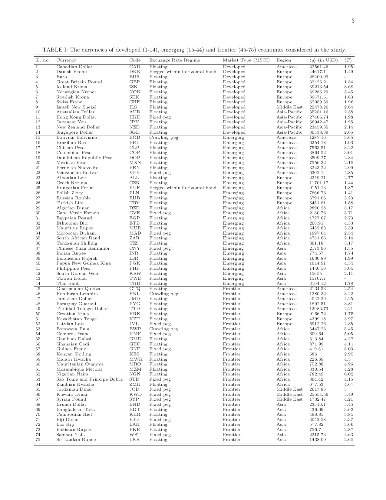

Identifying behavior that is relatively invariant under different conditions

is a challenging task in far-from-equilibrium complex systems. As an example of

how the existence of a semi-invariant signature can be masked by the

heterogeneity in the properties of the components comprising such systems, we

consider the exchange rate dynamics in the international currency market. We

show that the exponents characterizing the heavy tails of fluctuation

distributions for different currencies systematically diverge from a putative

universal form associated with the median value (~2) of the exponents. We

relate the degree of deviation of a particular currency from such an "inverse

square law" to fundamental macroscopic properties of the corresponding economy,

viz., measures of per capita production output and diversity of export

products. We also show that in contrast to uncorrelated random walks exhibited

by the exchange rate dynamics for currencies belonging to developed economies,

those of the less developed economies show characteristics of sub-diffusive

processes which we relate to the anti-correlated nature of the corresponding

fluctuations. Approaches similar to that presented here may help in identifying

invariant features obscured by the heterogeneous nature of components in other

complex systems.

-

Financial markets provide a natural quantitative lab for understanding some

of the most advanced human behaviours. Among them is the use of mathematical

tools known as financial instruments. Besides money, the two most fundamental

financial instruments are bonds and equities. More than 30 years ago Mehra and

Prescott found the numerical performance of equities relative to government

bonds could not be explained by consumption-based (mainstream) economic

theories. This empirical observation, known as the Equity Premium Puzzle, has

been defying mainstream economics ever since. The recent financial crisis

revealed an even deeper need for understanding financial products. We show how

understanding the rational nature of product design resolves the Equity Premium

Puzzle. In doing so we obtain an experimentally tested theory of product

design.

-

Using 1-min returns of Bitcoin prices, we investigate statistical properties

and multifractality of a Bitcoin time series. We find that the 1-min return

distribution is fat-tailed, and kurtosis largely deviates from the Gaussian

expectation. Although for large sampling periods, kurtosis is anticipated to

approach the Gaussian expectation, we find that convergence to that is very

slow. Skewness is found to be negative at time scales shorter than one day and

becomes consistent with zero at time scales longer than about one week. We also

investigate daily volatility-asymmetry by using GARCH, GJR, and RGARCH models,

and find no evidence of it. On exploring multifractality using multifractal

detrended fluctuation analysis, we find that the Bitcoin time series exhibits

multifractality. The sources of multifractality are investigated, confirming

that both temporal correlation and the fat-tailed distribution contribute to

it. The influence of "Brexit" on June 23, 2016 to GBP--USD exchange rate and

Bitcoin is examined in multifractal properties. We find that, while Brexit

influenced the GBP--USD exchange rate, Bitcoin was robust to Brexit.

-

We study asymptotic properties of maximum likelihood estimators of drift

parameters for a jump-type Heston model based on continuous time observations,

where the jump process can be any purely non-Gaussian L\'evy process of not

necessarily bounded variation with a L\'evy measure concentrated on

$(-1,\infty)$. We prove strong consistency and asymptotic normality for all

admissible parameter values except one, where we show only weak consistency and

mixed normal (but non-normal) asymptotic behavior. It turns out that the

volatility of the price process is a measurable function of the price process.

We also present some numerical illustrations to confirm our results.

-

The liberalization of electricity markets and the development of renewable

energy sources has led to new challenges for decision makers. These challenges

are accompanied by an increasing uncertainty about future electricity price

movements. The increasing amount of papers, which aim to model and predict

electricity prices for a short period of time provided new opportunities for

market participants. However, the electricity price literature seem to be very

scarce on the issue of medium- to long-term price forecasting, which is

mandatory for investment and political decisions. Our paper closes this gap by

introducing a new approach to simulate electricity prices with hourly

resolution for several months up to three years. Considering the uncertainty of

future events we are able to provide probabilistic forecasts which are able to

detect probabilities for price spikes even in the long-run. As market we

decided to use the EPEX day-ahead electricity market for Germany and Austria.

Our model extends the X-Model which mainly utilizes the sale and purchase curve

for electricity day-ahead auctions. By applying our procedure we are able to

give probabilities for the due to the EEG practical relevant event of six

consecutive hours of negative prices. We find that using the supply and demand

curve based model in the long-run yields realistic patterns for the time series

of electricity prices and leads to promising results considering common error

measures.

-

To understand the relationship between news sentiment and company stock price

movements, and to better understand connectivity among companies, we define an

algorithm for measuring sentiment-based network risk. The algorithm ranks

companies in networks of co-occurrences, and measures sentiment-based risk, by

calculating both individual risks and aggregated network risks. We extract

relative sentiment for companies to get a measure of individual company risk,

and input it into our risk model together with co-occurrences of companies

extracted from news on a quarterly basis. We can show that the highest

quarterly risk value outputted by our risk model, is correlated to a higher

chance of stock price decline, up to 70 days after a risk measurement. Our

results show that the highest difference in the probability of stock price

decline, compared to the benchmark containing all risk values for the same

period, is during the interval from 21 to 30 days after a quarterly

measurement. The highest average probability of company stock price decline, is

found at a delay of 28 days, after a company has reached its maximum risk

value. The highest probability differences for a daily decline were calculated

to be 13 percentage points.

This tutorial provides a gentle introduction to the particle Metropolis-Hastings (PMH) algorithm for parameter inference in nonlinear state-space models together with a software implementation in the statistical programming language R. We employ a step-by-step approach to develop an implementation of the PMH algorithm (and the particle filter within) together with the reader. This final implementation is also available as the package pmhtutorial in the CRAN repository. Throughout the tutorial, we provide some intuition as to how the algorithm operates and discuss some solutions to problems that might occur in practice. To illustrate the use of PMH, we consider parameter inference in a linear Gaussian state-space model with synthetic data and a nonlinear stochastic volatility model with real-world data.

This tutorial provides a gentle introduction to the particle Metropolis-Hastings (PMH) algorithm for parameter inference in nonlinear state-space models together with a software implementation in the statistical programming language R. We employ a step-by-step approach to develop an implementation of the PMH algorithm (and the particle filter within) together with the reader. This final implementation is also available as the package pmhtutorial in the CRAN repository. Throughout the tutorial, we provide some intuition as to how the algorithm operates and discuss some solutions to problems that might occur in practice. To illustrate the use of PMH, we consider parameter inference in a linear Gaussian state-space model with synthetic data and a nonlinear stochastic volatility model with real-world data.

We review the state of the art of clustering financial time series and the study of their correlations alongside other interaction networks. The aim of this review is to gather in one place the relevant material from different fields, e.g. machine learning, information geometry, econophysics, statistical physics, econometrics, behavioral finance. We hope it will help researchers to use more effectively this alternative modeling of the financial time series. Decision makers and quantitative researchers may also be able to leverage its insights. Finally, we also hope that this review will form the basis of an open toolbox to study correlations, hierarchies, networks and clustering in financial markets.

We review the state of the art of clustering financial time series and the study of their correlations alongside other interaction networks. The aim of this review is to gather in one place the relevant material from different fields, e.g. machine learning, information geometry, econophysics, statistical physics, econometrics, behavioral finance. We hope it will help researchers to use more effectively this alternative modeling of the financial time series. Decision makers and quantitative researchers may also be able to leverage its insights. Finally, we also hope that this review will form the basis of an open toolbox to study correlations, hierarchies, networks and clustering in financial markets.

We give complete algorithms and source code for constructing (multilevel) statistical industry classifications, including methods for fixing the number of clusters at each level (and the number of levels). Under the hood there are clustering algorithms (e.g., k-means). However, what should we cluster? Correlations? Returns? The answer turns out to be neither and our backtests suggest that these details make a sizable difference. We also give an algorithm and source code for building "hybrid" industry classifications by improving off-the-shelf "fundamental" industry classifications by applying our statistical industry classification methods to them. The presentation is intended to be pedagogical and geared toward practical applications in quantitative trading.

We give complete algorithms and source code for constructing (multilevel) statistical industry classifications, including methods for fixing the number of clusters at each level (and the number of levels). Under the hood there are clustering algorithms (e.g., k-means). However, what should we cluster? Correlations? Returns? The answer turns out to be neither and our backtests suggest that these details make a sizable difference. We also give an algorithm and source code for building "hybrid" industry classifications by improving off-the-shelf "fundamental" industry classifications by applying our statistical industry classification methods to them. The presentation is intended to be pedagogical and geared toward practical applications in quantitative trading.

In this paper, we introduce quantile coherency to measure general dependence structures emerging in the joint distribution in the frequency domain and argue that this type of dependence is natural for economic time series but remains invisible when only the traditional analysis is employed. We define estimators which capture the general dependence structure, provide a detailed analysis of their asymptotic properties and discuss how to conduct inference for a general class of possibly nonlinear processes. In an empirical illustration we examine the dependence of bivariate stock market returns and shed new light on measurement of tail risk in financial markets. We also provide a modelling exercise to illustrate how applied researchers can benefit from using quantile coherency when assessing time series models.

In this paper, we introduce quantile coherency to measure general dependence structures emerging in the joint distribution in the frequency domain and argue that this type of dependence is natural for economic time series but remains invisible when only the traditional analysis is employed. We define estimators which capture the general dependence structure, provide a detailed analysis of their asymptotic properties and discuss how to conduct inference for a general class of possibly nonlinear processes. In an empirical illustration we examine the dependence of bivariate stock market returns and shed new light on measurement of tail risk in financial markets. We also provide a modelling exercise to illustrate how applied researchers can benefit from using quantile coherency when assessing time series models.

In a very high-dimensional vector space, two randomly-chosen vectors are almost orthogonal with high probability. Starting from this observation, we develop a statistical factor model, the random factor model, in which factors are chosen at random based on the random projection method. Randomness of factors has the consequence that covariance matrix is well preserved in a linear factor representation. It also enables derivation of probabilistic bounds for the accuracy of the random factor representation of time-series, their cross-correlations and covariances. As an application, we analyze reproduction of time-series and their cross-correlation coefficients in the well-diversified Russell 3,000 equity index.

In a very high-dimensional vector space, two randomly-chosen vectors are almost orthogonal with high probability. Starting from this observation, we develop a statistical factor model, the random factor model, in which factors are chosen at random based on the random projection method. Randomness of factors has the consequence that covariance matrix is well preserved in a linear factor representation. It also enables derivation of probabilistic bounds for the accuracy of the random factor representation of time-series, their cross-correlations and covariances. As an application, we analyze reproduction of time-series and their cross-correlation coefficients in the well-diversified Russell 3,000 equity index.

We examine the effect of investor attention spillover on stock return predictability. Using a novel measure, the News Network Triggered Attention index (NNTA), we find that NNTA negatively predicts market returns with a monthly in(out)-of-sample R-square of 5.97% (5.80%). In the cross-section, a long-short portfolio based on news co-occurrence generates a significant monthly alpha of 68 basis points. The results are robust to the inclusion of alternative attention proxies, sentiment measures, other news- and information-based predictors, across recession and expansion periods. We further validate the attention spillover effect by showing that news co-mentioning leads to greater increases in Google and Bloomberg search volumes than unconditional news coverage. Our findings suggest that attention spillover in a news-based network can lead to significant stock market overvaluations, and especially when arbitrage is limited.

We examine the effect of investor attention spillover on stock return predictability. Using a novel measure, the News Network Triggered Attention index (NNTA), we find that NNTA negatively predicts market returns with a monthly in(out)-of-sample R-square of 5.97% (5.80%). In the cross-section, a long-short portfolio based on news co-occurrence generates a significant monthly alpha of 68 basis points. The results are robust to the inclusion of alternative attention proxies, sentiment measures, other news- and information-based predictors, across recession and expansion periods. We further validate the attention spillover effect by showing that news co-mentioning leads to greater increases in Google and Bloomberg search volumes than unconditional news coverage. Our findings suggest that attention spillover in a news-based network can lead to significant stock market overvaluations, and especially when arbitrage is limited.

Precise financial series predicting has long been a difficult problem because of unstableness and many noises within the series. Although Traditional time series models like ARIMA and GARCH have been researched and proved to be effective in predicting, their performances are still far from satisfying. Machine Learning, as an emerging research field in recent years, has brought about many incredible improvements in tasks such as regressing and classifying, and it's also promising to exploit the methodology in financial time series predicting. In this paper, the predicting precision of financial time series between traditional time series models and mainstream machine learning models including some state-of-the-art ones of deep learning are compared through experiment using real stock index data from history. The result shows that machine learning as a modern method far surpasses traditional models in precision.

Precise financial series predicting has long been a difficult problem because of unstableness and many noises within the series. Although Traditional time series models like ARIMA and GARCH have been researched and proved to be effective in predicting, their performances are still far from satisfying. Machine Learning, as an emerging research field in recent years, has brought about many incredible improvements in tasks such as regressing and classifying, and it's also promising to exploit the methodology in financial time series predicting. In this paper, the predicting precision of financial time series between traditional time series models and mainstream machine learning models including some state-of-the-art ones of deep learning are compared through experiment using real stock index data from history. The result shows that machine learning as a modern method far surpasses traditional models in precision.

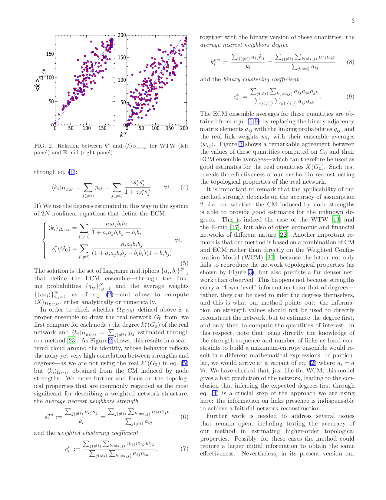

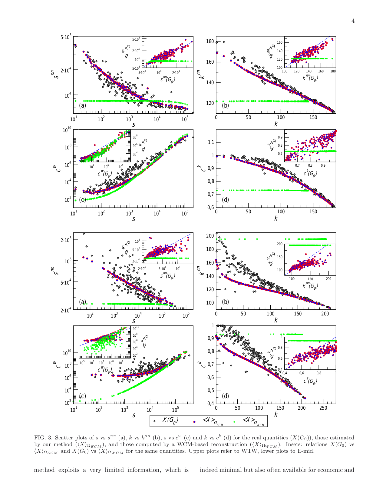

A fundamental problem in studying and modeling economic and financial systems is represented by privacy issues, which put severe limitations on the amount of accessible information. Here we introduce a novel, highly nontrivial method to reconstruct the structural properties of complex weighted networks of this kind using only partial information: the total number of nodes and links, and the values of the strength for all nodes. The latter are used as fitness to estimate the unknown node degrees through a standard configuration model. Then, these estimated degrees and the strengths are used to calibrate an enhanced configuration model in order to generate ensembles of networks intended to represent the real system. The method, which is tested on real economic and financial networks, while drastically reducing the amount of information needed to infer network properties, turns out to be remarkably effective$-$thus representing a valuable tool for gaining insights on privacy-protected socioeconomic systems.

A fundamental problem in studying and modeling economic and financial systems is represented by privacy issues, which put severe limitations on the amount of accessible information. Here we introduce a novel, highly nontrivial method to reconstruct the structural properties of complex weighted networks of this kind using only partial information: the total number of nodes and links, and the values of the strength for all nodes. The latter are used as fitness to estimate the unknown node degrees through a standard configuration model. Then, these estimated degrees and the strengths are used to calibrate an enhanced configuration model in order to generate ensembles of networks intended to represent the real system. The method, which is tested on real economic and financial networks, while drastically reducing the amount of information needed to infer network properties, turns out to be remarkably effective$-$thus representing a valuable tool for gaining insights on privacy-protected socioeconomic systems.

We propose a novel framework to investigate lead-lag relationships between two financial assets. Our framework bridges a gap between continuous-time modeling based on Brownian motion and the existing wavelet methods for lead-lag analysis based on discrete-time models and enables us to analyze the multi-scale structure of lead-lag effects. We also present a statistical methodology for the scale-by-scale analysis of lead-lag effects in the proposed framework and develop an asymptotic theory applicable to a situation including stochastic volatilities and irregular sampling. Finally, we report several numerical experiments to demonstrate how our framework works in practice.

We propose a novel framework to investigate lead-lag relationships between two financial assets. Our framework bridges a gap between continuous-time modeling based on Brownian motion and the existing wavelet methods for lead-lag analysis based on discrete-time models and enables us to analyze the multi-scale structure of lead-lag effects. We also present a statistical methodology for the scale-by-scale analysis of lead-lag effects in the proposed framework and develop an asymptotic theory applicable to a situation including stochastic volatilities and irregular sampling. Finally, we report several numerical experiments to demonstrate how our framework works in practice.

In this paper, we provide non-parametric statistical tools to test stationarity of microstructure noise in general hidden Ito semimartingales, and discuss how to measure liquidity risk using high frequency financial data. In particular, we investigate the impact of non-stationary microstructure noise on some volatility estimators, and design three complementary tests by exploiting edge effects, information aggregation of local estimates and high-frequency asymptotic approximation. The asymptotic distributions of these tests are available under both stationary and non-stationary assumptions, thereby enable us to conservatively control type-I errors and meanwhile ensure the proposed tests enjoy the asymptotically optimal statistical power. Besides it also enables us to empirically measure aggregate liquidity risks by these test statistics. As byproducts, functional dependence and endogenous microstructure noise are briefly discussed. Simulation with a realistic configuration corroborates our theoretical results, and our empirical study indicates the prevalence of non-stationary microstructure noise in New York Stock Exchange.

In this paper, we provide non-parametric statistical tools to test stationarity of microstructure noise in general hidden Ito semimartingales, and discuss how to measure liquidity risk using high frequency financial data. In particular, we investigate the impact of non-stationary microstructure noise on some volatility estimators, and design three complementary tests by exploiting edge effects, information aggregation of local estimates and high-frequency asymptotic approximation. The asymptotic distributions of these tests are available under both stationary and non-stationary assumptions, thereby enable us to conservatively control type-I errors and meanwhile ensure the proposed tests enjoy the asymptotically optimal statistical power. Besides it also enables us to empirically measure aggregate liquidity risks by these test statistics. As byproducts, functional dependence and endogenous microstructure noise are briefly discussed. Simulation with a realistic configuration corroborates our theoretical results, and our empirical study indicates the prevalence of non-stationary microstructure noise in New York Stock Exchange.

We conduct an extensive evaluation of price jump tests based on high-frequency financial data. After providing a concise review of multiple alternative tests, we document the size and power of all tests in a range of empirically relevant scenarios. Particular focus is given to the robustness of test performance to the presence of jumps in volatility and microstructure noise, and to the impact of sampling frequency. The paper concludes by providing guidelines for empirical researchers about which test to choose in any given setting.

We conduct an extensive evaluation of price jump tests based on high-frequency financial data. After providing a concise review of multiple alternative tests, we document the size and power of all tests in a range of empirically relevant scenarios. Particular focus is given to the robustness of test performance to the presence of jumps in volatility and microstructure noise, and to the impact of sampling frequency. The paper concludes by providing guidelines for empirical researchers about which test to choose in any given setting.

In this paper, we give a general time-varying parameter model, where the multidimensional parameter possibly includes jumps. The quantity of interest is defined as the integrated value over time of the parameter process $\Theta = T^{-1} \int_0^T \theta_t^* dt$. We provide a local parametric estimator (LPE) of $\Theta$ and conditions under which we can show the central limit theorem. Roughly speaking those conditions correspond to some uniform limit theory in the parametric version of the problem. The framework is restricted to the specific convergence rate $n^{1/2}$. Several examples of LPE are studied: estimation of volatility, powers of volatility, volatility when incorporating trading information and time-varying MA(1).

In this paper, we give a general time-varying parameter model, where the multidimensional parameter possibly includes jumps. The quantity of interest is defined as the integrated value over time of the parameter process $\Theta = T^{-1} \int_0^T \theta_t^* dt$. We provide a local parametric estimator (LPE) of $\Theta$ and conditions under which we can show the central limit theorem. Roughly speaking those conditions correspond to some uniform limit theory in the parametric version of the problem. The framework is restricted to the specific convergence rate $n^{1/2}$. Several examples of LPE are studied: estimation of volatility, powers of volatility, volatility when incorporating trading information and time-varying MA(1).

In this paper we estimate the mean-variance (MV) portfolio in the high-dimensional case using the recent results from the theory of random matrices. We construct a linear shrinkage estimator which is distribution-free and is optimal in the sense of maximizing with probability $1$ the asymptotic out-of-sample expected utility, i.e., mean-variance objective function for several values of risk aversion coefficient which in particular leads to the maximization of the out-of sample expected utility, to the maximization of the out-of-sample Sharpe ratio, and to the minimization of the out-of-sample variance. Its asymptotic properties are investigated when the number of assets $p$ together with the sample size $n$ tend to infinity such that $p/n \rightarrow c\in (0,+\infty)$. The results are obtained under weak assumptions imposed on the distribution of the asset returns, namely the existence of the fourth moments is only required. Thereafter we perform numerical and empirical studies where the small- and large-sample behavior of the derived estimator is investigated. The suggested estimator shows significant improvements over the naive diversification and it is robust to the deviations from normality.

In this paper we estimate the mean-variance (MV) portfolio in the high-dimensional case using the recent results from the theory of random matrices. We construct a linear shrinkage estimator which is distribution-free and is optimal in the sense of maximizing with probability $1$ the asymptotic out-of-sample expected utility, i.e., mean-variance objective function for several values of risk aversion coefficient which in particular leads to the maximization of the out-of sample expected utility, to the maximization of the out-of-sample Sharpe ratio, and to the minimization of the out-of-sample variance. Its asymptotic properties are investigated when the number of assets $p$ together with the sample size $n$ tend to infinity such that $p/n \rightarrow c\in (0,+\infty)$. The results are obtained under weak assumptions imposed on the distribution of the asset returns, namely the existence of the fourth moments is only required. Thereafter we perform numerical and empirical studies where the small- and large-sample behavior of the derived estimator is investigated. The suggested estimator shows significant improvements over the naive diversification and it is robust to the deviations from normality.

Financial markets are notoriously complex environments, presenting vast amounts of noisy, yet potentially informative data. We consider the problem of forecasting financial time series from a wide range of information sources using online Gaussian Processes with Automatic Relevance Determination (ARD) kernels. We measure the performance gain, quantified in terms of Normalised Root Mean Square Error (NRMSE), Median Absolute Deviation (MAD) and Pearson correlation, from fusing each of four separate data domains: time series technicals, sentiment analysis, options market data and broker recommendations. We show evidence that ARD kernels produce meaningful feature rankings that help retain salient inputs and reduce input dimensionality, providing a framework for sifting through financial complexity. We measure the performance gain from fusing each domain's heterogeneous data streams into a single probabilistic model. In particular our findings highlight the critical value of options data in mapping out the curvature of price space and inspire an intuitive, novel direction for research in financial prediction.

Financial markets are notoriously complex environments, presenting vast amounts of noisy, yet potentially informative data. We consider the problem of forecasting financial time series from a wide range of information sources using online Gaussian Processes with Automatic Relevance Determination (ARD) kernels. We measure the performance gain, quantified in terms of Normalised Root Mean Square Error (NRMSE), Median Absolute Deviation (MAD) and Pearson correlation, from fusing each of four separate data domains: time series technicals, sentiment analysis, options market data and broker recommendations. We show evidence that ARD kernels produce meaningful feature rankings that help retain salient inputs and reduce input dimensionality, providing a framework for sifting through financial complexity. We measure the performance gain from fusing each domain's heterogeneous data streams into a single probabilistic model. In particular our findings highlight the critical value of options data in mapping out the curvature of price space and inspire an intuitive, novel direction for research in financial prediction.

This paper shows how to carry out efficient asymptotic variance reduction when estimating volatility in the presence of stochastic volatility and microstructure noise with the realized kernels (RK) from [Barndorff-Nielsen et al., 2008] and the quasi-maximum likelihood estimator (QMLE) studied in [Xiu, 2010]. To obtain such a reduction, we chop the data into B blocks, compute the RK (or QMLE) on each block, and aggregate the block estimates. The ratio of asymptotic variance over the bound of asymptotic efficiency converges as B increases to the ratio in the parametric version of the problem, i.e. 1.0025 in the case of the fastest RK Tukey-Hanning 16 and 1 for the QMLE. The impact of stochastic sampling times and jump in the price process is examined carefully. The finite sample performance of both estimators is investigated in simulations, while empirical work illustrates the gain in practice.

This paper shows how to carry out efficient asymptotic variance reduction when estimating volatility in the presence of stochastic volatility and microstructure noise with the realized kernels (RK) from [Barndorff-Nielsen et al., 2008] and the quasi-maximum likelihood estimator (QMLE) studied in [Xiu, 2010]. To obtain such a reduction, we chop the data into B blocks, compute the RK (or QMLE) on each block, and aggregate the block estimates. The ratio of asymptotic variance over the bound of asymptotic efficiency converges as B increases to the ratio in the parametric version of the problem, i.e. 1.0025 in the case of the fastest RK Tukey-Hanning 16 and 1 for the QMLE. The impact of stochastic sampling times and jump in the price process is examined carefully. The finite sample performance of both estimators is investigated in simulations, while empirical work illustrates the gain in practice.

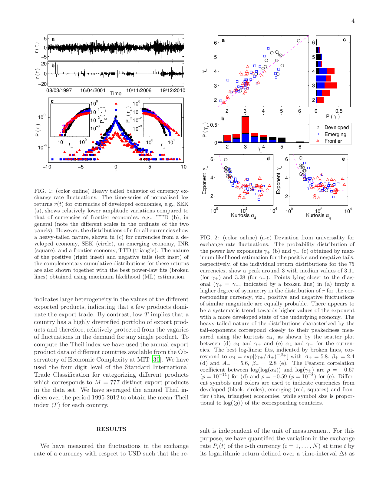

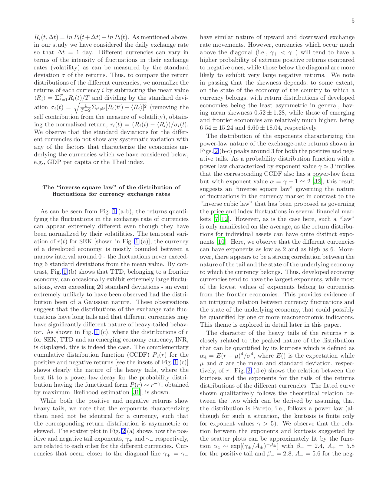

Identifying behavior that is relatively invariant under different conditions is a challenging task in far-from-equilibrium complex systems. As an example of how the existence of a semi-invariant signature can be masked by the heterogeneity in the properties of the components comprising such systems, we consider the exchange rate dynamics in the international currency market. We show that the exponents characterizing the heavy tails of fluctuation distributions for different currencies systematically diverge from a putative universal form associated with the median value (~2) of the exponents. We relate the degree of deviation of a particular currency from such an "inverse square law" to fundamental macroscopic properties of the corresponding economy, viz., measures of per capita production output and diversity of export products. We also show that in contrast to uncorrelated random walks exhibited by the exchange rate dynamics for currencies belonging to developed economies, those of the less developed economies show characteristics of sub-diffusive processes which we relate to the anti-correlated nature of the corresponding fluctuations. Approaches similar to that presented here may help in identifying invariant features obscured by the heterogeneous nature of components in other complex systems.

Identifying behavior that is relatively invariant under different conditions is a challenging task in far-from-equilibrium complex systems. As an example of how the existence of a semi-invariant signature can be masked by the heterogeneity in the properties of the components comprising such systems, we consider the exchange rate dynamics in the international currency market. We show that the exponents characterizing the heavy tails of fluctuation distributions for different currencies systematically diverge from a putative universal form associated with the median value (~2) of the exponents. We relate the degree of deviation of a particular currency from such an "inverse square law" to fundamental macroscopic properties of the corresponding economy, viz., measures of per capita production output and diversity of export products. We also show that in contrast to uncorrelated random walks exhibited by the exchange rate dynamics for currencies belonging to developed economies, those of the less developed economies show characteristics of sub-diffusive processes which we relate to the anti-correlated nature of the corresponding fluctuations. Approaches similar to that presented here may help in identifying invariant features obscured by the heterogeneous nature of components in other complex systems.

Financial markets provide a natural quantitative lab for understanding some of the most advanced human behaviours. Among them is the use of mathematical tools known as financial instruments. Besides money, the two most fundamental financial instruments are bonds and equities. More than 30 years ago Mehra and Prescott found the numerical performance of equities relative to government bonds could not be explained by consumption-based (mainstream) economic theories. This empirical observation, known as the Equity Premium Puzzle, has been defying mainstream economics ever since. The recent financial crisis revealed an even deeper need for understanding financial products. We show how understanding the rational nature of product design resolves the Equity Premium Puzzle. In doing so we obtain an experimentally tested theory of product design.

Financial markets provide a natural quantitative lab for understanding some of the most advanced human behaviours. Among them is the use of mathematical tools known as financial instruments. Besides money, the two most fundamental financial instruments are bonds and equities. More than 30 years ago Mehra and Prescott found the numerical performance of equities relative to government bonds could not be explained by consumption-based (mainstream) economic theories. This empirical observation, known as the Equity Premium Puzzle, has been defying mainstream economics ever since. The recent financial crisis revealed an even deeper need for understanding financial products. We show how understanding the rational nature of product design resolves the Equity Premium Puzzle. In doing so we obtain an experimentally tested theory of product design.

Using 1-min returns of Bitcoin prices, we investigate statistical properties and multifractality of a Bitcoin time series. We find that the 1-min return distribution is fat-tailed, and kurtosis largely deviates from the Gaussian expectation. Although for large sampling periods, kurtosis is anticipated to approach the Gaussian expectation, we find that convergence to that is very slow. Skewness is found to be negative at time scales shorter than one day and becomes consistent with zero at time scales longer than about one week. We also investigate daily volatility-asymmetry by using GARCH, GJR, and RGARCH models, and find no evidence of it. On exploring multifractality using multifractal detrended fluctuation analysis, we find that the Bitcoin time series exhibits multifractality. The sources of multifractality are investigated, confirming that both temporal correlation and the fat-tailed distribution contribute to it. The influence of "Brexit" on June 23, 2016 to GBP--USD exchange rate and Bitcoin is examined in multifractal properties. We find that, while Brexit influenced the GBP--USD exchange rate, Bitcoin was robust to Brexit.

Using 1-min returns of Bitcoin prices, we investigate statistical properties and multifractality of a Bitcoin time series. We find that the 1-min return distribution is fat-tailed, and kurtosis largely deviates from the Gaussian expectation. Although for large sampling periods, kurtosis is anticipated to approach the Gaussian expectation, we find that convergence to that is very slow. Skewness is found to be negative at time scales shorter than one day and becomes consistent with zero at time scales longer than about one week. We also investigate daily volatility-asymmetry by using GARCH, GJR, and RGARCH models, and find no evidence of it. On exploring multifractality using multifractal detrended fluctuation analysis, we find that the Bitcoin time series exhibits multifractality. The sources of multifractality are investigated, confirming that both temporal correlation and the fat-tailed distribution contribute to it. The influence of "Brexit" on June 23, 2016 to GBP--USD exchange rate and Bitcoin is examined in multifractal properties. We find that, while Brexit influenced the GBP--USD exchange rate, Bitcoin was robust to Brexit.

We study asymptotic properties of maximum likelihood estimators of drift parameters for a jump-type Heston model based on continuous time observations, where the jump process can be any purely non-Gaussian L\'evy process of not necessarily bounded variation with a L\'evy measure concentrated on $(-1,\infty)$. We prove strong consistency and asymptotic normality for all admissible parameter values except one, where we show only weak consistency and mixed normal (but non-normal) asymptotic behavior. It turns out that the volatility of the price process is a measurable function of the price process. We also present some numerical illustrations to confirm our results.

We study asymptotic properties of maximum likelihood estimators of drift parameters for a jump-type Heston model based on continuous time observations, where the jump process can be any purely non-Gaussian L\'evy process of not necessarily bounded variation with a L\'evy measure concentrated on $(-1,\infty)$. We prove strong consistency and asymptotic normality for all admissible parameter values except one, where we show only weak consistency and mixed normal (but non-normal) asymptotic behavior. It turns out that the volatility of the price process is a measurable function of the price process. We also present some numerical illustrations to confirm our results.

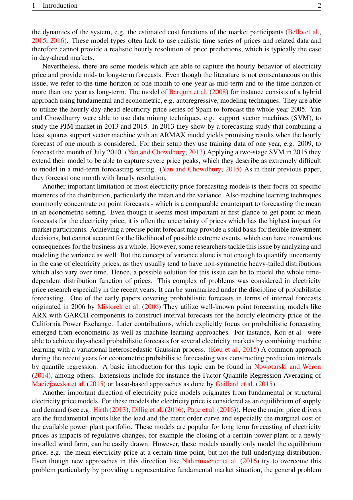

The liberalization of electricity markets and the development of renewable energy sources has led to new challenges for decision makers. These challenges are accompanied by an increasing uncertainty about future electricity price movements. The increasing amount of papers, which aim to model and predict electricity prices for a short period of time provided new opportunities for market participants. However, the electricity price literature seem to be very scarce on the issue of medium- to long-term price forecasting, which is mandatory for investment and political decisions. Our paper closes this gap by introducing a new approach to simulate electricity prices with hourly resolution for several months up to three years. Considering the uncertainty of future events we are able to provide probabilistic forecasts which are able to detect probabilities for price spikes even in the long-run. As market we decided to use the EPEX day-ahead electricity market for Germany and Austria. Our model extends the X-Model which mainly utilizes the sale and purchase curve for electricity day-ahead auctions. By applying our procedure we are able to give probabilities for the due to the EEG practical relevant event of six consecutive hours of negative prices. We find that using the supply and demand curve based model in the long-run yields realistic patterns for the time series of electricity prices and leads to promising results considering common error measures.

The liberalization of electricity markets and the development of renewable energy sources has led to new challenges for decision makers. These challenges are accompanied by an increasing uncertainty about future electricity price movements. The increasing amount of papers, which aim to model and predict electricity prices for a short period of time provided new opportunities for market participants. However, the electricity price literature seem to be very scarce on the issue of medium- to long-term price forecasting, which is mandatory for investment and political decisions. Our paper closes this gap by introducing a new approach to simulate electricity prices with hourly resolution for several months up to three years. Considering the uncertainty of future events we are able to provide probabilistic forecasts which are able to detect probabilities for price spikes even in the long-run. As market we decided to use the EPEX day-ahead electricity market for Germany and Austria. Our model extends the X-Model which mainly utilizes the sale and purchase curve for electricity day-ahead auctions. By applying our procedure we are able to give probabilities for the due to the EEG practical relevant event of six consecutive hours of negative prices. We find that using the supply and demand curve based model in the long-run yields realistic patterns for the time series of electricity prices and leads to promising results considering common error measures.